Millions of Americans cut off from unemployment benefits still won't return to work by year's end: analysis

Here are a few things to do if you're unemployed and need money now

Despite improving conditions and 1.3 million jobs being added to the market by the end of 2021, many Americans will still be out of work, according to a Goldman Sachs analysis. (iStock)

The expanded COVID-19 unemployment benefits helped millions of Americans make ends meet during the pandemic but analysts found that some actually earned more by staying home than they would have made by going to work.

Because of this generous unemployment payout, many politicians argued that unemployed Americans had less incentive to return to the workforce. In fact, about half of the states by June ended the extra pandemic unemployment assistance early in order to address a growing worker shortage.

Although unemployment benefits expired for the 5.3 million Americans in early September, hiring will only increase by about 1.3 million through the end of 2021, according to an analysis by Goldman Sachs released on Oct. 4.

"Current worker shortages reflect a perfect storm of factors that have significantly reduced the supply of workers who are currently looking for jobs at the same time that labor demand—as measured by job openings—has risen to an all-time high."

Goldman Sachs analysts provided a few suggestions for how the coronavirus pandemic impacted the workforce:

- Many workers used the pandemic as an opportunity to retire early. There are 1.5 million excess retirees — that's about a 0.6 percentage point hit to the labor market.

- Self-employment increased by over 800,000. Self-employment increased at the highest rate in the construction sector, where labor shortages are impacting the supply chain.

- Visas issued to immigrants and temporary workers fell by about 700,000. Analysts don't expect pandemic-related immigration declines to be offset by higher rates of immigration in the future.

Still, many Americans are simply out of work and without excess pandemic unemployment benefits. If you're unemployed and you need cash now, consider a few options to tide you over, such as emergency loans and cash-out mortgage refinancing.

If you decide to borrow money to make ends meet, visit Credible to compare rates across a variety of financial products. This ensures you're getting the most competitive interest rate for your financial situation.

MILLIONS OF AMERICANS FEAR MISSING DEBT PAYMENTS, NY FED REPORTS: HOW TO MANAGE YOUR DEBT

3 ways to get cash now if you're unemployed

Predatory short-term loans for those who are unemployed — such as those offered by payday lenders — can come with high interest rates and impossibly short repayment plans. Thankfully, there are other borrowing options for unemployed consumers who need online loans fast. Consider the following:

Keep reading to learn more about loan options for unemployed borrowers.

SENATE BLOCKS BILL TO SUSPEND DEBT LIMIT, AVERT GOVERNMENT SHUTDOWN THAT MAY DELAY SOCIAL SECURITY

1. Research emergency loans

Emergency loans are typically a type of unsecured personal loan that's offered by a bank, credit union or online lender. They offer small, lump-sum funding that you repay over a set period of time, typically several months or years.

Personal loans can be a good option if you need cash fast, since your funds may be disbursed into your bank account as soon as the next business day after loan approval.

Because personal loans are unsecured and don't require collateral, you can use the money as you see fit. But qualifying for this type of cash loan can be difficult if you're unemployed, since lenders determine eligibility based on your annual income, credit score and other financial criteria.

Even if you're currently out of work, you may still qualify for this type of loan if you have a solid credit history and an alternative source of income, such as Social Security, child support or alimony. But without a steady source of income, you might only qualify for offers with higher interest rates and additional fees. Still, personal loans are a good alternative to high-interest credit cards and payday loans.

You can check your loan options across multiple lenders without impacting your credit report on Credible. Once you have an idea of your estimated interest rate, use a personal loan calculator to estimate your monthly payments.

EVICTION MORATORIUM UPDATE: WARREN, PROGRESSIVES INTRODUCE BILL AIMED AT EXTENDING BAN

2. Borrow from your retirement account

Another option for emergency cash is to borrow a 401(k) loan. Borrowing from your retirement account essentially gives you a cash advance on your 401(k) with a low, fixed interest rate and flexible repayment schedule.

Since you're borrowing money from your own retirement savings, you won't be subject to a credit check. For that reason, these types of loans are popular among borrowers with a bad credit score.

However, not all retirement plans let you borrow from your 401(k), and many require that you're employed while you borrow. Still, it's good to check with your financial institution to see if you're an eligible borrower.

AOC AIMS TO EXTEND PANDEMIC UNEMPLOYMENT INSURANCE: WHAT TO DO IF YOU NEED CASH NOW

3. Tap into your home's equity

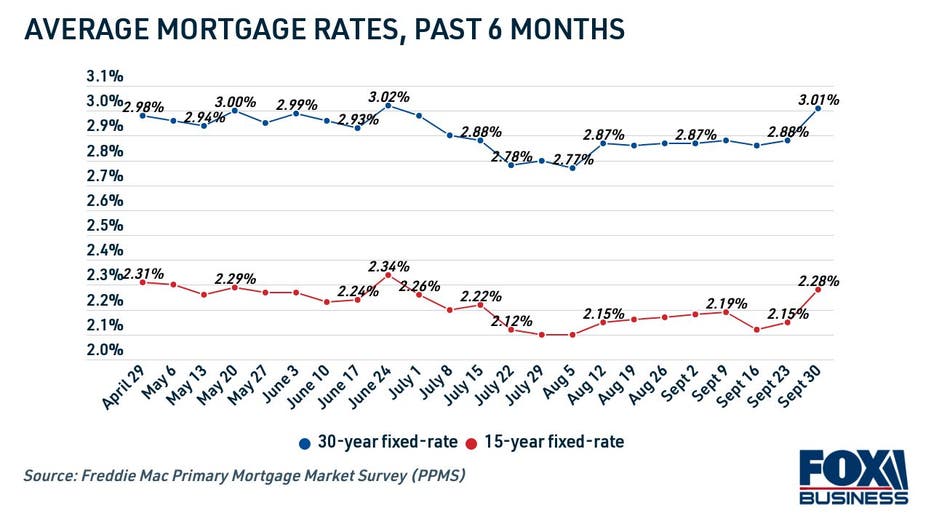

Home values are at an all-time high, and mortgage rates are still hovering near 3%, according to Freddie Mac. These are favorable conditions for homeowners who want to tap into their home equity with cash-out mortgage refinancing.

Cash-out refinancing is when you take out a home loan that's larger than your current mortgage and pocket the difference in a lump sum of cash. Your new mortgage will have different repayment terms, such as interest rate and monthly payment.

A similar way to tap into you're home's equity is to take out a second mortgage in the form of a home equity loan or home equity line of credit (HELOC). These different types of loans allow you to borrow against the value of your home with a new loan, but keep your current mortgage.

The primary drawback of borrowing from your home's equity is that you risk losing the roof over your head if you can't make payments. But borrowing against your home equity typically allows for lower interest rates and less stringent eligibility criteria when compared with unsecured loans such as personal loans.

Get in touch with an experienced loan officer to see if home equity loans, HELOCs or cash-out mortgage refinancing can help you cover expenses.

REVOLVING CREDIT BALANCES REACH PRE-PANDEMIC LEVELS: HERE'S HOW TO PAY OFF CREDIT CARD DEBT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.