Revolving credit balances reach pre-pandemic levels: Here's how to pay off credit card debt

The amount of debt that Americans are carrying has increased, suggesting a return to pre-pandemic spending habits. See how you can pay down credit card debt without having to significantly cut your spending habits. (iStock)

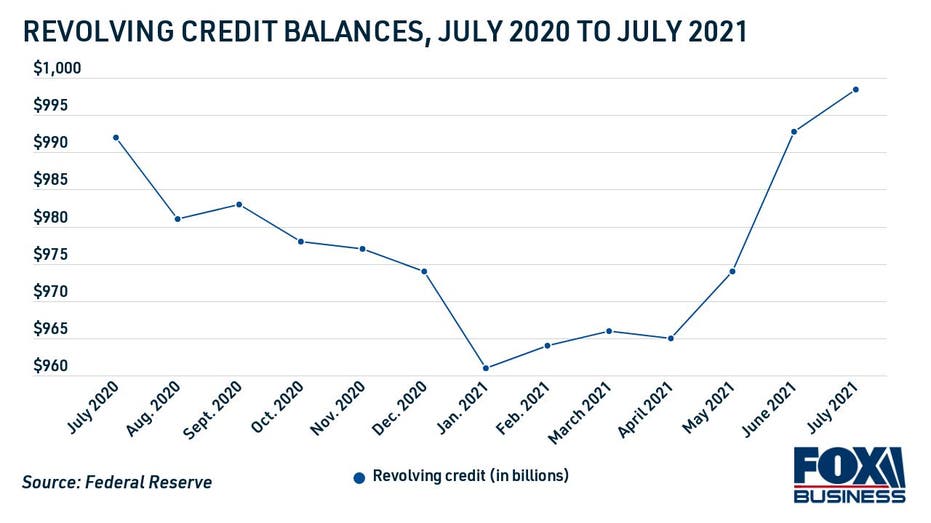

Americans managed to pay down their their credit card debt during the coronavirus pandemic, according to data from the Federal Reserve. But they've since added to their revolving debt balance as a result of using their cards again.

Revolving consumer credit increased at an annual rate of 10.9% in Q2 2021. June was the most significant month for credit card spending — revolving credit increased 22.3% year over year. While spending slowed slightly in July, it's still nearing $1 trillion.

WILL A NEW CREDIT CARD AFFECT MY MORTGAGE APPLICATION?

The last time revolving credit balances were over $1 trillion was in April 2020, before the COVID-19 pandemic slowed consumer spending.

If you're one of the many Americans who increased their credit card spending in recent months, you may be looking for a way to cut expenses. There are several ways to pay off credit card debt fast, such as debt consolidation loans, balance transfers and other debt payoff strategies.

Compare your options in the analysis below, and visit Credible to compare debt consolidation products like personal loans and balance-transfer cards.

STUDENT LOAN DEBT IS PREVENTING MILLENNIALS FROM BUYING A HOME

Use a personal loan to pay off credit card debt

If you make the minimum payment on your credit card debt each month, the outstanding balance increases due to high, variable interest rates. Revolving credit card debt is an expensive burden that can keep you from reaching financial milestones like buying a house or going back to college.

On the other hand, personal loans have low, fixed rates that allow you to pay off your debt on a set timeline. Your monthly payment will always be the same, and you'll know exactly how long it will take to pay off your debt.

The average personal loan interest rate was 9.58% in Q2 2021 per Fed data, assuming a two-year payoff term. In contrast, the average credit card interest rate for all accounts assessed interest was 16.30% during the same period. By qualifying for a lower rate, you can save hundreds of dollars in interest charges while becoming debt-free.

Personal loan rates can vary widely from lender to lender based on the borrower's credit score as well as the loan length and amount. Because of this, it's important to shop around for the lowest interest rate possible to ensure you're getting the best rate for your situation.

You can compare interest rates across multiple lenders without impacting your credit score on Credible. The table below shows estimated personal loan interest rates from real lenders.

DOES HAVING CREDIT CARDS WITH A ZERO BALANCE HURT YOUR CREDIT UTILIZATION?

Open a balance transfer credit card

Another common way to pay down credit card debt is to utilize a balance transfer. This allows you to move the balance of one or more credit cards to another credit card, ideally at a lower interest rate. Better yet, you may be able to secure a 0% APR introductory offer, which allows you to pay down your high-interest credit card debt without paying interest at all.

Keep in mind that introductory periods typically just last a set period of months, which gives you a limited amount of time to pay down the balance during the intro period before interest kicks in. Plus, you'll need a good or better credit score to qualify for the best balance transfer offers.

You'll also be charged a balance transfer fee of around 3-5% of the total balance, although some balance transfer cards do not charge a fee. And consider a credit card's balance transfer limit to ensure it's not lower than the amount you owe.

You can browse balance transfer offers from credit card companies on Credible's online financial marketplace.

HOW DO I BUILD AN EMERGENCY FUND?

Try an expert-approved debt repayment strategy

You can also try paying off credit card debt without taking out another loan or credit card. Two common debt repayment strategies are the debt snowball method and the debt avalanche method.

The debt avalanche strategy can help you save the most money over time. That's because you'll prioritize paying off the credit card balances that have the highest interest rate.

The debt snowball strategy can help you get a kickstart on your debt repayment — you start by paying off the lowest balance, moving onto the next smallest balance and saving the largest credit burdens for last.

Still need help deciding which strategy is most financially beneficial to you? Visit Credible to get answers to all your debt repayment questions.

SENATE BILL TARGETS STUDENT LOANS IN BANKRUPTCY

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.