Millions of Americans fear missing debt payments, NY Fed reports: How to manage your debt

A new report from the NY Fed found that 9.6% of Americans fear they might miss a debt payment in the next few months. Here's how you can get your debt under control. (iStock)

Consumers' expectations for long- and short-term inflation have reached a higher rate than ever before, according to the Federal Reserve Bank of New York's most recent Survey of Consumer Expectations (SCE).

Perhaps equally as concerning, though, is the fact that 9.6% fear they may miss a minimum debt payment over the next three months. Although this represents a slight decrease from the 12-month trailing average of 10.1%, it still shows that millions of Americans feel unequipped to handle their towering debt balances.

But with interest rates historically low across a number of financial products, it may be possible to lower the minimum payment on your loans so you can keep creditors and debt collectors at bay.

Keep reading to learn how to refinance your debts, including credit cards, mortgage and student loans. If you decide that refinancing is right for you, shop around for the lowest possible interest rate for your situation on a number of financial products on Credible — without hurting your credit score.

DEBT SNOWBALL VS. DEBT AVALANCHE METHOD: HIGHEST INTEREST RATES OR SMALLEST DEBTS FIRST?

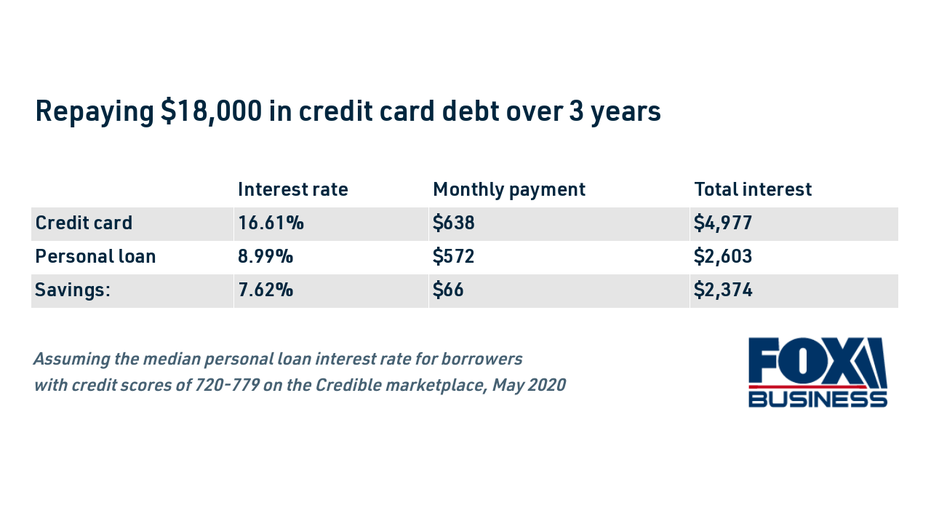

Consolidate credit card debt with a personal loan

High-interest revolving credit card debt can throw your monthly budget off-balance. And if you're making the minimum payment on your credit cards, it can feel impossible to stop your debt from spiraling out of control. Fortunately, there are a few popular ways to pay off credit card debt, including using a personal loan.

Personal loans, also known as debt consolidation loans, are lump-sum loans that you repay in fixed monthly payments over a set period of months or years. Unlike credit cards, personal loan interest rates are fixed, and your monthly payment will always be the same — and you'll know exactly when your debt will be repaid in full.

Personal loans also offer lower interest rates than credit cards. The average rate on a two-year personal loan was 9.58% in Q2 2021, according to the Federal Reserve, compared with 16.30% for credit card accounts assessed interest.

Lower interest rates can lead to lower monthly payments and significant savings on interest charges. Borrowers who consolidated their credit card debt into a personal loan using Credible can save an average of $66 on their monthly payment and $2,372 on interest over time.

3 EASY WAYS TO CUT EXPENSES AS EVICTION MORATORIUM, UNEMPLOYMENT BENEFITS EXPIRE

Determine your new monthly debt payment using Credible's personal loan calculator to see if credit card consolidation is right for you.

HOW TO PLAN FOR UNEXPECTED EXPENSES — AND STILL SAVE

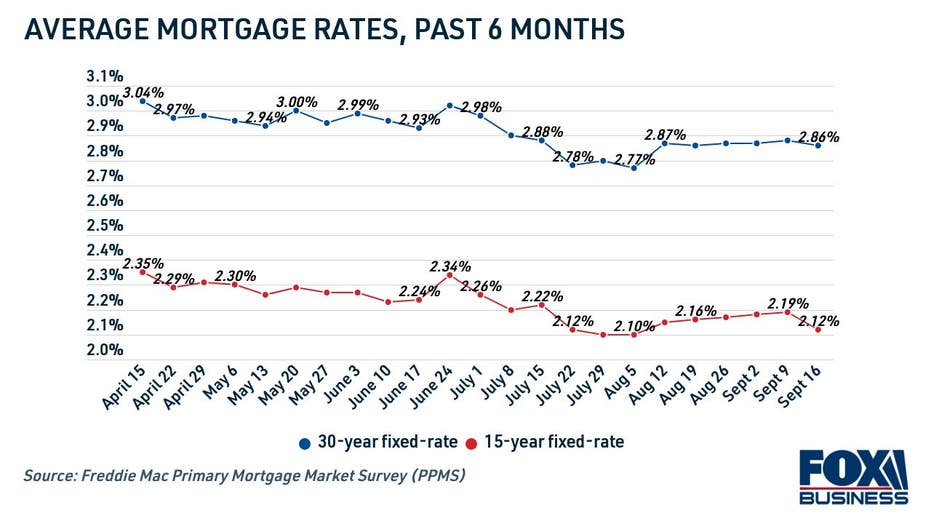

Lock in a record-low mortgage rate by refinancing

Millions of homeowners haven't yet taken advantage of record-low mortgage rates by refinancing, but there's still plenty of time to do so. Mortgage rates are still near historic lows, steadily hovering below 3% according to Freddie Mac. And with the end of a pandemic-era adverse refinancing fee, mortgage refinancing is now cheaper than ever.

HOW DO BALANCE TRANSFERS AFFECT YOUR CREDIT REPORTS?

Refinancing to a lower mortgage rate can help you save a significant amount of money on interest, pay off your home loan faster and even lower your monthly payments.

In one example, homeowners have the potential to save more than $300 on their monthly mortgage payment by refinancing to a new 30-year mortgage. Use a mortgage payment calculator to see how much you can save by refinancing your home loan.

One factor to consider is mortgage refinancing closing costs. These will cost about 1.5% of the mortgage balance are typically rolled into the total amount of the loan.

It's important to shop around with multiple mortgage lenders to get the lowest possible interest rate for your situation. You can compare mortgage refinance rates in just minutes on Credible.

HOW TO GROW YOUR RETIREMENT SAVINGS WITH MINIMAL RISK

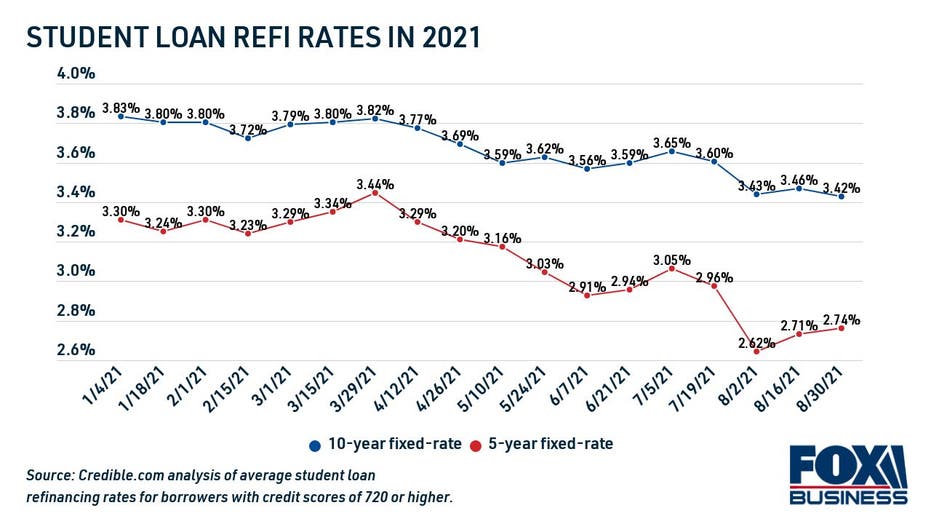

Refinance your student loans to lower your monthly payments

Student loan refinancing is similar to mortgage refinancing in that you're taking out a new loan with better terms to replace your current loan. And like mortgage rates, private student loan rates are still near all-time lows, per Credible data.

HOW DO I BUILD AN EMERGENCY FUND?

Creditworthy borrowers who refinanced to a longer-term student loan on Credible lowered their monthly payments by more than $250, all without increasing the overall cost of borrowing. Use Credible's student loan refinance calculator to see how much you can save on your monthly payment.

Federal student loan borrowers should be aware that refinancing a federal student loan into a private loan will make them ineligible for federal protections like income-driven repayment plans, administrative forbearance and student loan forgiveness programs.

Not sure if refinancing your loans is a smart move? Get in touch with an experienced loan officer at Credible who can guide you through the process and help you determine if refinancing is right for you.

HOW DEBT MANAGEMENT PLANS THROUGH A CREDIT COUNSELOR CAN HELP PAY OFF YOUR LOANS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.