Average personal loan interest rates remain low, so how can you get a good rate?

Learn about the average rates on a personal loan, as well as eligibility requirements, mortgage lenders, loan amounts, and monthly payments. (iStock)

Personal loans offer lump-sum funding that's disbursed directly into your bank account and repaid in monthly installments over a set period of months. Their interest rates are fixed, meaning they won't rise unexpectedly. This is in contrast to credit cards, which may have higher, variable interest rates.

These loans are typically unsecured, meaning they don't require you to put an asset up as collateral. Because of this, personal loan lenders rely on your financial history — including your credit score and debt-to-income ratio — to determine eligibility and set interest rates.

Personal loan interest rates are relatively low right now, making it a good time to pay off debt or finance home improvements. Read on to learn more about getting a good interest rate on a personal loan, and visit Credible when you're ready to start loan shopping.

WHAT IS A GOOD INTEREST RATE ON A PERSONAL LOAN?

Personal loan rates are at their lowest point in years

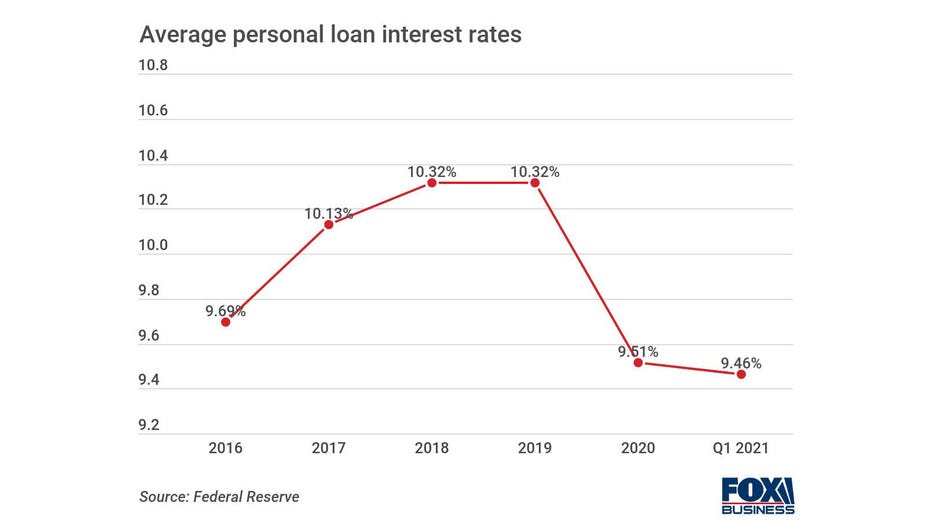

Personal loan interest rates typically range between 4% and 36%, with an average of 9.46% for a 24-month loan, according to the Federal Reserve. In contrast, the average interest rate on a credit card account that's assessed interest is 15.91%. Over the past few years, interest rates rose slightly before dropping in 2020 and Q1 2021. See how they've fluctuated in the chart below:

How to get the best interest rate on a personal loan

Personal loan interest rates vary widely based on a number of factors, including your credit score and debt-to-income ratio, as well as the loan amount and length of the loan. Here are a few steps you can take to get the best possible deal on a personal loan:

- Check and monitor your credit score

- Lower your debt-to-income ratio

- Get prequalified through multiple lenders

- Keep an eye out for other personal loan fees

WHEN TO USE A PERSONAL LOAN OVER A CREDIT CARD

Check and monitor your credit score

A good credit score is typically 670 or higher, as defined by the FICO scoring model. If your credit score is 669 or lower, you should consider working on building your credit before applying for a personal loan to ensure you can get a competitive interest rate.

Get a free copy of your credit reports from all three credit bureaus by visiting www.AnnualCreditReport.com. Below are a few ways to boost your credit:

- Pay down a sum of credit card debt: This can have an immediate positive effect on your credit score by lowering your credit utilization ratio.

- Open a secured credit card: This can help you build credit while using a small amount of savings as collateral.

- Check your credit reports for accuracy: If there's an error, like an inaccurate missed or late payment, you can dispute it to boost your credit score.

You can also get credit monitoring services for free — with no effect on your credit score — through Credible.

Lower your debt-to-income ratio

Your debt-to-income (DTI) ratio is the amount of debt, including student loans and auto loans for instance, you have borrowed relative to your income. Your DTI ratio should be below 35% to be eligible for the lowest personal loan rates.

You can lower your DTI ratio by either increasing your income or paying down a chunk of debt. You can use cash windfalls, like a stimulus check or tax refund, to decrease your DTI with little effort.

SOME OF THE BEST PLACES TO GET A PERSONAL LOAN

Get prequalified through multiple lenders

Personal loan prequalification lets you check your loan eligibility and potential interest rate with a soft credit pull, which won't affect your credit score. This way, you can shop around for the lowest possible interest rate for your unique situation.

Not all lenders offer prequalification, but since there's no cost or effect on your credit score, it's still good to check your potential rates through the lenders that do.

You can get prequalified through multiple lenders at once and compare rates by filling out just a single form on Credible's online loan marketplace.

16 OF THE BEST PERSONAL LOANS IN 2021

Keep an eye out for other personal loan fees

Your interest rate isn't the only measure of how much your personal loan will cost. You should also consider any other costs, like a loan origination fee or prepayment penalty.

Personal loan origination fees are a percentage of the total cost of the loan, and they can be taken from the total balance or added on top. They typically range from 1%-8%, but some personal loan lenders don't charge an origination fee.

Prepayment penalties are assessed if you repay the loan before the term expires. However, prepayment penalties are becoming less common on personal loans. It's still good to read the fine print to check for a prepayment penalty if you plan on paying off your loan early.

The annual percentage rate (APR) on your personal loan will include the interest rate as well as any fees, so it's a more accurate measure of the cost of a loan than an interest rate alone.

Use Credible's personal loan calculator to see how your monthly payments and total loan cost fluctuate with interest rates. While you're there, shop around for the lowest interest rates for your situation.

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.