Average personal loan interest rates drop to lowest level of 2021, Fed reports

How to lock in a low rate

Personal loans can come with a range of rates depending on a borrower's creditworthiness. Here's how you can take advantage of low average personal loan rates. (iStock)

Personal loan rates are lower now than they've been all year, according to the Federal Reserve. This is good news for consumers who want to use a personal loan to consolidate debt, finance home improvements or pay for large expenses.

The average interest rate on a two-year personal loan fell to 9.39% in Q3 2021, according to the Fed's report, compared to 9.58% in Q2 and 9.46% in Q1. But just because the average personal loan interest rate remains low doesn't mean all borrowers will qualify for a low rate.

Keep reading to learn more about how personal loan rates are determined and how you can qualify for a good interest rate. When you're ready to apply for a personal loan, compare rates across personal loan lenders without impacting your credit score on Credible.

15 BEST DEBT CONSOLIDATION LOANS FOR FAIR CREDIT

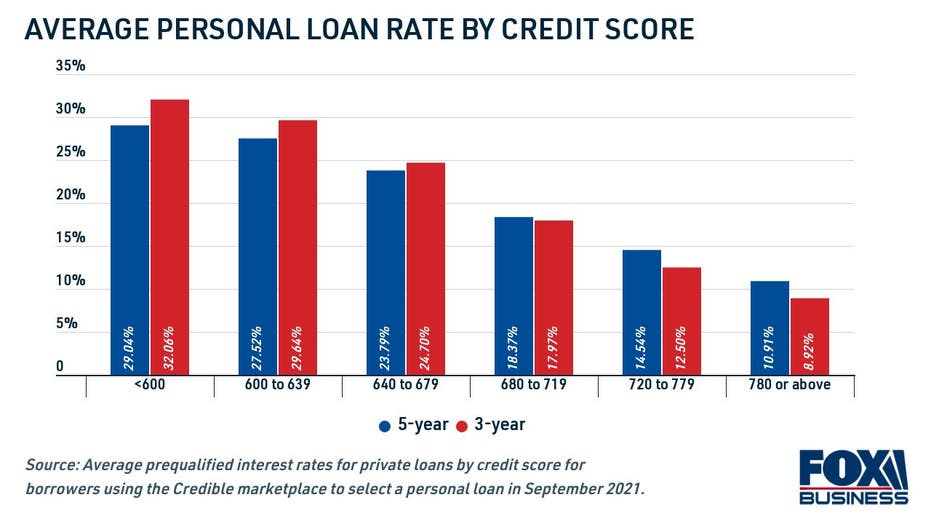

How are personal loan interest rates determined?

Personal loans are typically unsecured, which means they don't require you to put up an asset as collateral in the event you don’t repay the loan. Without collateral, lenders must use a borrower's credit history to determine their likelihood of default.

Lenders judge your financial responsibility using your credit score and debt-to-income ratio (DTI). Borrowers with bad credit and high DTI are historically less likely to repay the loan in full, which makes it a riskier bet for the lender. On the other hand, borrowers with good credit and a low DTI are safer investments for lenders, which grants them a better chance of being approved at a lower interest rate.

In addition to your credit score, there are a few other factors personal loan lenders consider when setting interest rates: the loan amount and the loan length. A personal loan with a larger loan amount and short repayment term may come with a much higher interest rate than a small loan that's spread across a longer term of monthly payments.

Plus, your interest rate is just one factor in calculating the total cost of a personal loan. You'll want to look at the annual percentage rate (APR), which is the total cost of borrowing the loan, including the interest rate and origination fees. Some personal loan lenders don't charge an origination fee. In this case, the APR is the same as the interest rate.

You'll also need to consider if a personal loan lender charges prepayment penalties, which are assessed if you pay off your personal loan before the loan term expires. Many lenders don't charge these penalties, though, so be sure to look through the loan offer if you plan on paying off your personal loan early.

Browse estimated personal loan APRs and loan terms from real lenders in the table below, and visit Credible to see personal loan rates tailored to you.

REVOLVING CREDIT BALANCES REACH PRE-PANDEMIC LEVELS: HERE'S HOW TO PAY OFF CREDIT CARD DEBT

How to lock in a low personal loan rate

While the average interest rate on a personal loan remains low, that's not the case for all borrowers. To qualify for the best personal loan interest rates, you'll need to exceed a lender's minimum credit score requirements and prove you're a creditworthy borrower. Here are a few ways to qualify for a lower rate on a personal loan.

HOW DOES PAYDAY LOAN CONSOLIDATION WORK?

Request a copy of your credit report

Your credit report is an in-depth look at your financial well-being as a borrower. It includes all the debts that are taken out in your name, your loan amounts and interest rates and your on-time payment history. It's important to take a close look at your credit report to see where you have room for improvement and check for errors.

You can get a free copy of your credit report from all three credit bureaus on www.AnnualCreditReport.com.

HOW TO SAVE MONEY ON YOUR PERSONAL LOAN — AND PAY OFF YOUR DEBT FASTER

Work on building your good credit score

A lower credit score directly translates to higher personal loan interest rates and vice versa. Borrowers with excellent credit will have the best chance at scoring a personal loan with lower interest rates. If you have bad credit, work on building your score before applying for a personal loan using these strategies:

- Continue making on-time payments.

- Pay down credit card debt to lower your credit utilization rate.

- Open a secured credit card to build your score fast.

You should also enroll in a credit monitoring service to ensure identity thieves don't open credit accounts under your name and use your credit negatively. You can get free credit monitoring services on Credible.

BORROWERS WHO CONSOLIDATED CREDIT CARD DEBT SAVED $2K+ ON AVERAGE, DATA SHOWS

Keep your debt-to-income ratio low

Your debt-to-income ratio (DTI) is the amount of debt you have in your name relative to your annual income. To calculate your DTI, use this formula: Total monthly debt divided by gross monthly income multiplied by 100.

You should look at keeping your DTI ratio below 35% to qualify for a number of financial products, including mortgages, private student loans and personal loans.

HOW STUDENT LOANS AFFECT YOUR DEBT-TO-INCOME RATIO

Compare the best personal loan rates across multiple lenders

Average personal loan rates can vary from lender to lender. For example, a credit union or online lender may offer lower personal loan rates than a traditional bank. Because of this, it's important to compare interest rates from multiple sources to ensure you're getting a good rate.

Many banks and online lenders let you check your personal loan interest rate without impacting your credit score through a process called prequalification. This way, you can browse estimated rates and formally apply through the lender that presents the best offer.

You can view personal loan prequalification offers across multiple lenders all in one place on Credible. Once you have a good idea of your interest rate, use a personal loan calculator to estimate your monthly payment.

HERE'S WHY VARIABLE-RATE STUDENT LOAN REFINANCING MAY BE A GOOD MOVE

Consider a secured loan as an alternative to a personal loan

Since personal loan rates are so heavily dependent on a borrower's credit score, consumers with fair or poor credit should consider secured loans as a borrowing alternative. There are several types of secured loans that offer cash funding:

- Secured personal loans. Some personal loan lenders will offer auto-secured loans to borrowers who wouldn't otherwise qualify for a loan. In this case, you use your car title as collateral to get a lower rate — but if you don't repay the loan, creditors can seize your vehicle to recuperate the cost of the loan.

- 401(k) loans. Some 401(k) plans allow consumers to borrow from their account balance. Since you're borrowing from your own retirement savings, you don't need to submit to a credit check. Interest rates are typically low, which makes them a good option for low-cost borrowing. But you may be subject to early withdrawal fees, and you risk overborrowing from your retirement nest egg.

- Cash-out mortgage refinancing. Mortgage rates are near historic lows, according to Freddie Mac, which makes it a good time to refinance your mortgage to a lower rate. And with home equity near record highs, you may be able to borrow a mortgage that's larger than what you owe on your current home loan and pocket the difference in cash. Since this is a secured loan, though, you risk losing your home if you can't repay your new mortgage.

Secured loans can be a good borrowing option for borrowers who otherwise wouldn't qualify for an unsecured loan, but they come with the added risk of losing any assets you put up as collateral. Get in touch with a knowledgeable loan officer from Credible to learn more about your secured fixed-rate loan options, such as cash-out mortgage refinancing.

STUDENT LOAN REFINANCING RATES FOR FIXED-RATE LOANS STICK AT HISTORICAL LOWS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.