3 in 4 online shoppers experience buyer's remorse, survey says

About a third of consumers said they regret overspending while shopping online

Online shopping can result in impulse purchases and the temptation to overspend, keeping consumers from meeting their financial goals, according to a new survey. (iStock)

While online shopping is a convenient way to purchase the items you need and compare prices across retailers without leaving the comfort of your home, survey data said that it can also lead to poor spending habits.

Nearly three-quarters (74%) of online shoppers have experienced buyer's remorse, according to a recent survey from the coupon search website Slickdeals.

The most commonly held regret was that an item's value was less than expected for the price (39%), followed by not really using an item purchased online (34%). About a third (32%) of consumers said they regret spending too much money while shopping online.

If you're feeling the urge to splurge, keep reading for tips on how to curb overspending habits. Plus, learn more about how to manage your credit card debt. One strategy is credit card consolidation, which is when you pay off high-interest credit card debt with a fixed-rate loan. You can learn more about personal loans for debt consolidation on Credible.

3 WAYS INFLATION IS IMPACTING YOUR WALLET, AND HOW TO COMBAT RISING PRICES

How to practice healthy spending habits while shopping online

One of the most common regrets held by consumers was that they spend too much money while shopping online, the survey said. If you share this sentiment, check out these tips from the credit scoring company, FICO, to help you stop overspending online:

- Don't shop online when you're in a bad mood. Get in a clear headspace before whipping out your credit card to avoid unnecessary spending. You may also want to steer clear when you’ve been drinking – about six in 10 consumers admitted that they shop online while inebriated, according to Slickdeals.

- Wait a day before making a purchase online. Move the item out of your shopping cart and into a list to save it for later. If you still need the item in the following days, think hard about whether the purchase is worthwhile.

- Avoid buy now, pay later (BNPL). Installment financing options like BNPL can tempt you to overspend on a purchase you can't really afford. And if you miss a BNPL payment, it could result in damage to your credit score.

- Make a shopping list with spending limits. Just like grocery shopping, you should come prepared with a detailed list of the items you need, so you can avoid impulse buying the ones you don't. Also, set a dollar limit for how much you're willing to spend per item.

- Set aside money for a "splurge fund." This separate account can come from birthday money, work bonuses or other cash windfalls. If you need some retail therapy, you can tap into this extra cash reserve instead of relying on credit or dipping into your emergency savings.

As an added bonus, you can put your rainy day fund in a high-yield savings account and watch the balance grow over time with interest. You can visit Credible's online financial marketplace to compare savings rates across multiple banks at once.

5 MONEY TIPS TO REACH YOUR SAVINGS GOALS

What to do if you're struggling with credit card debt

Shopping online can be a gateway to overspending for consumers who struggle to manage their credit card balances. If you're unable to keep up with your spending behavior, read more about common debt repayment methods in the sections below.

Consider meeting with a credit counselor

Nonprofit credit counseling agencies provide free or low-cost debt management services for consumers who grapple with financial planning.

A credit counselor can analyze your monthly income and expenses to help you create a budget. In some cases, they might enroll you in a debt management plan (DMP) to repay your creditors in fixed installments. Credit counselors may even be able to negotiate with creditors on your behalf to lock in a lower interest rate or waive late fees.

You can find an accredited credit counseling agency in your area on the Department of Justice website.

HOW TO MAXIMIZE YOUR CREDIT CARD REWARDS

Utilize a balance transfer credit card

Credit card balance transfers allow you to move the debt of one or more accounts onto a new card with a lower interest rate. Applicants with excellent credit may even qualify for an introductory 0% APR offer, effectively giving them a period of up to 18 months to repay their debt at zero interest.

However, balance transfer cards are typically reserved for borrowers with a very good credit score, defined by the FICO model as 740 or higher. Consequentially, debtors with fair or bad credit may not qualify. Plus, many credit card companies charge a balance transfer fee, typically between 3% and 5% of the amount being transferred.

You can visit Credible to compare balance transfer credit cards for free without impacting your credit score.

RENT PRICES SURGE ACROSS THE COUNTRY, REPORT FINDS

Consolidate credit card balances into a fixed-rate loan

Credit card consolidation allows borrowers to consolidate multiple higher interest debts into a single monthly payment with a personal loan. According to the Federal Reserve, personal loans typically offer lower rates than credit cards — that means you may be able to save money in interest charges, pay off debt faster and reduce your monthly debt payments with debt consolidation.

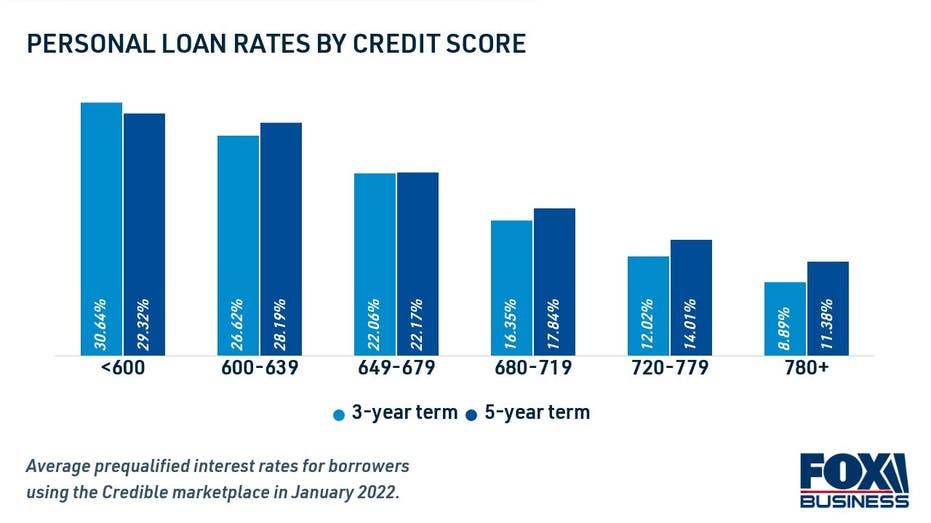

Personal loan lenders determine interest rates and eligibility based on the loan length and amount, as well as a borrower's creditworthiness. Applicants with good credit and a low debt-to-income ratio (DTI) will qualify for the lowest interest rates available, while those with fair credit or worse may not qualify at all.

Most lenders let you prequalify to see your estimated interest rate with a soft credit check, which won't impact your credit score. You can prequalify through multiple lenders at once on Credible's personal loan marketplace.

DEBT COLLECTORS CAN NOW CONTACT YOU THROUGH TEXT, EMAIL AND SOCIAL MEDIA

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.