3 ways inflation is impacting your wallet, and how to combat rising prices

Prices on consumer goods have caused uncertainty while the economy recovers from the COVID-19 pandemic. Here's how inflation can impact your finances in the long run, and how you can protect your assets. (iStock)

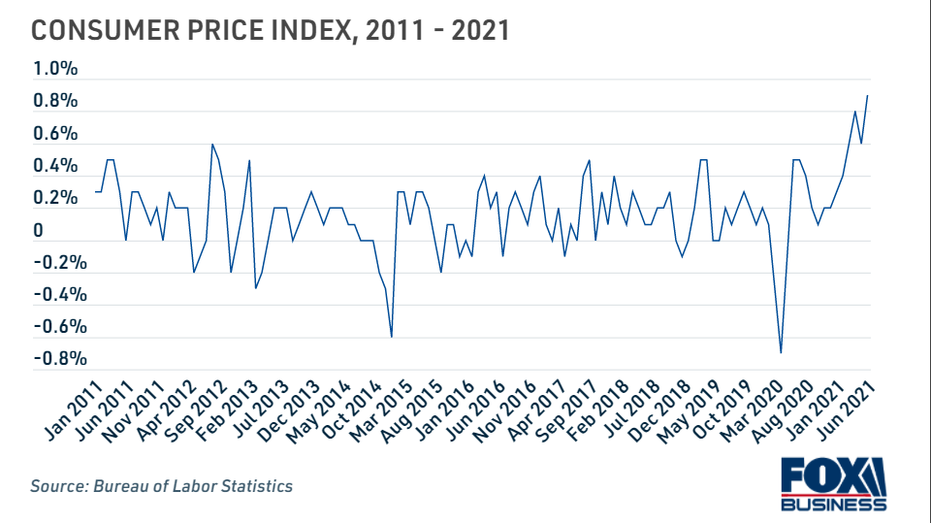

Inflation happens when the price of goods and services increases, which reduces the purchasing power of the dollar. Prices on commodities increased 5.4% over the past year, according to the June 2021 Consumer Price Index (CPI), one measure of inflation reported by the Bureau of Labor Statistics (BLS).

One obvious consequence of inflation is that it increases the general level of prices, but high inflation can impact your finances in a number of ways, from rising interest rates to deflating savings. Keep reading to find out how inflation affects your wallet, and how to combat these effects.

You can shop around for a wide variety of financial products on Credible's online marketplace to make sure you're prepared to offset inflation.

HERE’S HOW COVID-19 CHANGED THE MORTGAGE PROCESS

1. Inflation can cause interest rates to rise

The Federal Reserve uses indicators like the CPI to decide how to set interest rates during its Federal Open Markets Committee (FOMC) meetings. In order to keep inflation in check, the Fed may implement an interest rate hike, which would make sense in today's environment of swift inflation. In fact, the Fed has predicted two rate hikes by 2023, which will inevitably result in a higher rate on a number of financial products.

While increasing savings rates will be welcome news for some, increasing mortgage rates will drive up the cost of homeownership. Consumers have been enjoying record-low mortgage and refinance rates for the past year or so, but the time to secure a good mortgage rate is running out. The Mortgage Bankers Association (MBA) predicts that 30-year mortgage rates will rise to 4.3% in 2022 and 4.9% in 2023.

What you can do now: Refinance your mortgage and other debts while interest rates are still low. Mortgage refinancing can help you lower your monthly payments and save money over the life of your home loan by locking in a historically low interest rate. Plus, with the recent elimination of a pandemic-era refinancing fee, mortgage refi is more affordable than ever.

Browse rates from real mortgage lenders in the table below, and visit Credible to find your mortgage rate without impacting your credit score.

HOW THE CORONAVIRUS PANDEMIC CAN IMPACT YOUR PERSONAL FINANCES

2. Inflation can throw your budget off-balance

When consumer prices rise, so does your spending on most everyday items. You'll have to adjust your monthly budget when it comes to consumer goods like groceries, household essentials and clothing — you might even see your insurance premiums, utility costs and energy prices increase as well.

This can be even more consequential if you aren't earning higher wages. Instead of looking for ways to cut spending on necessary items and decrease your standard of living, look for ways to decrease other debt payments while interest rates are still low.

What you can do now: See if you could benefit by refinancing your student loans. Private student loan refinance rates are near all-time lows, which means you may be able to secure a better interest rate on your college debt and lower your monthly payments. Borrowers who refinanced their student loans to a longer term on Credible saved more than $250 per month on their student loan payment.

While it's not recommended that you refinance federal student loans, since doing so would make you ineligible for forbearance and even student loan forgiveness, refinancing your private student loans is a good move right now. Compare student loan refinance rates on Credible's online loan marketplace.

BIDEN 'EXTREMELY OPTIMISTIC' ABOUT MAY JOBS REPORT, ECONOMISTS LESS SO

3. Inflation can dampen your savings over time

It's smart to put aside money in savings to use as an emergency fund when unexpected financial matters arise. But if your cash is sitting in a low-interest savings account, future inflation will outpace the growth of your savings rather quickly.

No matter how much you invest, the amount you save is likely to lose value over time because of inflation — and that problem is exacerbated if you carry loads of revolving credit card debt. Revolving debt increased 11.4% in May 2021 alone, suggesting that many consumers are relying on credit cards as a result of inflation. This interest-bearing debt practically reverses any investment you have, because you're paying sky-high interest rates on whatever credit card balance you have.

What you can do now: Pay off high-interest credit card debt to make your savings and investments work harder for you. There are several ways to get rid of credit card debt, including personal loans for debt consolidation. Personal loans have fixed repayment terms and typically have lower interest rates than credit cards. They're unsecured, so lenders determine your eligibility and personal loan rate based on your credit score and debt-to-income (DTI) ratio.

If you're considering consolidating debt with a personal loan, it's important to shop around to make sure you're getting the best possible interest rate for your financial situation. Use the calculator below to see how much you can save on your credit card debt, and visit Credible to compare personal loan interest rates across multiple lenders in just minutes.

JEROME POWELL BELIEVES HIGH INFLATION RATE IS TEMPORARY – HOW ARE INTEREST RATES AFFECTED?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.