IRS updates guidance on 1099-Ks: What to know

The updated IRS FAQ document provides answers to a number of common questions about Form 1099-K.

Kevin Hassett blasts new IRS tax-reporting rule: The IRS is buying the option to harass all Americans

Former Chair, Council of Economic Advisers Kevin Hassett discusses the IRS postponing its tax rule on Venmo and PayPal payments over $600 and concerns of overreach on 'Kudlow.'

The Internal Revenue Service (IRS) released an updated frequently asked questions document for taxpayers and tax professionals this week regarding Form 1099-K, which is used to report income for self-employed workers and people who sell personal items or receive funds from third-party organizations.

Aside from answering a number of frequently asked questions from taxpayers about the Form 1099-K, the updated IRS document emphasizes the agency's recent announcement that calendar year 2022 will be considered a transition year for a new rule that lowered the reporting threshold to $600.

That change, enacted under the Democrats' American Rescue Plan Act, threatens to impact millions of Americans who use third-party apps like PayPal and its subsidiary Venmo to send or receive money—but it won't be in effect for the upcoming tax season.

You should not receive a 2022 1099-K unless you have gross payments over $20,000 and over 200 transactions. However, some taxpayers may receive a Form 1099-K in error at the lower threshold early next year despite the change due to the timing of the delayed implementation announcement in late December.

IRS DELAYS NEW TAX-REPORTING RULE ON VENMO, PAYPAL PAYMENTS OVER $600

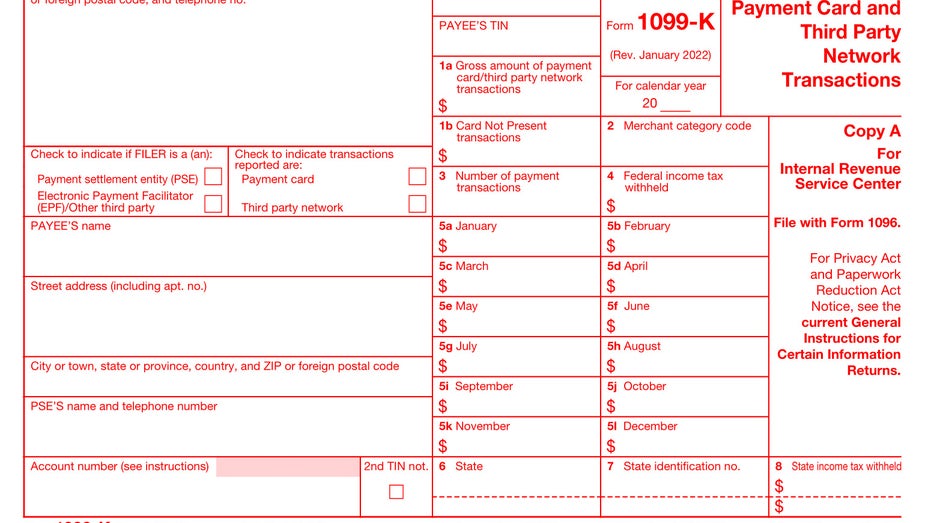

IRS Form 1099-K

The IRS' updated FAQ helps taxpayers understand why they're receiving Form 1099-K and what types of income and transactions need to be reported on the form. Here's a look at some of the key takeaways:

Does a gain or loss on the sale of a personal item need to be reported on Form 1099-K?

Gains on the sale of personal items are considered taxable income and need to be reported to the IRS on Form 1040 Schedule D, which is the capital gains and losses section of the individual income tax return; and Form 8949, which reports the sale and disposition of capital assets.

The proceeds from a sale could be also reported on Form 1099-K. The IRS FAQ used an example in which a taxpayer received $900 for tickets that cost $500. The 1099-K will show $900. It's up to the recipient to show a $400 gain on Schedule D and Form 8949. Without proper reporting the IRS may assume the entire amount taxable.

Losses on the sale of a personal item aren't tax-deductible, and if a taxpayer receives a 1099-K for a sale that resulted in a net loss, they would need to make off-setting entries to report the cost of the item and income received on Schedule 1 of Form 1040. You can only report your costs up to the amount of your proceeds, so if you bought an item for $1,000 and sold it at a loss for $600, you would list $600 as the sale price in one part of Schedule 1 and write "Form 1099-K Personal Item Sold at a Loss…. $600" to zero out your entry on another line of Schedule 1.

5 THINGS TO KNOW ABOUT YOUR 2023 TAXES

The reflection of a pedestrian is seen walking past an Internal Revenue Service (IRS) office building in the East Harlem neighborhood of New York, U.S., on Saturday, June 24, 2017. (Photographer: Timothy Fadek/Bloomberg via Getty Images / Getty Images)

If I have a holiday craft business, will I get a Form 1099-K?

The IRS says that a person with a holiday craft business may receive a Form 1099-K based on the type of transactions.

If you accept payment cards, like credit or debit cards, you'll receive a Form 1099-K for the gross amount of payments made to you through payment cards for the calendar year. This reporting requirement hasn't changed and there isn't a minimum threshold for payments like this to trigger the reporting requirement.

You may also receive a Form 1099-K if you accepted payments from a third-party settlement organization where the number of transactions exceeded 200 and the aggregate amount of payments received exceeded $20,000 for a calendar year.

Does using a credit card to make purchases for a small business and not-for-profit hobby trigger a 1099-K report?

The IRS says a small business owner or not-for-profit hobbyist who doesn't accept payment cards but does use a credit card and third-party settlement organization to buy goods, materials or supplies shouldn't receive a Form 1099-K for their purchases.

FINANCIAL NEW YEAR'S RESOLUTIONS FOR 2023

A man enters the Internal Revenue Service (IRS) building in Washington, D.C., U.S., on Friday, May 7, 2010. (Photographer: Andrew Harrer/Bloomberg via Getty Images / Getty Images)

Who is responsible for reporting transactions?

For payment card transactions, the merchant that transfers funds to the participating payee is responsible for reporting the gross amount of reportable transactions. This can be outsourced to a processor that may share a contractual obligation

When it comes to third-party settlement transactions, the third-party organization or its electronic payment facilitator is responsible for reporting gross amounts of reportable transactions paid to the participating payees in their network.

Who should taxpayers contact if they have questions about their Form 1099-K?

The IRS says that taxpayers who have questions about information on a Form 1099-K they received should contact the filer. Contact information for the filer can be found in the upper-left corner of the form.

If a taxpayer doesn't recognize the filer, they should reach out to the payment settlement entity whose name and phone number can be found in the lower-left corner of the form above their account number.

What will happen once the lower threshold $600 threshold takes effect?

As previously noted, the third-party transaction threshold won't be lowered to $600 for the 2022 calendar year, but it is expected to be in effect for the 2023 calendar year—meaning it will be something taxpayers have to deal with when they file 2023 returns in 2024 unless the IRS issues another delay or Congress moves to modify the threshold.

Once the implementation delay concludes and the new rule takes effect, the reporting threshold will drop from gross payments exceeding $20,000 with over 200 transactions to a threshold of $600.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

IRS to begin sending 1099-K forms for some payments

Sen. Mike Braun, R-Ind., explains the details regarding the IRS starting to send out 1099-K forms for some payments on ‘Fox Business Tonight.’