43% of seniors grapple with higher debt payments as Fed raises interest rates, survey finds

Here are 3 ways seniors can pay off credit card debt

Social Security benefits may not be sufficient for seniors struggling to keep up with debt payments, according to a new survey from The Senior Citizens League. (iStock)

In March, the Federal Reserve implemented the first of several interest rate hikes planned for 2022 to offset rising consumer prices. But at a time when inflation is rising at its fastest pace in 40 years, the Fed's economic policy may drive borrowing costs higher for seniors — many of whom rely on a fixed Social Security income.

About two in five seniors (43%) carry revolving credit card debt, according to a new survey from advocacy group The Senior Citizens League (TSCL). What's more, about half (49%) of respondents have spent their savings or have no emergency fund at all.

"Credit card debt in retirement can quickly get out of hand, and this is especially true during periods when interest rates climb," said TSCL Policy Analyst Mary Johnson.

Keep reading to learn how the Fed's benchmark rate hikes will impact the cost of living for America's seniors, as well as how you can reduce your credit card balances. One strategy is to consolidate high-interest credit card debt into a fixed-rate personal loan. You can visit Credible to compare credit card consolidation loan rates for free without impacting your credit score.

RETIREES STRAINED BY HIGHER HOME INSURANCE RATES IN FLORIDA

TSCL: Social Security payments aren't keeping up with inflation

A recent TSCL report found that the 5.9% Social Security cost of living adjustment (COLA) for 2022 isn't sufficient to keep up with rising prices, particularly when it comes to higher health care costs. As inflation continues to "erode Social Security buying power," many seniors are covering expenses with credit card spending.

Federal Reserve Chairman Jerome Powell said the central bank is planning several interest rate hikes this year to combat inflation, which rose 7.9% annually in February — well above the Fed's 2% target. But this move may increase debt payments for seniors who have a fixed Social Security income.

"We are in a steeply inflationary period when rising interest rates will mean many consumers will need to reduce the amount of debt that they are carrying on credit cards month to month in order to keep that cost manageable," Johnson said.

When the Fed raises its benchmark rate, it can cause interest rates to rise on a number of variable-rate borrowing products like credit cards. This can drive the monthly minimum payments higher, making it more difficult for many consumers to afford their credit card bills.

It may be possible for borrowers to reduce their monthly payments and save money on interest through credit card consolidation. This is when you borrow a fixed-rate personal loan to pay off credit card balances in predictable monthly payments over a set repayment period. You can learn more about debt consolidation loans by getting in touch with a knowledgeable loan expert at Credible.

NEARLY 70% OF MEDICAL BILLS IN COLLECTIONS WILL BE REMOVED FROM CREDIT REPORTS

3 ways to pay off credit card debt

Getting out of debt is difficult enough in normal economic conditions, but it may be even harder during inflationary periods when prices are rising on a number of necessary expenses. But as credit card rates are poised to rise, it's more important than ever to find ways to avoid racking up high credit card balances.

"Inflation has many older households struggling to stay afloat," Johnson says. "As difficult as these times may seem right now, it’s important to have a plan to reduce debt — and that would mean putting less on credit cards, and paying more of the balance," Johnson says.

You can read more about how to get rid of credit card debt in the sections below.

1. Nonprofit credit counseling services

Credit counseling agencies offer free or low-cost services to consumers who are struggling to manage their debts. A credit counselor may enroll you in a debt management plan (DMP) to repay your creditors in monthly payments. They also may be able to negotiate with your creditors to reduce the amount of debt you owe, waive late fees and lower your interest rate.

You can find a list of accredited, nonprofit credit counseling agencies on the Department of Justice website.

HOW DEBT RELIEF PROGRAMS CAN HELP PAY OFF YOUR LOANS

2. Balance transfer credit cards

It may be possible to move the balances of one or more credit cards onto a new account with better terms with a balance transfer. This can make it easier to pay off credit card debt in a single monthly payment with a lower interest rate.

Well-qualified applicants may also qualify for a balance transfer card with an introductory 0% APR offer, essentially giving them a period of up to 21 months to pay off credit card debt at zero interest. These offers are typically reserved for those with very good or excellent credit, defined by the FICO model as a credit score of 740 or higher.

It's important to note that you may be charged a balance transfer fee of 3-5% of the total amount being transferred. You can visit Credible to compare balance transfer offers from multiple credit card companies at once.

DEBT COLLECTORS CAN NOW CONTACT YOU THROUGH TEXT, EMAIL AND EVEN SOCIAL MEDIA

3. Credit card consolidation loans

Debt consolidation is when you borrow an unsecured personal loan to repay multiple types of debt at a lower interest rate. Personal loans offer fixed interest rates, which means that your monthly payment and debt repayment terms will stay the same during the borrowing period.

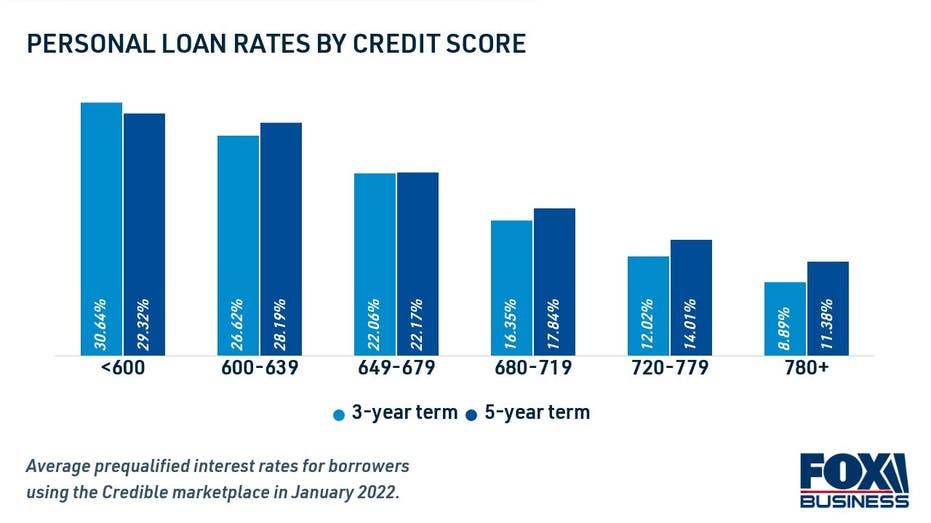

Personal loan lenders determine eligibility and interest rates based on a borrower's creditworthiness. Applicants with good credit and a low debt-to-income ratio (DTI) will see the best possible offers, while those with fair or bad credit may have a hard time securing a personal loan with good terms.

Thankfully, there's good news for consumers who are thinking about using this debt repayment strategy: Personal loan rates reached a record low in March, according to data from Credible. This means borrowers may be able to save more money than ever before by paying off credit card debt with a fixed-rate loan.

You can browse current personal loan rates in the table below, and visit Credible to see offers tailored to you for free without impacting your credit score. That way, you can decide if credit card consolidation is the right debt repayment method for your financial situation.

DON'T FILE BANKRUPTCY ON STUDENT LOANS — DO THIS INSTEAD

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.