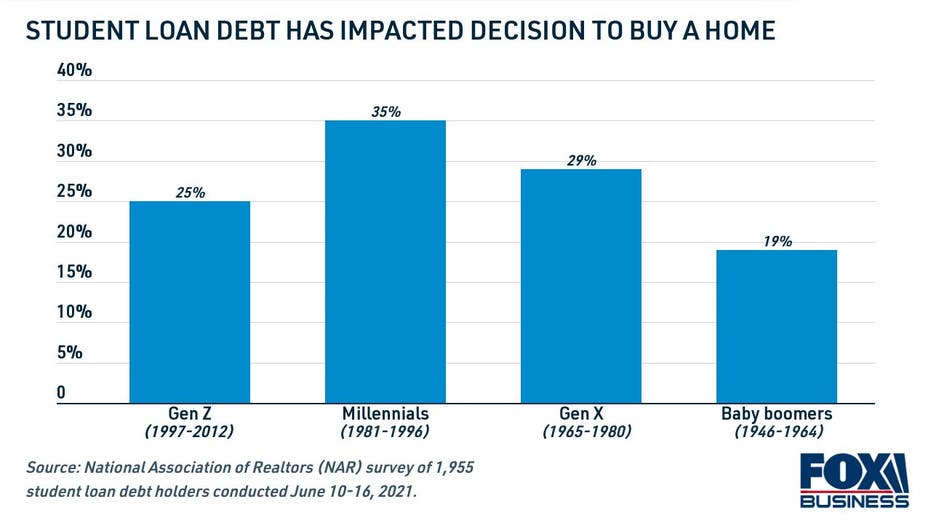

35% of millennials say student loan debt is preventing them from buying a home: survey

See how you can cut down your outstanding student loan balance to achieve the American dream of homeownership. (iStock)

Homeownership can be a stable way to create long-lasting wealth while simply paying your living expenses. But buying a home can be challenging for borrowers who have other significant financial obligations like student loan debt.

Student loan debt has kept 35% of millennial borrowers from purchasing a home, according to a new survey from the National Association of Realtors (NAR). It's also impacted homeownership among the other generations; a fifth (19%) of baby boomers said that student loan debt has prevented them from buying a home.

12 MISTAKES TO AVOID AS A FIRST-TIME HOME BUYER

Thankfully, there are several ways to make your student loan debt more manageable so you can achieve your financial goals. Consider your options such as income-driven repayment plans and student loan refinancing in the analysis below.

If you decide to refinance your student loan debt, be sure to compare interest rates across multiple lenders to ensure you're getting the best interest rate possible for your financial situation. You can compare rates in just minutes without impacting your credit score on Credible.

WHAT YOU NEED TO KNOW BEFORE MAKING A DOWN PAYMENT ON A HOUSE

Student loans influence borrowers' financial decisions

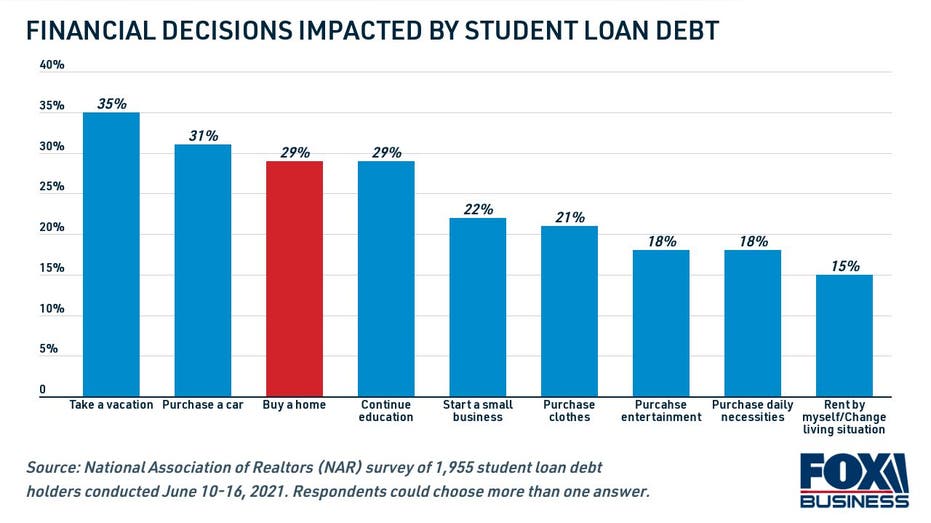

It's clear that student loan payments can stand in the way of the American dream of homeownership. Nearly 30% of all borrowers surveyed said that their student loan debt is holding them back from getting a home loan.

Among all student loan borrowers who do not yet own a home, more than half (51%) said that student loan debt is holding them back from homeownership, and about three-quarters (72%) said student loan debt will delay them from purchasing a home. Among current homeowners, half (50%) said student loan debt delayed their home purchase.

The financial impact of student loans doesn't end there, though. More than a third (35%) of borrowers said their college debt has prevented them from taking a vacation. About 3 in 10 said that student loan debt has impacted their decision to buy a car or continue their post-secondary education.

The financial impact of student loan debt varies across generations. For example, 22% of Gen Z borrowers said their college debt has prevented them from renting on their own and moving out of their parent or guardian's home. It's held 29% of millennials back from starting a small business.

THIS IS THE BEST WAY TO LOWER YOUR MONTHLY MORTGAGE PAYMENT

3 ways to make student loan debt more manageable

You don't have to sacrifice your financial well-being while paying off your student loans. There are several ways to pay off your loans faster, lower your monthly payments and maybe even have your student loan debt fully discharged.

BORROWERS WHO CONSOLIDATED CREDIT CARD DEBT SAVED $2K+ ON AVERAGE

1. Refinance your student loans to a lower rate

Student loan refinancing is when you take out a new loan to pay off your current student loans for better terms. Now is a great time to refinance your college debt, because student loan refinance rates are still hovering near all-time lows, according to data from Credible.

By refinancing to a lower interest rate, you may be able to pay off your debt faster or even lower your monthly payments. Well-qualified borrowers who refinanced to a longer-term loan on Credible saved more than $250 on their monthly payments, while those who refinanced to a shorter-term loan shaved years off their student loan repayment and saved nearly $17,000 on interest.

Keep in mind that refinancing your federal student loans into a private student loan may grant you a lower interest rate, but you'll lose federal benefits like COVID-19 emergency forbearance, income-driven repayment (IDR) plans and even possible student loan forgiveness.

Not sure if refinancing is right for you? Browse student loan rates from real private lenders in the table below, and use Credible's student loan calculator to see how much you can save.

DOES HAVING CREDIT CARDS WITH A ZERO BALANCE HURT YOUR CREDIT UTILIZATION?

2. Enroll in an income-driven repayment plan or apply for additional forbearance

Federal student loan borrowers can enroll in income-driven repayment (IDR), which limits your student loan payments to about 10-20% of your disposable income. You can enroll in an IDR plan on the office of Federal Student Aid (FSA) website.

Federal student loan forbearance ends soon, and payments will restart in February 2022. Still, many borrowers are still not ready to resume federal student loan payments. Eligible federal borrowers may qualify to have their payments paused for an additional 36 months through economic hardship deferment or unemployment deferment.

If you have private loans, you may be able to apply for hardship forbearance. Keep in mind that each lender has its own set of eligibility requirements when it comes to deferment.

HOW STUDENT LOANS AFFECT YOUR DEBT-TO-INCOME RATIO

3. Research student loan forgiveness programs like PSLF and borrower defense

The Department of Education has canceled nearly $10 billion worth of student loan debt for more than 563,000 borrowers since President Joe Biden took office. But that's just a fraction of the 45 million student loan borrowers who owe $1.7 trillion in student loan debt.

The Biden administration has made it easier for borrowers to get their student loans forgiven through the total and permanent disability (TPD) discharge program and the closed school discharge program. But if you don't qualify for these programs, consider your alternative student loan forgiveness options:

- Public Service Loan Forgiveness program (PSLF): Civil servants like teachers, nurses and law enforcement officers who work for a government agency may be eligible to have the remainder of their federal student loan debt discharged after making 120 qualifying payments. PSLF eligibility is notoriously complicated, though, so familiarize yourself with the program requirements.

- Borrower defense to repayment: If your school misled you or engaged in some other sort of misconduct while you were attending, you can apply to have your student loans forgiven through borrower defense. The Biden administration has approved $1.5 billion in borrower defense claims since the president took office.

- Military loan forgiveness programs: The Army, Navy, Air Force and National Guard all have their own student loan assistance programs that offer up to $65,000 in aid. Plus, the Biden administration recently waived student loan interest for 47,000 current and former active-duty service members.

Even if you don't qualify for student loan forgiveness, you still have options for making your student loan debt more manageable. Get in touch with a knowledgeable loan officer at Credible to explore your student loan repayment options, including refinancing.

IF YOU NEED MORTGAGE DOWN PAYMENT ASSISTANCE, CONSIDER THESE OPTIONS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.