Fannie Mae to consider on-time rent payments when underwriting mortgages, which is good news for buyers

Fannie Mae issued new guidelines allowing conventional mortgage lenders to consider an applicant's history of on-time rent payments when issuing home loans. (iStock)

It's about to get easier for homebuyers with a limited credit history to qualify for a mortgage, thanks to a new decision by Fannie Mae to consider an applicant's on-time rent payment history when determining loan eligibility.

Starting Sept. 18, 2021, single-family lenders will be able to automatically identify a pattern of recurring rent payments in an applicant's bank statements during the underwriting process "to deliver a more inclusive credit assessment," according to a press release from Fannie Mae.

It is but one important step in correcting the housing inequities of the past, creating a more inclusive mortgage credit evaluation process going forward, and encouraging the housing system to develop new ways of safely assessing and determining mortgage eligibility in order to fairly serve all potential homeowners.

WHAT YOU NEED TO KNOW BEFORE MAKING A DOWN PAYMENT ON YOUR HOME

This is good news for homebuyers with a limited credit history but a strong record of on-time rent payments. About 20% of U.S. adults have an insufficient credit history, in part because only 5% of renters today have their on-time rent payments reported to the credit bureaus.

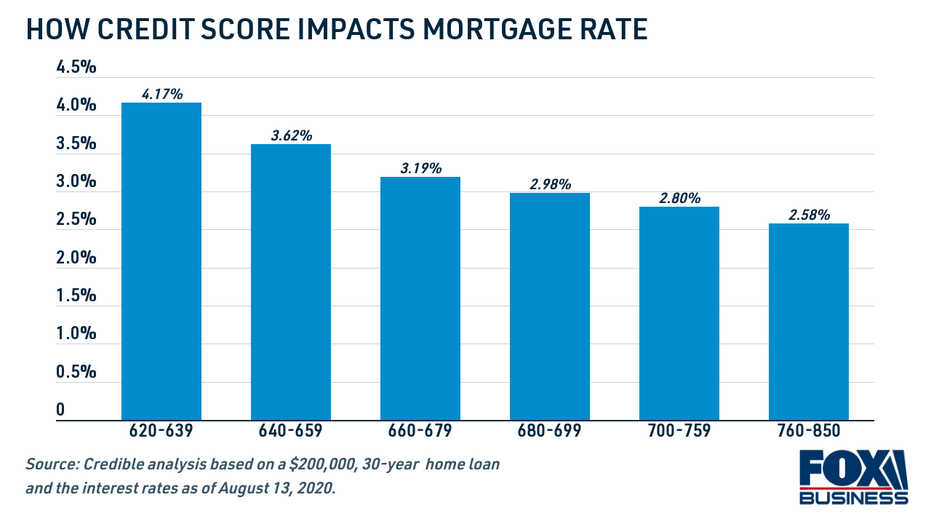

Keep reading to learn more about how your credit score impacts your mortgage eligibility. If you're in the market to buy a home, visit Credible to shop for a mortgage without impacting your credit score.

WHAT ARE THE NEW FHA LOAN LIMITS FOR 2021?

Why is your credit score important when buying a home?

A person's credit score is supposed to be an all-encompassing measure of their fiscal responsibility, but that's not always the case. The credit bureaus (Equifax, Experian and Transunion) expect to see a long history of diverse accounts, making it difficult for young consumers who are apprehensive of credit cards to achieve a good credit score.

But without a robust credit history, it's harder to get access to financial products that help you achieve life's milestones like buying a house. That's because mortgage lenders determine your likelihood of repaying the loan based on your credit score.

Fannie Mae's newest guidelines have the potential to help millions of prospective homebuyers who are able to make their mortgage payments but don't have an established credit history. Research shows that 17% of mortgage applicants who recently did not qualify for conventional loans would have been eligible if their on-time rent payments were considered.

Even with this new underwriting option, though, it may still be difficult for bad-credit borrowers to get approved for a home loan — especially at the lowest rates available. The best mortgage rates with the lowest monthly payments are reserved for mortgage applicants with an excellent credit score and debt-to-income ratio (DTI ratio), according to a Credible analysis.

It's also important to do your research and shop around with mortgage lenders to see what kind of rates you can qualify for. See estimated interest rates for borrowers with scores of 740 or higher in the table below, and visit Credible to compare mortgage rates across multiple lenders.

VETERANS BORROWING VA LOANS AT A RECORD PACE, STUDY SHOWS

Buying a home? Here's how you can build your credit score

Just because it may be possible to qualify for a mortgage without a decent credit history doesn't mean you'll get a good mortgage rate or a high enough loan amount. If you're in the market to purchase a home, it's still a good idea to work on building your credit before you apply for a mortgage. Here are a few ways to improve your credit score:

- Keep paying your bills. On-time payment history is the most significant factor impacting your FICO score, so it's important to keep track of your payments and dispute false late payments on your credit report.

- Pay down credit card debt. Your credit utilization ratio, which is the amount of credit you're using versus the credit you have available, should ideally be below 30%. Try increasing your monthly debt payments.

- Request a credit limit increase. Ask your credit card issuer to increase your credit limit in order to lower your credit utilization ratio. Just be sure not to spend more money since your limit is higher.

- Open a secured credit card. Also known as a credit-builder card, a secured card requires you to make a cash deposit. You can borrow money against those funds to help build your on-time payments.

- Ask to be an authorized user. If you're close with someone who makes consistent on-time credit card payments, being added to their account can bolster your credit score.

Prospective homebuyers should also keep an eye on their credit score during the mortgage process. Credit monitoring can help you stay up-to-date on any changes to your score, so you're not caught by surprise when you're ready to apply for a mortgage. Sign up for free credit monitoring services on Credible.

FREDDIE MAC LAUNCHES NEW HOME RENOVATION MORTGAGE, HERE'S HOW TO GET ONE

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.