40% of millennials say credit card debt is their biggest financial setback, survey finds

Here are three ways millennials can get out of credit card debt

A new survey found that millennials are more financially confident and optimistic than any other generation, but they're held back by high-interest credit card debt. (iStock)

Credit cards come with many benefits, such as providing a way for consumers to earn rewards on their purchases and build their credit scores. But revolving credit card debt that's carried over from month to month can be an expensive burden due to high interest rates.

Two in five millennials (40%) say that credit card debt is their greatest financial setback, according to a new survey from Affirm, a buy now, pay later financing company. Millennials also worry about money an average of 7 times per day, more than any other generation surveyed.

However, the survey also found that millennials feel more financially confident than any other age group, and they're the most optimistic about what their finances will look like ten years from now. Aside from that, 61% of U.S. consumers also believe that living through the pandemic has made the younger generations more financially savvy.

Keep reading to learn more about how to get out of credit card debt, and visit Credible to explore your debt consolidation options.

GETTING OUT OF DEBT IS A TOP NEW YEAR'S RESOLUTION, STUDY FINDS

3 strategies for paying off credit card debt

It's easy to rack up high-interest credit card debt without noticing, especially if you rely on credit cards to cover unexpected expenses like car repairs and surprise medical bills. Recent Federal Reserve data shows that Americans are becoming increasingly reliant on credit cards as revolving credit balances spiked to pre-pandemic levels in Nov. 2021.

If you're struggling to pay off your debt, consider the following debt repayment strategies:

Read more about each method in the sections below.

1. Credit card balance transfer

One popular way to get out of credit card debt is to open a balance transfer credit card. This allows you to move the balance of one or more credit cards onto a new card that you repay on better terms, such as a lower interest rate.

Consolidating with a balance transfer card can help borrowers save money while paying off credit card debt. But keep in mind that some credit card issuers may charge a balance transfer fee worth 3-5% of the amount being transferred. Plus, there may be a limit to the amount that you can transfer.

This method can be especially beneficial for creditworthy applicants who can qualify for 0% APR on balance transfers. These zero-interest offers typically last up to 18 months from account opening — and when the promotional period expires, interest is charged on the remaining balance.

Zero-interest balance transfer offers give borrowers the ability to pay off their credit card balances without paying any interest. However, these offers are reserved for applicants with very good to excellent credit, which is defined by the FICO model as 740 and above.

You can compare balance transfer credit card offers on Credible for free without affecting your credit score and determine if this debt repayment method is right for your financial situation.

BUY NOW, PAY LATER LOANS TO BE FORMALLY INCLUDED IN EQUIFAX CREDIT REPORTS

2. Debt consolidation loans

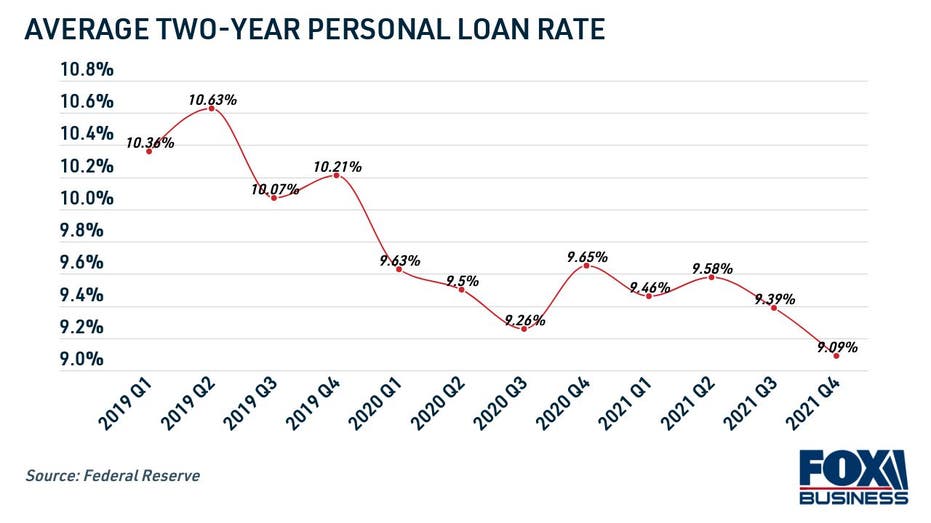

Another popular debt payoff strategy is to utilize a personal loan for debt consolidation. Unsecured personal loans allow borrowers to repay higher interest debt, including credit cards, at a low, fixed rate. Since personal loan interest rates are at all-time lows, according to the Fed, it may be possible to save more money than ever using this debt consolidation method.

By consolidating credit card debt into a personal loan, borrowers have the potential to save hundreds or even thousands of dollars over the course of their debt repayment. A recent Credible analysis found that well-qualified borrowers can save nearly $2,400 on average by paying off credit card debt with a personal loan.

A debt consolidation loan can also help you lower your monthly debt payments. The same analysis found that borrowers can save an average of $66 on their monthly payments by paying off credit card debt with a personal loan.

Personal loan interest rates are based on a borrower's credit profile, so applicants with high credit scores will qualify for the lowest rates. On the other hand, borrowers with bad credit may not qualify for a debt consolidation loan.

You can visit Credible to compare personal loan interest rates and terms across multiple lenders at once to help you find the lowest rate possible for your financial situation. Then, you can use a personal loan calculator to estimate your monthly payment and potential interest savings.

GEN Z CONSUMERS RESOLVE TO SAVE MONEY AND SPEND LESS IN 2022

3. Nonprofit credit counseling

The debt repayment strategies above may be good options for borrowers with good credit. However, consumers with fair or bad credit may not qualify for balance transfer credit cards or debt consolidation loans. It may be possible for subprime borrowers to pay off credit card debt through nonprofit credit counseling.

Credit counseling agencies provide free or low-cost services to consumers struggling with insurmountable debt. A credit counselor may help you create a budget or enroll you in a debt management plan (DMP), which may come with a monthly fee.

As an added bonus, credit counselors may be able to negotiate with creditors on your behalf to lower your interest rates and waive late fees. You can search for accredited nonprofit credit counseling agencies on the Department of Justice website.

If you're still not sure which debt repayment strategy is right for you, get in touch with a knowledgeable loan officer at Credible who can guide you through your options. Plus, you can browse current personal loan interest rates in the table below.

HOW DOES THE DEBT SNOWBALL METHOD WORK? STARTING WITH THE SMALLEST BALANCES

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.