How to lower your credit card payments by consolidating into a personal loan

Credit card consolidation loans may save you thousands in interest charges

Personal loans offer a way to repay credit card debt at a fixed interest rate and low monthly payment. (iStock)

Making the minimum payments on your credit cards can be an expensive way to get out of debt, and it's even more frustrating when even the minimum payments are unaffordable. Because credit card interest accrues daily, it can take years to pay off your balances even when you don't miss a payment.

Thankfully, there are faster (and cheaper) ways to pay off credit card debt — such as credit card consolidation loans. This is a type of personal loan that you repay in fixed monthly installments at a lower interest rate. Consolidating into a new loan may even help you pay less than the minimum credit card payment, all while getting out of debt faster and saving money over time.

Keep reading to learn how to lower your credit card payments using a personal loan. You can visit Credible to compare personal loan rates for free without impacting your credit score.

15 BEST DEBT CONSOLIDATION LOANS FOR FAIR CREDIT

Personal loans may help you lower your credit card payments

Credit card companies may allow you to borrow money up to a certain limit while making a low minimum payment, sometimes just $25 or a small percentage of the total balance. But the more debt you have, the higher your minimum payment will be — and the longer it will take to pay off your balances.

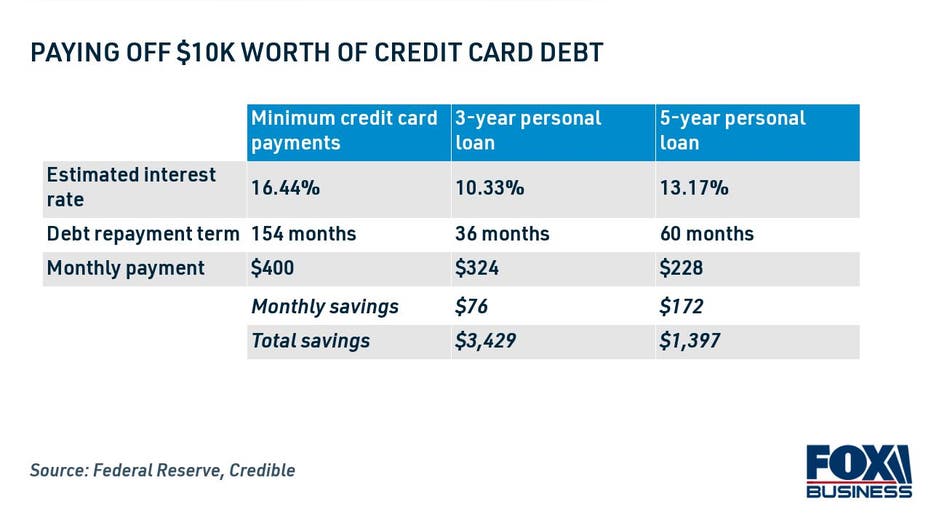

For example, if you have $10,000 worth of credit card debt, your monthly payment may be as high as $400, or 4% of the total balance. Since the average credit card rate is at 16.44%, according to the Federal Reserve, it will take more than 12 years to repay the debt with interest and fees.

It may be possible to reduce your monthly payment and pay off debt years faster by consolidating into a personal loan. That's because interest rates are much lower for personal loans than they are for credit cards. Plus, personal loan rates are fixed for the entirety of the term, which means interest doesn't accrue on a daily basis.

Paying of $10,000 in credit card debt with a 3-year personal loan can potentially reduce your monthly payment by $76 per month. By refinancing into a 5-year personal loan, you may save $172 per month compared to the minimum credit card payment.

Since you're paying off the debt years faster, you can save even more money in interest charges over the life of the loan. Interest rates are lower for shorter-term loans, which means you may be able to save nearly $3,500 over time by choosing a 3-year loan term compared to making the minimum credit card payment. But even if you choose the 5-year personal loan term with a lower monthly payment, you may still save about $1,400 while you repay your debt.

You can visit Credible to see personal loan rates tailored to you with a soft credit check, and use a personal loan calculator to estimate your new monthly payments.

PERSONAL LOAN ORIGINATION FEES: ARE THEY WORTH THE COST?

How to use a personal loan for credit card debt consolidation

It's relatively simple to pay off high-interest credit card balances with a personal loan, and it can be done completely online without leaving the comfort of your home. Here's what the process looks like in five steps:

- Determine how much you need to borrow

- Check your credit score

- Choose a loan term

- Compare personal loan rates

- Formally apply for the loan

Read more about each step in the sections below:

1. Determine how much you need to borrow

You can consolidate the balances of one or more credit cards into a personal loan. Add up your credit card balances to determine the personal loan amount you need to borrow.

Be careful not to over-borrow, or else you'll pay interest on money you didn't need to repay your credit card debt.

HOW TO GET A BALANCE TRANSFER CREDIT CARD

2. Check your credit score

Since personal loans are unsecured and don't require collateral, lenders determine your eligibility and interest rate based on your creditworthiness. This includes your credit score and debt-to-income ratio, which is your debt payments divided by your monthly income.

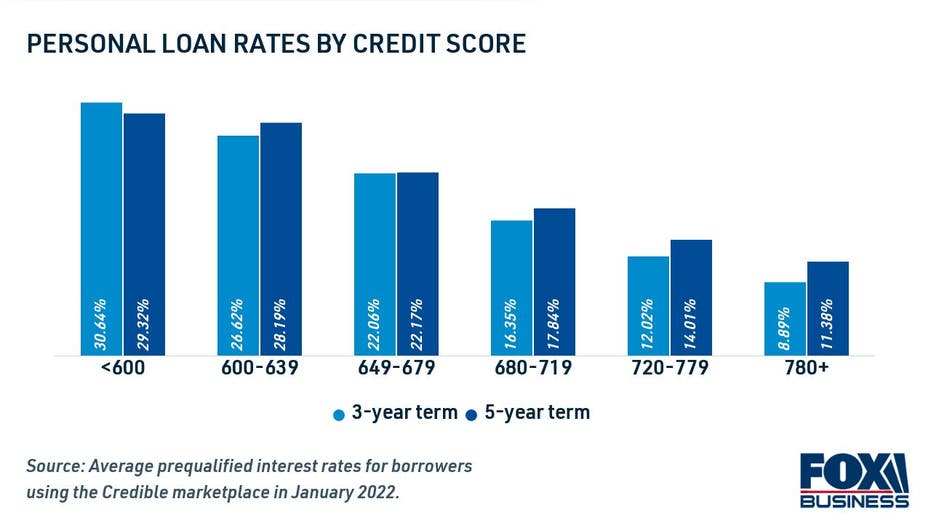

Applicants with very good or excellent credit, defined by the FICO scoring model as 740 or higher, will qualify for the lowest personal loan rates available. On the other hand, borrowers with bad credit will have a difficult time qualifying for a personal loan with good terms.

Knowing your credit score can help you determine if you're a good candidate for credit card consolidation. You can check your credit score and enroll in free credit monitoring on Credible.

HOW TO CHECK YOUR CREDIT SCORE FOR FREE WITHOUT PENALTY

3. Choose a loan term

Shorter loan repayment terms typically offer lower interest rates, but they'll come with higher monthly payments. But because you're paying off your debt faster, you'll save more in interest charges over the life of the loan.

Longer loan terms may help you reduce your monthly payments, but may come with higher interest rates. This can add to the overall cost of borrowing the loan, although it may be worthwhile if your goal is to lower your credit card payments.

For example, well-qualified borrowers who used Credible to get prequalified for a 3-year personal loan saw an average rate of 10.33% during the week of Feb. 7. Average rates of 5-year fixed-rate personal loans were 13.17% during this time.

HOW TO USE A HOME EQUITY LOAN FOR DEBT CONSOLIDATION

4. Compare personal loan rates

Most online lenders let you get prequalified to see your estimated personal loan rates and repayment terms. Prequalification requires a soft credit inquiry, and it won't hurt your credit score.

You can compare credit card consolidation loan rates across multiple lenders at once on Credible.

5 BENEFITS OF HAVING A GOOD CREDIT SCORE

5. Formally apply for the loan

Once you've chosen the right personal loan offer for your needs, you'll need to fill out a formal personal loan application through the lender. This requires a hard credit inquiry, which will temporarily lower your credit score.

If you're approved, the personal loan funds may be deposited directly into your checking account as soon as the next business day. You can then use the money to pay off your credit card balances to zero. Be careful not to accumulate new credit card debt while you're repaying your personal loan.

You can browse personal loan rates in the table below, and visit Credible to learn more about your debt consolidation options.

WHAT IS A HOME EQUITY LINE OF CREDIT AND HOW DOES IT WORK?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.