Own any of these investments? Don't let these tax rules surprise you

Many investments follow traditional capital gains tax rates

Taxes made easy for newlyweds and new parents

Sponsor Content: Tax advice for recently married couples and new parents filing in 2022

Part of being financially savvy is knowing exactly what kind of tax bill you may face for different income levels or investments. While some parts of the U.S. tax code may be fairly straightforward, there are some exceptions you should be aware of in case it applies to you.

WAITING ON A TAX REFUND FROM LAST YEAR? HERE'S SOME GOOD NEWS

How capital gains taxes work

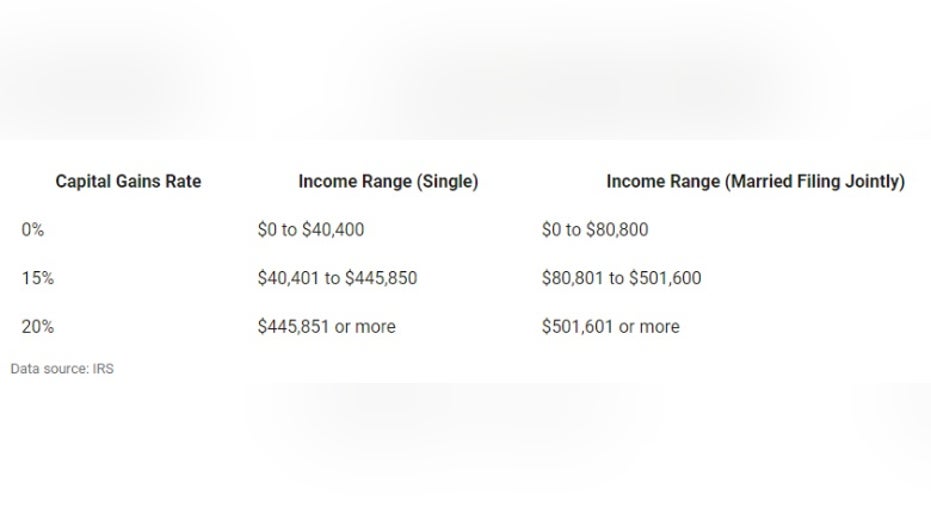

For starters, many investments follow traditional capital gains tax rates. Short-term capital gains -- those held under one year -- are taxed at regular income tax rates. Investments held longer than one year are given a favorable tax treatment and are much more straightforward. There are three primary capital gains tax brackets:

Courtesy of the Motley Fool, via data from the IRS.

For example, if you bought shares of a company for $1,000, held them for nine months, and then sold them for $1,500, you'd owe your income tax percentage on the $500 profit. If you bought those same shares and held them for two years before selling, you'd owe your capital gains rate. While the vast majority of investments fall into these straightforward capital gains brackets, there are three exceptions you should know about in case it applies to you.

1. How collectibles are taxed

Collectibles -- such as rare items, artwork, gold and silver coins, stamps, and antiques -- are considered alternative assets by the IRS. Let's say you bought a piece of art for $10,000 and later sold it for $50,000. Assume that you're in the highest ordinary income tax bracket. Under normal circumstances, you'd pay 20% on the $40,000 profit ($8,000). However, since art is considered a collectible, you'd pay a higher 28% rate, making your tax bill $11,200.

While normal exchange-traded funds (ETFs) are taxed at regular capital gains rates, ETFs that are backed by gold or silver fall into the collectibles category and also face the 28% rate, so make sure you don't underestimate your potential tax bill by using your typical capital gains rate to calculate what you owe.

BEHIND ON FILING YOUR TAX RETURN? MAKE THIS KEY MOVE

2. How qualified small business stock is taxed

If you sell shares of a qualified small business stock (QSBS), the greater of $10 million or 10 times your adjusted basis -- the cost you paid for them -- is free from capital gains taxes if you've held it for at least five years (unless the business is operating in financial services, farming, restaurants, or hotels).

For example, if you bought 100,000 shares of a company at its initial issuance for $15 each ($1.5 million total) and 5+ years later sold all the shares, up to $15 million would be exempt. Had you bought those same 100,000 shares for $5 ($500,000) and later sold them, $10 million would be exempt. Unfortunately, any excess earnings above the exemption will face a 28% capital gains tax.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

3. How property under Section 1250 is taxed

Section 1250 of the Internal Revenue Code (IRC) focuses on taxing the gains made from selling depreciated real estate property, which could be commercial buildings, rental properties, or warehouses. Imagine that you purchased a warehouse for $250,000, and some years later, it has depreciated by $50,000, making its tax basis $200,000. If you were to sell the property for $225,000, your taxable gain would be $25,000.

Under normal circumstances, that $25,000 in profit would be subjected to your typical capital gains rate, but since it falls under the IRC's Section 1250, it'll be taxed at a 25% rate.

CLICK HERE TO READ MORE ON FOX BUSINESS

Knowing can help your financial planning

One of the keys to successful financial planning is knowing your expenses, and for people who are selling assets of any kind, part of those expenses will likely include capital gains taxes. Using the wrong capital gains rate and miscalculating what you may owe can result in a bill that's thousands more than you anticipated and throw off your planning. To stop this from happening, one of the best things you can do is to know in which category your assets fall and whether they're an exception to the typical rates.

The Motley Fool has a disclosure policy.