Half of Americans consistently struggle to pay their bills on time, survey says

1 in 5 consumers said that inflation has made it harder to pay their debts

Just half of Americans were able to consistently pay their bills on time in the past year, a new survey shows. Many consumers said inflation is to blame. (iStock)

Inflation is surging at the highest rate in 40 years, and it's impacting the way consumers save and spend money.

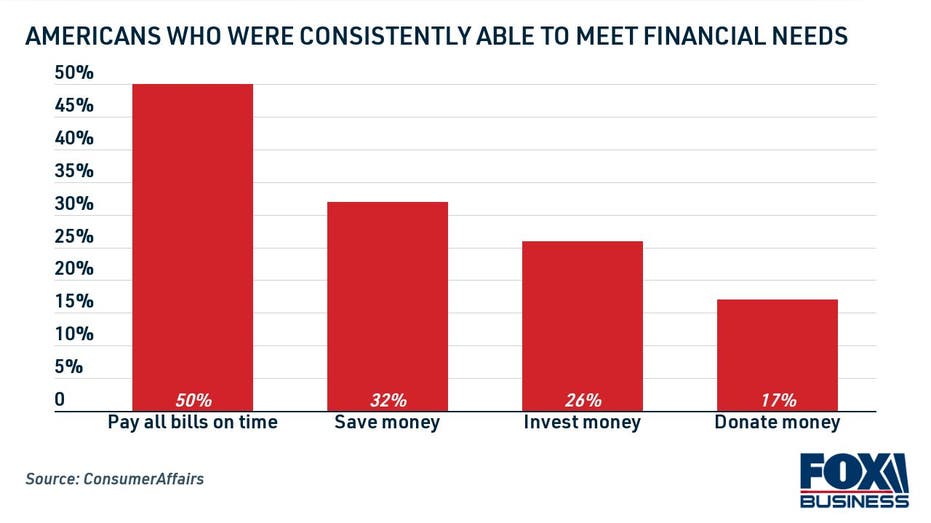

In the past year, 50% of Americans were unable to consistently pay their bills on time, according to a new survey from ConsumerAffairs. Less than a third (32%) of respondents were able to save money consistently, while just over a quarter (26%) were able to invest. About a fifth said their ability to afford bills worsened due to inflation.

AVERAGE HOUSEHOLD PAYS $1K IN CREDIT CARD INTEREST AND FEES ANNUALLY

This comes at a time when credit card balances are growing at a record pace, according to the Federal Reserve Bank of New York, which signals that Americans are becoming more reliant on credit card spending to make ends meet.

Keep reading to learn more about how inflation is impacting household finances, as well as what you can do to offset rising consumer prices and credit card debt. One way to cut spending is to consolidate debt into a personal loan while interest rates are at historic lows. You can compare debt consolidation loans on Credible for free without impacting your credit score.

PERSONAL LOAN ORIGINATION FEES: ARE THEY WORTH THE COST?

Inflation strains household finances, including essential spending

The Consumer Price Index (CPI) rose 7.5% annually in January, which means that Americans are faced with higher costs for necessities like food, housing and utilities.

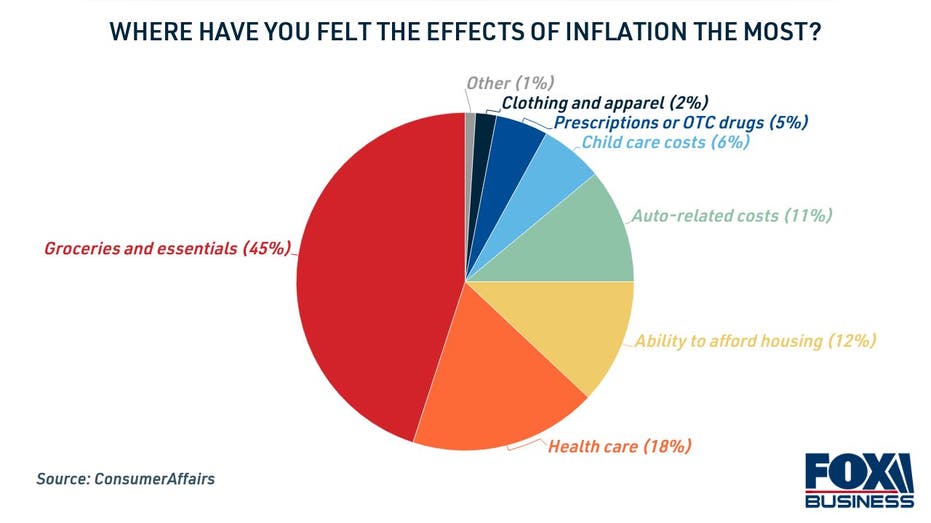

Consumers said that inflation has had the largest impact on groceries and essentials (45%), followed by health care (18%), housing costs (12%) and auto loans (11%), according to the survey.

HOW TO GET A BALANCE TRANSFER CREDIT CARD

Three-quarters of consumers have had to change their spending habits in the past year to make ends meet, such as buying fewer groceries (31%) selling personal items (26%) and getting a second job (25%). Additionally, 1 in 9 respondents had to pull their children out of child care.

As inflation soars, household debt grew by $1 trillion in 2021 — the most since before the Great Recession, according to the NY Fed. Notably, Americans added $86 billion to their revolving credit card balances during this time.

If you're looking for ways to pay down high-interest credit card debt amid rising consumer prices, you may consider opening a debt consolidation loan. This is a type of personal loan that's used to repay debt in fixed monthly installments at a low interest rate. You can compare personal loan rates on Credible, and use a personal loan calculator to estimate your monthly payments.

15 OF THE BEST PERSONAL LOANS FOR BAD CREDIT

How to consolidate debt into a personal loan

Using a personal loan for debt consolidation is relatively simple, and the application process can be done completely online. Consolidating debt at a lower interest rate may help you reduce your monthly payments, pay off debt faster and save thousands of dollars over time. Here's how it works:

- Calculate the loan amount you need to borrow. Add up all your high-interest debt payment obligations, such as credit cards and payday loans. This will help you determine the minimum loan amount you need to consolidate your debts.

- Check your credit score. Personal loan lenders determine your interest rate and eligibility based on your credit history. This includes your credit score and debt-to-income ratio, which is your monthly debt payments divided by your income.

- Compare personal loan rates. Most lenders let you get prequalified to see your estimated interest rate with a soft credit inquiry, which won't impact your credit score. That way, you can shop around for the lowest possible rate for your financial situation.

- Choose a loan offer. Shorter loan terms may offer lower interest rates, but they'll come with higher monthly payments. Longer loan terms can help you reduce your monthly debt payments, but they may cost more money over time due to higher interest rates.

- Formally apply for the loan. Once you've chosen the personal loan agreement that works for you, you'll formally apply for the loan. This will require a hard credit check at the time of application, which will have a temporary but minimal impact on your credit score.

HOW YOUR CREDIT SCORE IS IMPACTED BY SOFT AND HARD CREDIT INQUIRIES

Upon loan approval, the funding may be deposited into your bank account as soon as the next business day. You can then use the money to pay off your credit balances to zero. Just be careful not to accumulate more credit card debt while you repay the personal loan.

You can browse current personal loan interest rates in the table below, and visit Credible to see debt consolidation offers tailored to you without hurting your credit score.

DOES HAVING CREDIT CARDS WITH A ZERO BALANCE HURT YOUR CREDIT UTILIZATION RATIO?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.