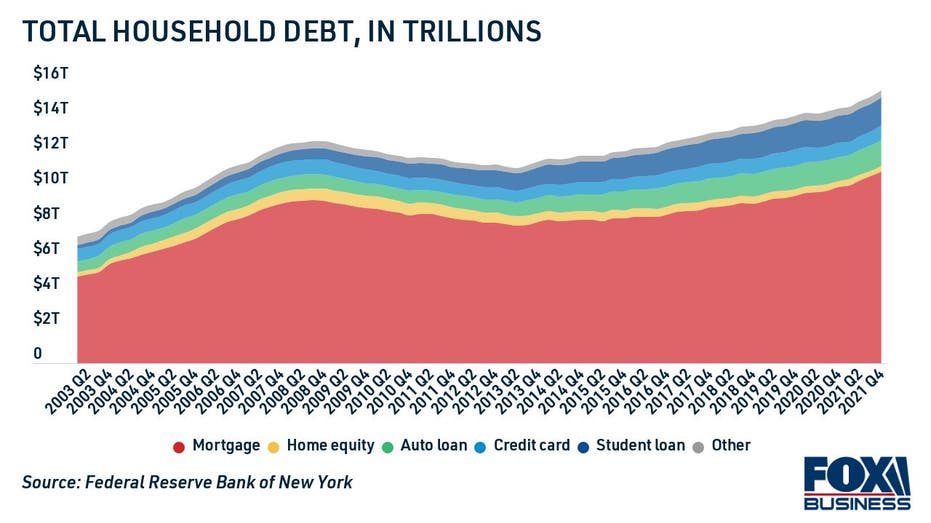

NY Fed: Household debt grew by $1 trillion in 2021, most since before the Great Recession

Here's how to pay down your mortgage, credit card and student loan balances

Growing household debt is driven by higher prices on consumer goods, including homes and cars, according to the New York Fed. (iStock)

Household debt grew by more than $1 trillion last year, driven by rising prices on cars and housing, according to a new report from the Federal Reserve Bank of New York. This is the largest annual debt increase since before the Great Recession of 2008.

"The total increase in nominal debt during 2021 was the largest we have seen since 2007," said New York Fed Senior Vice President Wilbert Van Der Klaauw in a statement. "The aggregate balances of newly opened mortgage and auto loans sharply increased in 2021, corresponding to increases in home and car prices."

Notably, credit card debt soared by $52 billion in the fourth quarter of 2021, which is the largest quarterly increase in the 22 years since the NY Fed began collecting this data. Outstanding mortgage debt grew by $258 billion during this time, and auto loan balances increased by $15 billion.

Keep reading to learn more about the growing household debt balances, including ways to pay off debt and save money. You can visit Credible to compare a variety of debt consolidation products, such as credit card consolidation loans, student loan refinancing and mortgage refinancing.

1.5M HOMEOWNERS IN MORTGAGE DELINQUENCY, REPORT FINDS

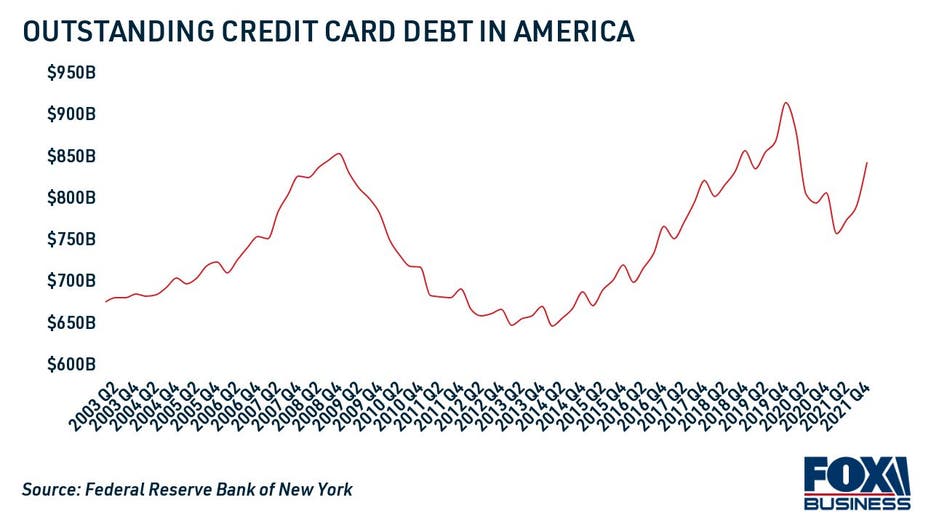

Credit card debt surges to pre-pandemic levels

Outstanding credit card debt grew to $856 billion last year, which is the highest it's been since the coronavirus pandemic began in early 2020. In the fourth quarter of 2021, credit card balances spiked 6.5% — a record quarterly increase since the NY Fed began collecting this data.

REVOLVING CONSUMER CREDIT BALANCES REACH PRE-PANDEMIC LEVELS

This suggests that Americans are becoming increasingly reliant on high-interest credit card debt as inflation drives up prices on a number of consumer goods, from gas to groceries. And with the average credit card interest rate at 16.44%, according to the Federal Reserve, consumers with revolving credit card balances could be driven even further into debt.

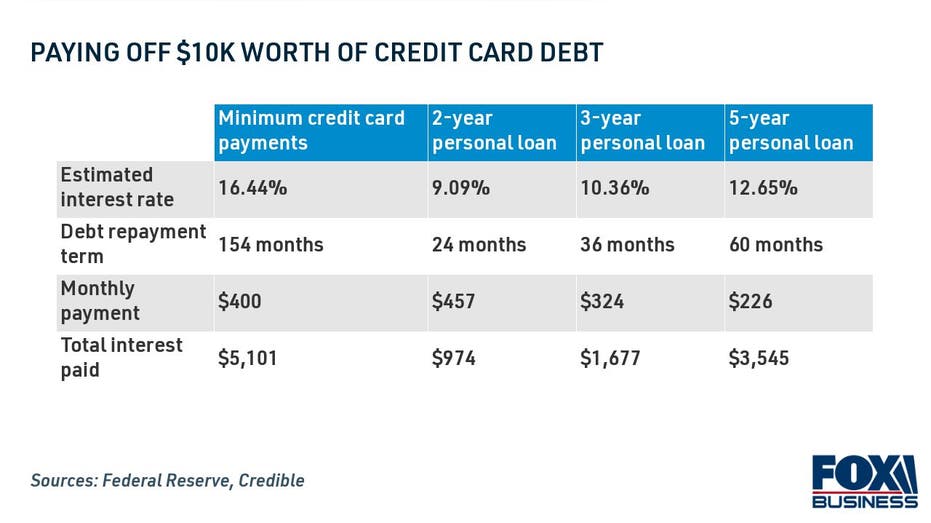

One way to pay down credit card debt is with a personal loan for debt consolidation. This is a type of unsecured, lump-sum loan that's repaid in fixed monthly installments at a lower interest rate. The average interest rate on a two-year personal loan is currently at a historic low of 9.09%, the Fed reports.

Paying off credit card debt with a personal loan may save well-qualified borrowers thousands of dollars worth of interest charges over time, a recent analysis suggests. You can use a personal loan calculator to estimate your monthly payments and potential savings.

If you decide to use a personal loan for credit card consolidation, visit Credible to compare interest rates for free without impacting your credit score. That way, you can shop around for the best possible offer for your financial situation.

THREE-QUARTERS OF AMERICANS WORRY SOCIAL SECURITY WILL RUN OUT BEFORE THEY RETIRE

Student loan debt steadily grows to $1.58T

Student loan balances increased by $21 billion in 2021, according to the NY Fed. That's a relatively small annual increase, because the interest and payments on federal student loans have been paused since March 2020.

Although the Biden administration has extended the federal student loan forbearance period several times, monthly payments and interest charges are set to resume this May. At this time, student loan balances may resume pre-pandemic growth, leaving millions of borrowers responsible for repaying their student debt for the first time in more than two years.

If you're not prepared to resume federal student loan payments in a few short months, here are a few strategies to consider:

- Enroll in an income-driven repayment plan (IDR) to limit your student loan payments to 10-20% of your disposable income. Federal student loan borrowers can learn more about IDR plans on the Federal Student Aid website.

- Apply for up to 36 months of additional federal forbearance through an economic hardship or unemployment deferment request. Keep in mind that interest may accrue while your student loans are in deferment, adding to your total loan balance over time.

- Refinance to a private student loan with a lower interest rate. Student loan refinancing may help some borrowers reduce their monthly payments, pay off their debt faster and save money over time. You can use a student loan refinance calculator to estimate your potential savings.

It's important to note that refinancing your federal student debt into a private loan will make you ineligible for certain protections, such as IDR plans, COVID-19 administrative forbearance and federal student loan forgiveness programs. You can visit Credible to learn more about student loan refinancing and determine if this debt repayment strategy is right for you.

WHAT CREDIT SCORE DO YOU NEED FOR A MORTGAGE?

Rising home prices spur growing mortgage balances

The surge in household debt was driven in part by record home price growth, the NY Fed found. Rising home values resulted in homebuyers taking out larger home loans — mortgage originations exceeded $4.5 trillion last year, which is a historic high in terms of annual growth.

Many homeowners were able to take advantage of rising home equity and historically low interest rates during the pandemic to refinance their mortgage loans. Although mortgage rates have begun to rise at the beginning of 2022, some homeowners may still benefit from refinancing thanks to home price appreciation.

Mortgage refinancing may help you lower your monthly mortgage payment, repay your home loan faster and save money on interest over the life of the loan. You can compare current mortgage rates in the table below, and visit Credible to see mortgage refinancing offers tailored to you for free without impacting your credit score.

MORTGAGE FORECLOSURES RISE AS MORATORIUM ENDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.