Fed rate hikes may drive up your monthly credit card payments: Here's how to cut costs

Consolidating into a fixed-rate loan can help you offset rate hikes

Variable credit card APRs are likely to rise in the coming months as the Federal Reserve is expected to increase interest rates. (iStock)

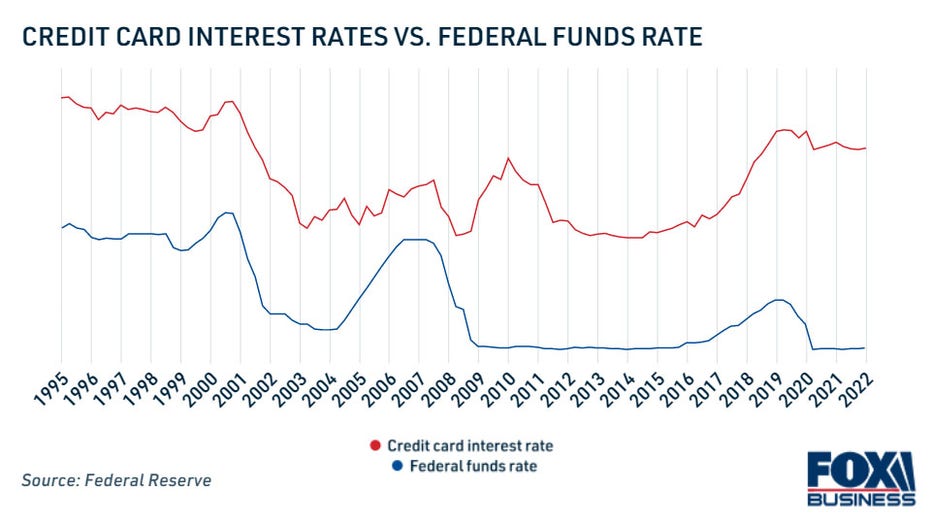

The Federal Reserve lowered its benchmark rate in spring 2020 to stimulate economic activity during the COVID-19 pandemic. As a result, interest rates stayed low on a number of financial products, from mortgages to credit cards.

But the Fed has planned several rate hikes in 2022 to combat high inflation, which is surging well above the central bank's 2% annual target. The first increase was implemented this March, causing 30-year mortgage rates to soar past 5% for the first time in more than a decade.

While the Fed's economic policy had a swift and significant impact on mortgage rates, the rate hikes haven't been as consequential for credit card users — yet. Fed Chairman Jerome Powell previously indicated that consumers should expect faster and larger rate increases throughout the year, which means that credit card rates will only continue to rise.

The latest data from the Fed shows that the average credit card interest rate has already begun to tick up along with the federal funds rate. In the first quarter of 2022, the average credit card rate rose to 14.56%, up slightly from 14.51% in the fourth quarter of 2021.

If you're looking for ways to cut down on interest charges as the Fed raises rates this year, you might consider consolidating variable-rate credit card debt into a fixed-rate personal loan. This will lock in your interest rate for the entirety of the repayment term. You can learn more about debt consolidation on Credible.

PROS AND CONS OF BALANCE TRANSFER CREDIT CARDS

When your credit card company can raise your rate

Your credit card issuer can increase your interest rate on new purchases if you have a variable rate that's tied to a certain index like the U.S. prime rate, according to the Consumer Financial Protection Bureau (CFPB). Since the prime rate is impacted by the Fed's benchmark rate, your credit card interest rate will likely rise at about the same pace.

"That means you’ll pay more on your card balances," CFPB Director Rohit Chopra said in a recent blog post.

It's important to note that your bank must give you a notice 45 days in advance before increasing your interest rate. Additionally, your credit card rate may rise to a penalty APR if your minimum payment is more than 60 days late past your due date.

Since credit card interest is compounded daily, the added cost of borrowing can add up quickly when your rate increases. Plus, your monthly minimum credit card payments will rise in turn.

If you're struggling to keep up with your minimum monthly payment, you might consider credit card consolidation with a personal loan. You can visit Credible to compare personal loan rates for free without impacting your credit score.

AVERAGE HOUSEHOLD PAYS $1K IN CREDIT CARD INTEREST AND FEES ANNUALLY

How to pay off credit card debt with a personal loan

Consolidating credit card debt into a personal loan at a lower interest rate may help you lower your monthly payment and save money over time. Plus, debt consolidation is a simple process that can be done completely online. Here are five steps for paying off credit card balances with a personal loan:

1. Check your credit score.

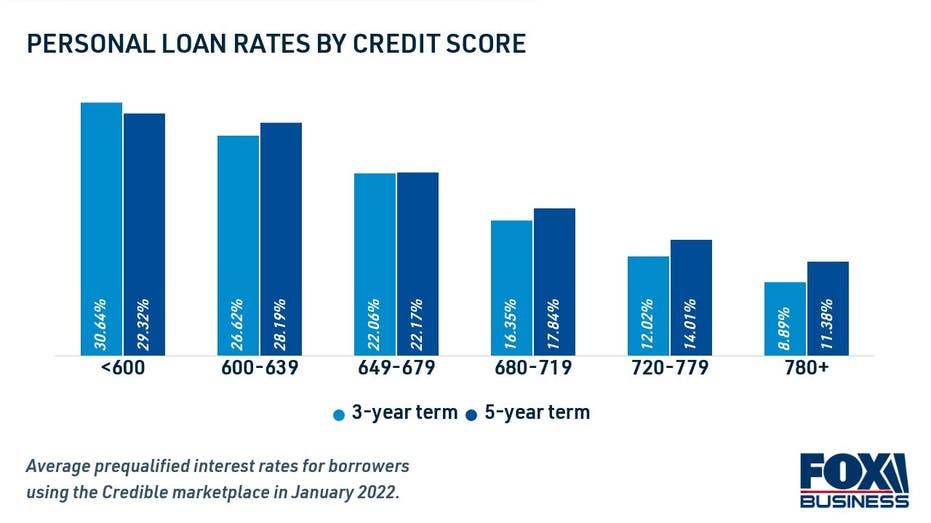

Personal loan lenders determine an applicant's interest rate based in part on creditworthiness and debt-to-income ratio (DTI). Borrowers with an excellent credit score and a low credit utilization will see the best possible offers, while those with fair or bad credit may see higher rates — if they qualify at all.

To get a better idea of your credit history, you can request a free copy of your credit report through all three major credit bureaus (Equifax, Experian and TransUnion) on www.AnnualCreditReport.com.

HOW DO BALANCE TRANSFERS AFFECT YOUR CREDIT SCORE?

2. Estimate your loan amount.

Add up your credit card balances to determine how much you need to borrow. You can consolidate the debt from one or multiple credit cards into a single monthly payment with a personal loan. Then, you can use a personal loan calculator to see your monthly payment.

3. Shop around to compare offers.

Most lenders let you get prequalified to see your estimated interest rate with a soft credit inquiry, which won't impact your credit score. You can compare personal loan rates from multiple lenders at once on Credible's online loan marketplace.

6 BEST PERSONAL LOANS FOR GOOD CREDIT

4. Formally apply for the loan.

Once you've chosen the best loan offer for your financial situation, you'll need to submit a formal application. This requires a hard credit check, which will have a temporary negative impact on your credit history. You'll also need to submit proof of identification and income, such as pay stubs and a driver's license.

5. Wipe your credit card balances to zero.

Upon approval, the lender will deposit your personal loan funds directly into your bank account, sometimes as soon as the next business day. You can use your loan to pay off the entire balance of your credit card debt at a fixed rate, so your monthly payment won't rise with inflation.

You can browse current personal loan rates in the table below, and visit Credible to learn more about credit card consolidation.

HOW TO MAXIMIZE YOUR CREDIT CARD REWARDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.