Biden criticizes GOP lawmakers for 'dangerous' debt ceiling inaction, warns of interest rate hikes

Failure to raise the debt limit may also delay Social Security payments, federal salaries and veterans' benefits

Lawmakers in Washington are working to pass a debt limit suspension before government funding runs out, which could happen as soon as Oct. 18, according to Treasury estimates. (iStock)

As the federal government draws closer to defaulting on its financial obligations for the first time in history, President Joe Biden condemned Republicans for refusing to raise the debt ceiling and "playing Russian roulette with the U.S. economy" during an address from the White House on Monday.

"Not only are Republicans refusing to do their job, they’re threatening to use the power — their power to prevent us from doing our job: saving the economy from a catastrophic event," Biden said. "I think, quite frankly, it’s hypocritical, dangerous and disgraceful."

Legislation surrounding the federal debt limit has earned bipartisan support in recent years — it was raised three separate times during the Trump administration. But this time, GOP lawmakers said they won't vote to raise the debt ceiling. Senate Minority Leader Mitch McConnell (R-Ky.) wrote to the president that "since your party wishes to govern alone, it must handle the debt limit alone as well."

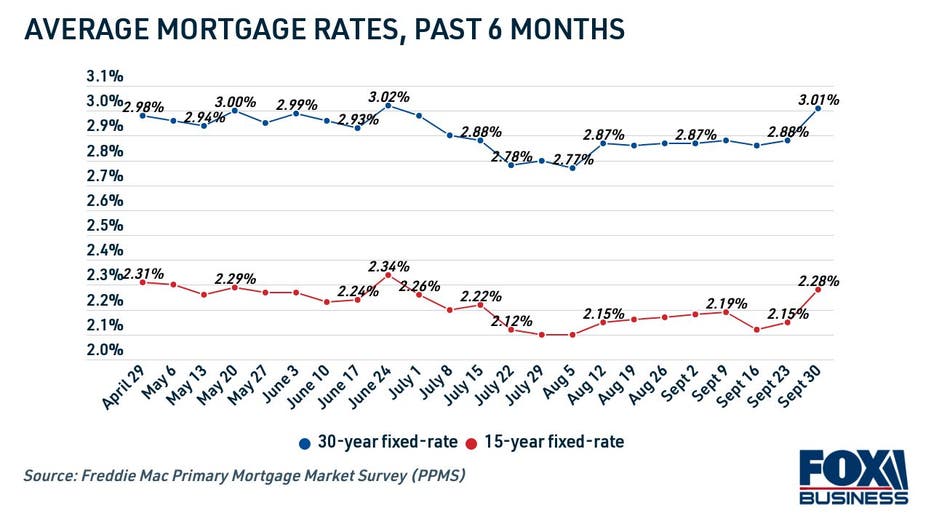

Failure to raise or suspend the debt limit could jeopardize federal payments, Biden warned, including Social Security checks, salaries for military personnel and veterans' benefits. Going into default could also permanently damage the credit of the United States, causing interest rates to rise on mortgages, auto loans and credit cards, he added.

In the days ahead, even before the default date, people may see the value of their retirement accounts shrink. They may see interest rates go up, which will ultimately raise their mortgage payments and car payments.

SENATE BLOCKS BILL TO AVERT GOVERNMENT SHUTDOWN THAT MAY DELAY SOCIAL SECURITY, MEDICARE BENEFITS

Congress has until Oct. 18 to come up with a solution to address the debt ceiling before the government defaults on its obligations, according to Treasury Secretary Janet Yellen. The Treasury Department has been taking "extraordinary measures" to keep the government funded since the previous debt ceiling suspension expired at the end of July, Yellen has said.

If you rely on federal payments like Social Security or veterans' benefits, keep reading to learn how you can manage your finances in the event of a government default. You can compare a range of financial products on Credible's online marketplace without impacting your credit score.

BIDEN FACING RENEWED PUSH FROM DEMOCRATS TO CANCEL $50K IN FEDERAL STUDENT LOAN DEBT

How to get extra cash if you rely on federal benefits

Federal payments, including government salaries and Social Security payments, are hanging in the balance as lawmakers struggle to come to an agreement about the debt limit. If you rely on federal payments to make ends meet, you may want to consider your borrowing options to avoid potentially defaulting on your personal financial obligations.

FAILURE TO LIFT DEBT CEILING MAY CAUSE MORTGAGE RATES TO RISE, REPORT FINDS

Tap into your home equity

Mortgage refinancing can grant you better terms like a lower mortgage rate, but it may also allow you to tap into your home's equity in the form of cash.

Cash-out mortgage refinancing involves taking out a mortgage that's larger than what you currently owe on your home loan, so you can pocket the difference in a lump sum. The amount you can borrow depends on your home's appraisal value — and thanks to record-high home values, that's higher than ever.

Keep in mind that mortgage refinancing also comes with closing costs, which are typically about 2% to 6% of the total loan amount. You can use a mortgage payment calculator to see the total cost of refinancing to a larger loan.

Mortgage rates are currently near historic lows, according to Freddie Mac, but that could change if the government defaults on its debt later this month. That means now is a good time to lock in a favorable mortgage refinancing offer.

You can compare rates without impacting your credit score on Credible so you can decide if cash-out refinancing is right for you.

MILLIONS OF AMERICANS FEAR MISSING DEBT PAYMENTS, NY FED REPORTS

Lower your debt payments by refinancing

You can refinance just about any type of loan, including home loans and student loans. And since interest rates are historically low across a range of financial products, refinancing may help you lower your monthly payments in addition to saving money on interest over time.

Student loan borrowers who refinanced to a longer-term loan were able to cut their monthly payments by more than $250 on average, according to a Credible analysis. With mortgage refinancing, you may be able to lower your mortgage payments, as well.

You can compare interest rates on a variety of financial products — including student loan refinancing and mortgage refinancing — on Credible's online marketplace.

BIDEN ADMIN REVERSES DONALD TRUMP-ERA STUDENT LOAN POLICY LIMITING STATE OVERSIGHT

Borrow an unsecured personal loan

Personal loans are lump-sum loans that don't require you to borrow against an asset like your home. They're repaid in fixed monthly payments, which can make them a more predictable alternative to taking out credit card debt.

Additionally, personal loan interest rates are typically lower than credit card interest rates. The average rate on a two-year personal loan was 9.58% in the second quarter of 2021, according to the Federal Reserve, compared with 16.30% for credit card accounts assessed interest.

You can compare personal loan interest rates for free on Credible. You can also use Credible's personal loan payment calculator to determine if this borrowing option fits into your monthly budget.

SENATE MAJORITY LEADER CHUCK SCHUMER RENEWS CALLS TO CANCEL $50K IN STUDENT LOAN DEBT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.