529 college savings plans: What to know and what has changed

The plans can help families limit borrowing for education

Get all the latest news on coronavirus and more delivered daily to your inbox. Sign up here.

Friday is national 529 College Savings Plan Day, which has been designated to celebrate and publicize the tax-advantaged method to save for education costs.

Users can prepay or contribute to a 529 account, which lets after-tax money grow tax-free. Distributions are not subject to taxes at the federal level if they are used for approved expenses, which includes items like tuition, books, room and board and technology. Recent legislation has expanded what qualifies as an allowable expense, which gave beneficiaries greater flexibility to cover their education costs.

Here are some things to know about the plans:

- There are no income restrictions on individual contributors, but allocations worth more than $15,000 during the year could trigger the gift tax. There are maximum aggregate limits for some plans that vary by state. In general, the plan's balance is not to exceed the expected costs of the beneficiary's qualified expenses.

- Contributions are not deductible, but some states may offer tax incentives.

- Accounts are offered through states and also through brokers, while qualified education institutions can only offer a prepaid tuition type 529 plan.

UNIVERSITY OF CALIFORNIA WILL STOP USING SAT, ACT

- The person who purchases the 529 plan is in control of the funds until their withdrawal.

- As of 2018, people have been allowed to withdraw up to $10,000 in annual expenses for other costs associated with an elementary, private or religious school. As of 2020, individuals have been able to allocate up to $10,000 toward repaying student loan debt, while another $10,000 is available to be put toward debt held by the beneficiary’s siblings

- The SECURE Act, passed in December, allowed funds to be used to pay for apprenticeship programs registered with the Labor Department.

- The Tax Cuts and Jobs Act also allowed for funds to be rolled over, in some cases, into an ABLE account, which is a tax-favored account to help families save and pay for disability-related expenses

- Funds can also be rolled over to the account of another family member without penalty.

NOTRE DAME BRINGING STUDENTS BACK TO CAMPUS 2 WEEKS EARLY

- Using the funds for anything other than qualified education-related expenses can trigger penalties, meaning earnings on contributions will be taxed as ordinary income and may also be subject to a 10 percent federal fee.

- The plans have grown in popularity throughout recent years, and they are the most popular way to save for college, according to Sallie Mae. About 30 percent of people said they have a plan.

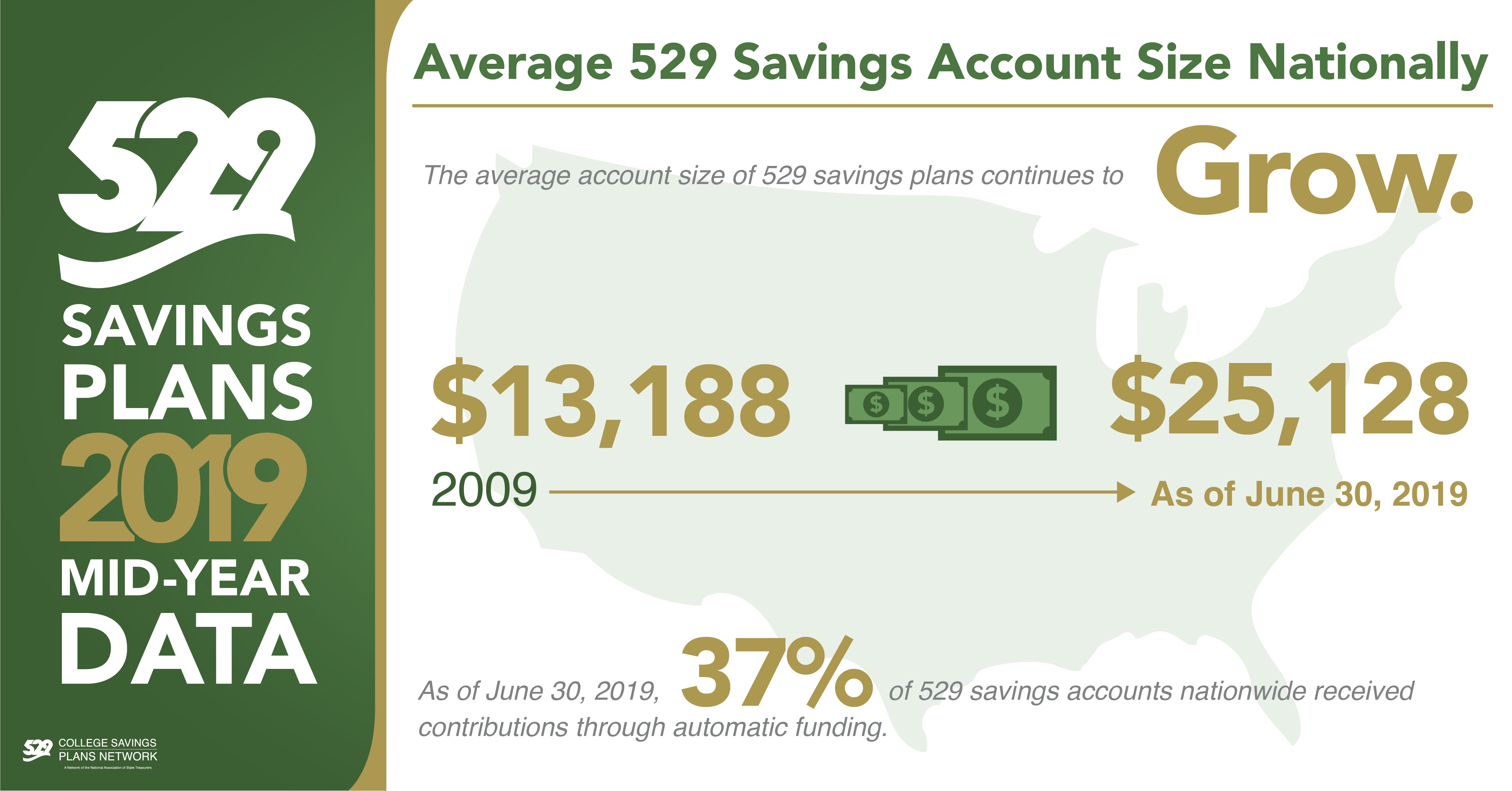

- The average 529 balance, as of 2019, was $25,128.

{kind=link}

A number of states on Friday are using inventive ways to get residents to open an account as the country celebrates their potential advantages. In Minnesota, for example, every account opened between May 26 and May 31 can receive a $50 match.

CLICK HERE TO READ MORE ON FOX BUSINESS

At a time when mounting student loan debt is burdening many Americans, the plans can be a way to limit how much families need to borrow for higher education. Outstanding student loan debt hit more than $1.5 trillion this year, according to data from the Federal Reserve Bank of New York. Education debt is second only to mortgage debt as a share of Americans’ total debt burdens.