Money is the top reason why students are dropping out of college, study finds

Here’s how private student loans can help students pay for school

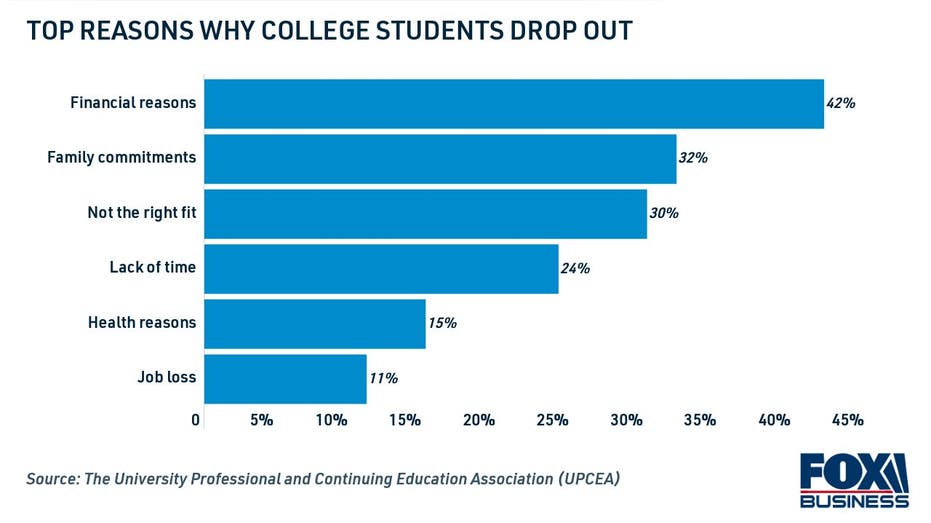

A recent study found that 42% of students who recently dropped out cited financial reasons as their primary cause for leaving. (iStock)

Having a college degree can offer many opportunities, but it can also come with a burdensome price tag. College costs have skyrocketed over the past few decades, outpacing inflation and making it difficult for Americans to afford higher education.

Money is the top reason why college students leave school, according to a recent study by the University Professional and Continuing Education Association (UPCEA). About two in five (42%) college dropouts cited financial reasons for leaving school, outweighing the percentage of students who left for other reasons like family commitments (32%) and health reasons (15%).

MILLIONS OF AMERICANS HAVE COLLEGE DEBT BUT NO DEGREE

Financial issues are an even larger problem for low-income students, according to Dr. Amy Smith, chief learning officer at online education company StraighterLine. The study showed that about two-thirds (65%) of those who stopped attending college had a household income of $50,000 or less — that's compared to less than 2% with an income above $100,000.

"Another key takeaway is the majority of disengaged learners are working adults that make $50,000 or less, so they are working on pretty tight budgets," Smith said. "This is a significant factor that colleges and universities need to think about when re-engaging students."

If you're considering dropping out due to financial reasons, keep reading to learn more about how you can pay for college and finish your degree. Visit Credible to compare private student loan rates across multiple lenders, so you can find the best possible offer for your financial situation.

COLLEGE GRADUATES CAN SAVE MORE MONEY AS STUDENT LOAN REFI RATES SET RECORD LOW

Bridge financing can help students who can't afford college

The federal government issues loans, scholarships and grants through the Free Application for Federal Student Aid (FAFSA). But federal student loans may not cover the entire cost of going to college due to annual borrowing limits, potentially leaving students on the hook for expenses such as room and board.

Here are the current federal Direct loan borrowing limits:

- Dependent undergraduate students: $5,500 for the first year of enrollment, $6,500 for the second year and $7,500 for the third year and beyond. The total borrowing limit for the entire undergraduate tenure is $31,000.

- Independent undergraduate students: $9,500 for the first year of enrollment, $10,500 for the second year and $12,500 for the third year and beyond. The total borrowing limit for the entire undergraduate tenure is $57,500.

- Graduate and professional students: $20,500 per year. The total borrowing limit (including undergraduate loans) is $138,500.

Students who have exhausted their federal financial aid awards may have considered dropping out, but it's not the only option. If you can't afford college tuition, you could consider bridging the financing gap with federal PLUS loans or private student loans.

If you're considering borrowing a private student loan to help pay for college, visit Credible to compare interest rates for free without impacting your credit score. Seeing your offers can help you decide if this financing option is right for you.

BIDEN MAY CUT FREE COMMUNITY COLLEGE FROM ECONOMIC PACKAGE

Private student loans vs. Direct PLUS loans

Federal PLUS loans are held by the federal government, whereas private student loans are issued by private financial institutions like banks and online lenders.

The office of Federal Student Aid (FSA) offers two types of loans for students who need more money to continue their education: Parent PLUS loans and graduate PLUS loans. Parent PLUS loans are awarded to parents of undergraduate students, while graduate PLUS loans are available to students who are enrolled in graduate school or another professional program.

Unlike Parent PLUS loans, private student loans can be borrowed by undergraduate students directly. This can make it possible for students to bridge the college financing gap without relying on their parents to borrow additional loans. Here are a few other notable differences between federal PLUS loans and private student loans:

- Private student loan eligibility is based on a borrower's creditworthiness, such as credit score and debt-to-income ratio. Students can consider enlisting the help of a cosigner to lock in better terms, like a lower interest rate.

- The current federal PLUS loan interest rate is 6.28% for loans originated before July 1, 2022. The average private student loan rate is 5.89% for a 10-year fixed-rate loan and 3.26% for a 5-year variable-rate loan, according to Credible.

- Private student loans aren't eligible for select government benefits like income-driven repayment plans (IDR), administrative forbearance periods or federal student loan forgiveness programs.

If you're still unsure whether you should borrow a private student loan, visit Credible to see your estimated offers. Then, use a student loan calculator to determine your monthly payments.

WHAT IS THE FREE APPLICATION FOR FEDERAL STUDENT AID?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.