College costs have risen at nearly 5x the rate of inflation, report finds

A degree from a public four-year institution would cost about $10,000 if college costs were consistent with inflation trends

The average cost of tuition, fees and other expenses at higher education institutions are rising at a much faster rate than inflation, according to a recent study. (iStock)

College expenses have escalated in recent years, but the rising costs are even more notable when accounting for inflation.

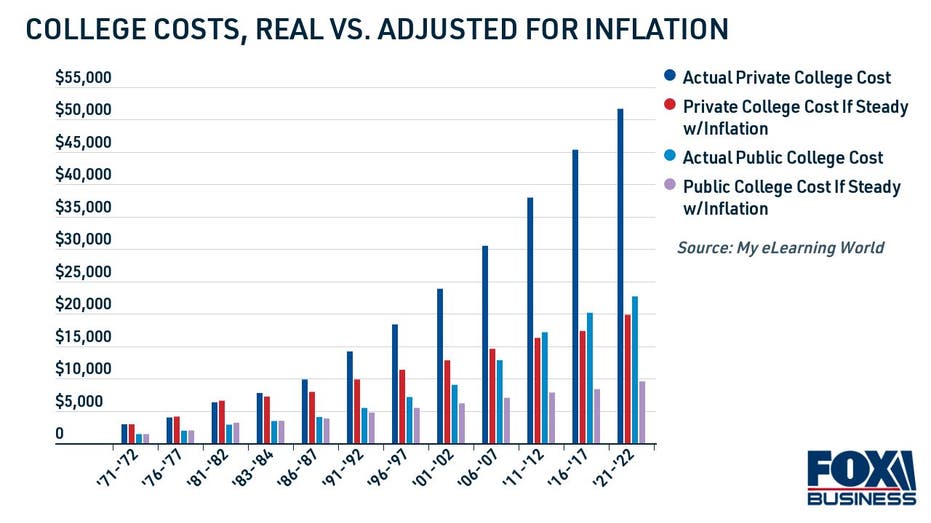

The price tag of a college education has risen at about 4.6 times the rate of inflation over the past 50 years, according to a recent report from My eLearning World.

BIDEN MAY CUT FREE PUBLIC SCHOOL COMMUNITY COLLEGE FROM ECONOMIC PACKAGE

The report analyzed the average annual price for attending college including tuition, fees, room and board and books using statistics from the nonprofit College Board.

Today, public college costs between $22,690 for in-state students to $39,510 for out-of-state students. In 1971, the average cost was $1,410 per year. For private schools, the costs have risen at an even higher rate.

The report estimates that if college costs rose consistently with inflation over the past five decades, students would be paying roughly $10,000 per year to attend a public university and $20,000 to attend a private university.

Despite the rising cost of higher education, research shows that it often pays off to have a college degree. Keep reading to learn more about your options for financing a college education, including private student loans. You can compare interest rates on private loans for free on Credible without impacting your credit score.

4 PRIVATE STUDENT LOAN TIPS FOR UNDERGRADUATE STUDENTS

How college students can cope with rising tuition costs

College tuition and fees can be a big expense for young high school graduates. When you add in other expenses like room and board, meal plans and textbooks, it can seem overwhelming.

Thankfully, there are plenty of options for rising college students who are looking to borrow money to cover expenses. If you're deciding how to pay for college, follow these steps:

- Do your research. Look up the average salary for your field of study, as well as the average cost of college at any university you're interested in applying to. Then, determine if your earnings will be enough to pay off future college debt.

- See if you qualify for federal financial aid. Fill out the Free Application for Financial Student Aid (FAFSA) to determine if you're eligible for federal student loans, grants and work-study programs.

- Apply for scholarships. Look for ways to finance your college education without overborrowing. The Sallie Mae website, for example, has a free guide on how to apply for college scholarships.

- Look into part-time jobs. Universities typically offer on-campus positions at cafeterias, bookstores and even in student housing. This can help cover unexpected expenses, as well as textbooks and groceries.

- Bridge the gap with private student loans. Federal Direct student loans have annual borrowing limits which may not cover the full cost of college. In this case, consider using private student loans to make up the difference.

AVERAGE TUITION FOR A PUBLIC FOUR-YEAR UNIVERSITY IS UP 33% SINCE 2000

Private student loans can be a good way to bridge the financing gap when federal loans aren't enough to cover college costs. Unlike federal loans, though, private student loan interest rates can vary from lender to lender depending on a borrower's creditworthiness.

If you decide to borrow private student loans, it's important to compare rates across multiple lenders on an online marketplace like Credible to ensure you're getting the best possible deal for your situation. And if you want to get an even lower rate, consider enlisting the help of a creditworthy cosigner like a parent or guardian.

7 IN 10 PARENTS SPENT MORE ON COLLEGE TUITION AND FEES THAN THEY EXPECTED, SURVEY FINDS

What to do with existing college debt

With the average cost of college outpacing inflation, it makes sense that student loan debt is also increasing at a high rate. The outstanding student loan debt in America is more than $1.75 trillion, according to the Federal Reserve — that's up about 20% in the past five years alone.

If you're trying to decide what to do with your student debt, you could consider refinancing to a private student loan at a lower interest rate. Refinancing to a lower rate can help you reduce your monthly payments, pay off your debt faster and even save thousands on the cost of interest over time.

It's important to note that refinancing your federal loans into a private loan would make you ineligible for certain federal benefits, like income-driven repayment plans, COVID-19 administrative forbearance and student loan forgiveness programs like Public Service Loan Forgiveness (PSLF).

See if refinancing to a private student loan is right for you by checking your free offers on Credible without impacting your credit score. Then, use a student loan refinancing calculator to view your estimated repayment terms.

MILLENNIAL, GEN Z GRADUATES PLAN TO LOWER STUDENT LOAN PAYMENTS WITH REFINANCING, SURVEY FINDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.