Public Service Loan Forgiveness program called ‘broken’ & ‘confusing’ after Biden admin. asks for feedback

98% of PSLF applications are rejected, typically because of an issue with the qualifying repayment plan. The Education Department has given borrowers the chance to submit feedback about the federal student loan program — here's what they're saying. (iStock)

A 65-year-old education professor who earned her doctorate degree in the 1980s is still repaying $137,000 worth of student loan debt — a balance that has ballooned over time thanks to ever-present interest.

A physician at the Department of Veterans Affairs who will continue serving veterans despite the fact that the private sector offers a considerably larger salary.

A public school teacher who wants to retire soon but needs to keep working to meet eligibility requirements.

These are just a few of the nearly 43,000 student loan borrowers who have shared their stories about the Public Service Loan Forgiveness (PSLF) program with the Department of Education.

PSLF is a student loan forgiveness program aimed at discharging the remaining balance of federal student loan debt for public servants — like nonprofit workers, government employees and military personnel — who have made 120 consecutive qualifying payments.

But since its inception, the program only has a 2% approval rate. That's because the program has strict requirements for a qualifying employer and eligible loans, as well as issues with student loan servicers and payment gaps during forbearance and deferment.

The Biden administration opened a public inquiry into the PSLF program, inviting borrowers to give their honest feedback:

"The system does not reward, nor fully inform or prepare, those who enter into public service."

"This whole student loan experience has caused me an enormous amount of stress and sleepless nights," wrote a 37-year-old public servant and father of three. "It is a burden that weighs not just on me, but also on my wife and the finances of our young family."

"If the goal is to help public service workers with student loan debt, why are some of us being penalized for having the wrong type of loan or repayment plans?" asked a borrower with more than $100,000 in student loan debt who has been an employee of the New York State court system for 18 years.

"The requirements for PSLF must be simplified and consistently applied, and borrowers should not be penalized for the actions of servicers, for the year they graduated, or for the changing rules of the program itself," said a borrower who has been employed by the federal government for 20 years.

While the Education Department's recent inquiry into PSLF gives borrowers a place to vent and provide recommendations to fix the program, many borrowers with public service jobs are still struggling to repay mountains of student loan debt.

Here are a few options for student loan repayment if you don't qualify for PSLF, including student loan refinancing. If you decide to refinance your private student loans, visit Credible to compare offers from multiple lenders without impacting your credit score.

TWO STUDENT LOAN SERVICERS, INCLUDING FEDLOAN SERVICING, END FEDERAL CONTRACTS

What to do if you don't qualify for PSLF

Student loan debt can stand in the way of achieving financial milestones like buying a house and saving for retirement — at least that's the story of one student loan borrower who gave feedback about the PSLF program. But thankfully, there are a few ways to make student loans more manageable. Consider your options below.

SENATE CONFIRMS JAMES KVAAL AS UNDER SECRETARY OF EDUCATION

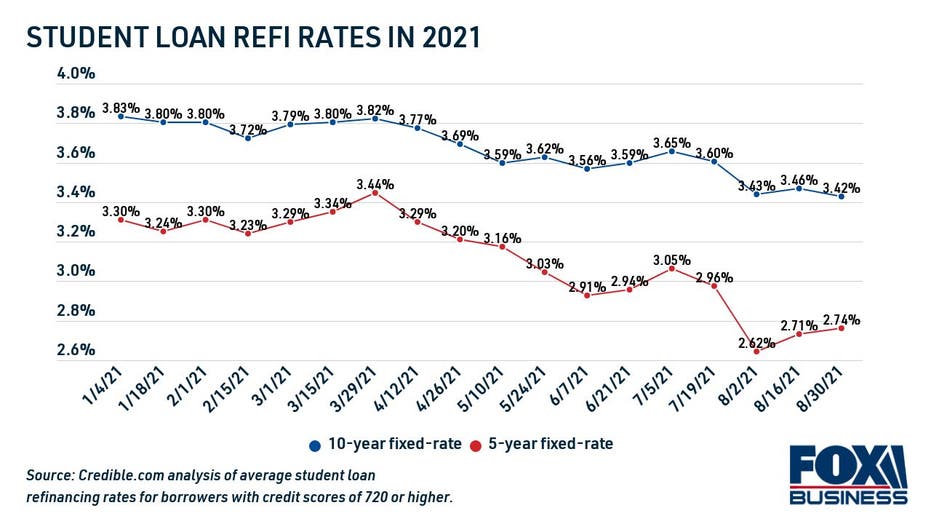

Refinance your student loans to a lower interest rate

Private student loan refinancing can potentially help you pay off your loans faster, lower your monthly payment and save money on interest over time. And since student loan refinance rates are near historic lows, there's never been a better time to refinance your private student loans for better terms.

If you're vying for PSLF eligibility, though, it's important to know that refinancing your federal student loans into a private student loan would make you ineligible for this student debt forgiveness program.

But you have nothing to lose by refinancing your private student loans to a lower interest rate. See student loan rates from real private lenders in the table below. Visit Credible to see your estimated student loan refinance rates across multiple lenders in just minutes.

35% OF MILLENNIALS SAY STUDENT LOAN DEBT IS PREVENTING THEM FROM BUYING A HOME

Research alternative student loan forgiveness programs

PSLF isn't the only student loan cancellation program available. There are plenty of student loan forgiveness programs that vary based on your career field or even your disability status. Here are a few programs you might consider if you don't qualify for PSLF:

- Teacher Loan Forgiveness Program. If you teach full-time for five consecutive academic years at a low-income school, you may be eligible for up to $17,5000 worth of federal student loan forgiveness. Learn more on the Federal Student Aid website.

- Borrower defense to repayment. Student loan borrowers who were defrauded by their college may qualify to have their federal loans discharged under the borrower defense program. The Biden administration has forgiven $1.5 billion worth of student loan debt under borrower defense.

- Military service loan forgiveness programs. The Army, Navy, Air Force and National Guard offer their own student loan forgiveness programs. For example, the Army’s College Loan Repayment Program will repay a third of your student loan debt every year for three years, up to $65,000 total.

The Biden administration has forgiven approximately $9.5 billion worth of student loan debt for more than half a million borrowers through total and permanent disability discharges, closed school discharges and the borrower defense program.

47K VETERANS AND ACTIVE-DUTY TROOPS WILL AUTOMATICALLY RECEIVE STUDENT LOAN RELIEF

Make more than the minimum payment on your student loans

When you're making the minimum payment on your student loans, a significant portion of that will be dedicated to interest while you're chipping away at the principal balance. But by making more than the minimum payment on your student loan debt, you're able to whittle down that principal balance while saving money on interest over the life of the loan.

You can use a student loan repayment calculator to estimate how much you can save on interest charges over time by making larger student loan payments.

FEDERAL DIRECT LOAN RATES JUMP NEARLY 1% IN JULY

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.