Personal loan rates could rise in March as Fed plans quarter-point rate hike

The central bank's economic outlook may impact consumer borrowing costs

Despite strong wage growth and a low unemployment rate, consumers are feeling the impacts of higher prices. The Fed is planning a March rate hike to address inflation, but it could impact personal loan rates. (iStock)

The Federal Reserve kept its benchmark rate near zero since March 2020 to boost economic recovery amid the COVID-19 pandemic. But with record-high annual inflation and a strong labor market, the Fed is planning to implement several rate hikes in 2022 starting this month.

When the central bank raises the federal funds rate, interest rates are likely to edge up on a number of financial products, including credit cards, private student loans, home equity lines of credit — and personal loans.

Keep reading to learn more about how the Fed's economic policy may impact personal loan rates, as well as how to get a low interest rate on a personal loan. One way is to compare rates across multiple lenders at once on Credible's online marketplace.

WHAT THE FED'S NEW ECONOMIC POLICY MEANS FOR MORTGAGE RATES

What Fed rate hikes could mean for personal loans

Lenders set consumer borrowing rates based on the prime rate, which is an economic index tracking the rates that banks charge their most creditworthy commercial borrowers. The prime rate is largely impacted by the federal funds rate.

A group of high-ranking Fed policymakers on the Federal Open Market Committee (FOMC) determine the federal funds rate, modifying the central bank's economic policy to match current conditions. The FOMC is keeping a close eye on inflation, which rose at an annual rate of 7.5% in January — nearly triple the Fed's 2% target.

Fed Chair Jerome Powell told lawmakers last week that he will propose a quarter-point rate hike during the March 15-16 FOMC meeting to curb high inflation. He added that Fed officials are "prepared to move more aggressively by raising the federal funds rate by more than 25 basis points" at future meetings.

"With inflation well above 2% and a strong labor market, we expect it will be appropriate to raise the target range for the federal funds rate at our meeting later this month," Powell said.

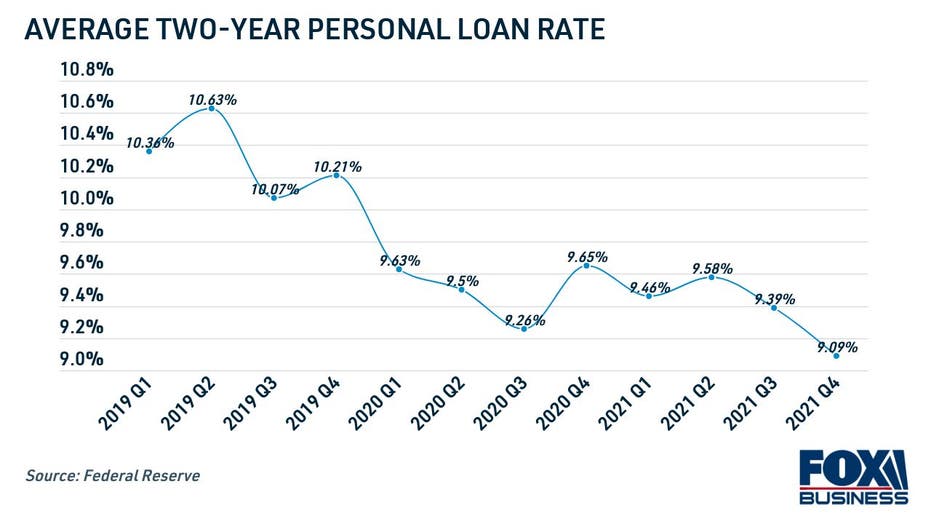

The upcoming rate hikes will impact the prime rate and likely cause borrowing costs to edge higher on a number of consumer borrowing products, including personal loans. Average personal loan rates reached historic lows in late 2021 due in part to the Fed's moderate economic policy, but they may begin to edge up as a result of rate hikes in 2022.

While personal loan lenders take the prime rate into account, they lean more heavily on other factors like an applicant's credit score and debt-to-income ratio (DTI) to determine interest rates. And because rates vary from one lender to the next, it's important to shop around across multiple lenders.

You can visit Credible to compare personal loan rates tailored to you for free without impacting your credit score.

PERSONAL LOAN RATES ARE MUCH LOWER IN 2022 THAN THEY WERE A YEAR AGO, DATA SHOWS

How to get a low personal loan rate

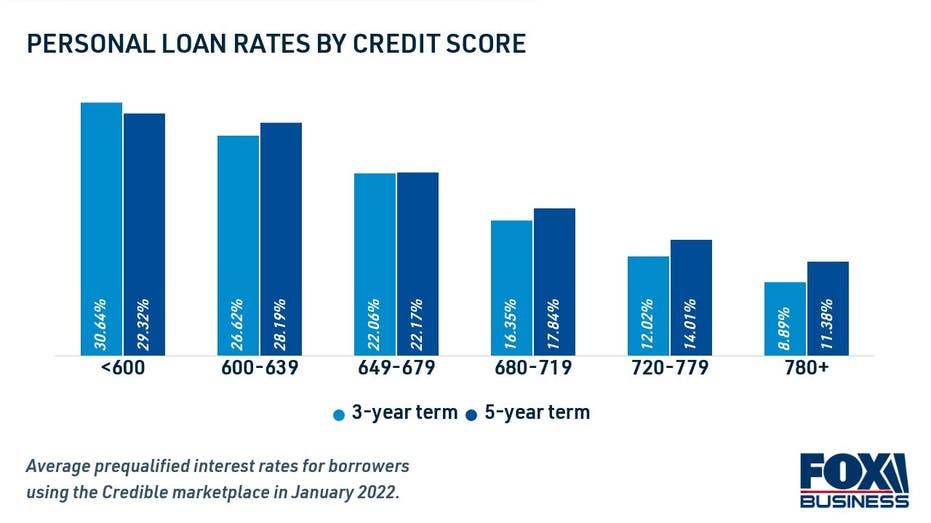

Although the Fed's March rate hike may impact average personal loan rates, there are a number of factors within your control that lenders consider when setting interest rates. Personal loan lenders lean heavily on your creditworthiness, including credit score and DTI, to determine your interest rate and eligibility

Applicants with very good to excellent credit, defined by the FICO scoring model as 740 or higher, will see the lowest personal loan rates. On the other hand, those with bad credit may see higher rates — if they qualify at all.

Here are a few tips for getting a low interest rate on a personal loan:

- Work on building your credit score. Improve your on-time payment history and lower your credit utilization, which is the amount of revolving debt you owe compared to the credit limit available to you. Also consider enrolling in free credit monitoring services on Credible.

- Reduce your debt burden. Ideally, lenders like to see a DTI ratio of 36% or lower. If you have excessive levels of debt, consider dedicating cash windfalls like tax refunds and work bonuses to paying down your current loans. Alternatively, you can search for ways to increase your income.

- Shop around with multiple lenders. Most personal loan lenders let you prequalify to see your estimated interest rate with a soft credit inquiry, which won't affect your credit score. That way, you can shop for the lowest rate possible.

You can browse current personal loan rates in the table below. Then, you can visit Credible to get prequalified through multiple lenders at once, so you can shop around for the best offer for your financial situation.

FORECAST: HERE'S WHAT THE HOUSING MARKET WILL LOOK LIKE IN 2022, ACCORDING TO AN EXPERT

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.