Can 2H Earnings Meet the Street’s Lofty Expectations?

Half time is over on Wall Street – and now the question is whether companies can meet analysts’ rosy earnings expectations.

Over the first six months of 2014, during which the U.S. experienced some severe weather as well as a rebound in the manufacturing economy and initial signs of widening inflation, the S&P 500 climbed 6%.

Getting ready for the second half of the year means taking a fresh look at what’s expected of the S&P 500 -- the index used by the majority of fund managers, and also one for which Wall Street furnishes earnings expectations and other data.

As we head into the back half of the year, even though the manufacturing economy is humming and it looks like China is at a minimum bottoming, there are several headwinds ahead. Among the potential hurdles are renewed concerns over the consumer, the start of an inflation pick-up amid rising input prices (food, energy, and manufacturing) and minimum-wage hikes.

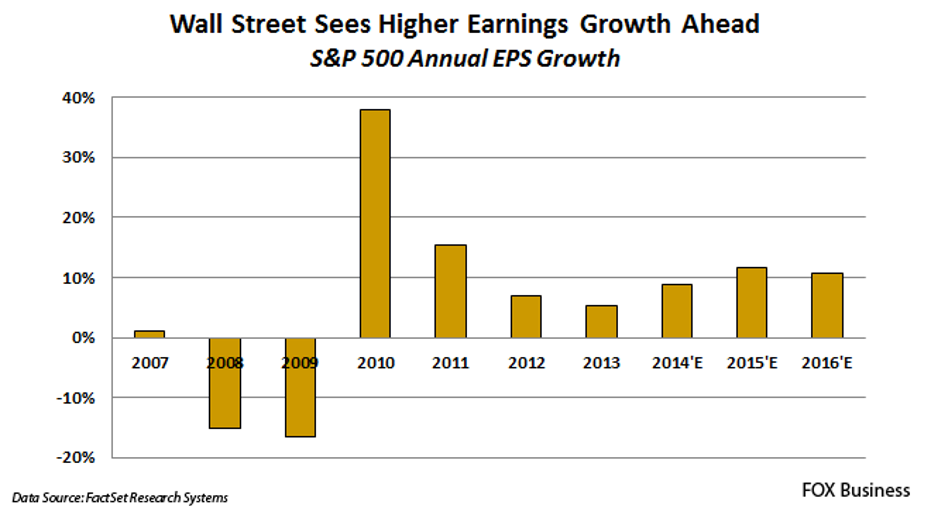

In light of all this, it's time to look at second-half and full-year earnings expectations for the S&P 500. Firms included in the S&P 500 are targeted to deliver earnings of $119.37 for 2014, up 6.2% from the year prior, according to FactSet Research Systems. Based on its recent closing price, the market is trading at 16.6x those earnings, which is not far off the 2001-to-2013 average multiple of 16.9x.

From the get-go, full-year 2014 earnings growth is projected to be slower than the mean -- 6.2% compared to an average of 8.7% from 2001 to 2013. Moreover, there are reasons to think the 2014 consensus expectation could be too optimistic.

Over the last few years, S&P 500 second-half earnings climbed 4.2% from the first half on average. This year, that growth is expected to come in at 9.4%. Granted, the first quarter had several issues this year, including severe weather that led to shutdowns at companies and even the federal government, but that expected growth still seems aggressive.

Another way of looking at it is to compare year-over-year earnings growth rates for the second half of 2014 vs. 2013. Comparing those factors, which removes seasonal variances, bears out the notion that earnings expectations are more than a tad aggressive. It may surprise you that 2014 second-half earnings are targeted to grow 11% year over year, even though such comparisons have only averaged 5.6% over the last few years.

Keep in mind too that gross domestic product comparisons year over year in the second half of 2014 won’t be as easy as they are with the first half of 2014. GDP reached 4.1% in 3Q 2013 before dipping to 2.6% in 4Q 2014 for a blended rate of 3.35% in the second half of 2013. Current GDP expectations for the second half of 2014 call for up to 3.5% growth – not significantly better than 2013.

For my money, second-half expectations are indeed aggressive and that’s before we receive company commentary both good and bad. Good – the rebounding manufacturing and housing economy. The bad – higher input costs, the impact of rising minimum wages, uncertain consumer spending and the risk of higher interest rates. That makes company commentary far more important compared to just a few months ago.

Time to Hone Your Portfolio

As I’ve learned over the last 20 years, however, it pays to check your opinion and let the data talk to you. In this case, the data will be the hundreds of corporate earnings reports that will start hitting the tape later this week. It all kicks off with Alcoa’s (NYSE:AA) earnings report after Tuesday’s New York market close. While there are other companies, such as Fastenal (NASDAQ:FAST) and Wells Fargo (NYSE:WFC), issuing their June quarter results next week the real deluge happens over next few weeks.

Putting all of this into a cocktail shaker, shaking and pouring it out suggests we could see some downward revisions ahead for S&P 500 earnings expectations. If that proves the case, it likely signals a topping out in the stock market following near daily new record highs of late.

If that happens and some froth comes out of the market in the form of a modest pullback, investors should welcome that opportunity to revisit well positioned companies that are poised to grow their earnings faster than the market and are trading at favorable risk-to-reward metrics. In other words, it’s time to sharpen your pencil and build you shopping list – I know I am.

Chris Versace owns none of the companies mentioned nor does The Thematic Growth Portfolio that he manages.