How Tech Is Boosting SMB Lending

Small business loan approvals at big banks have hit their highest levels since the credit crunch began in late 2008.

Following the mortgage bust, many big banks essentially turned off the spigot to small business lending. This always struck me as curious because prior to starting Biz2Credit.com, I analyzed loan portfolios of banks. My research found that small business lending was usually the most profitable part of bank lending.

When the so-called "credit crunch" hit, big banks in particular became extremely risk averse, and it became very difficult for entrepreneurs to secure capital -- even those who had proven themselves to be creditworthy borrowers. Meanwhile, many large financial institutions advertised that they were increasing their small business lending efforts and invested in hiring new staff to do so. This rang hollow at the time.

What happened is that other players filled the void in the marketplace. For example, credit unions decided to take advantage of this hole in the marketplace by increasing their small business loan-making. As did alternative lenders -- cash advance companies, factors, and others -- leveraging their investment in technologies that enabled them to make informed lending decisions in a short amount of time.

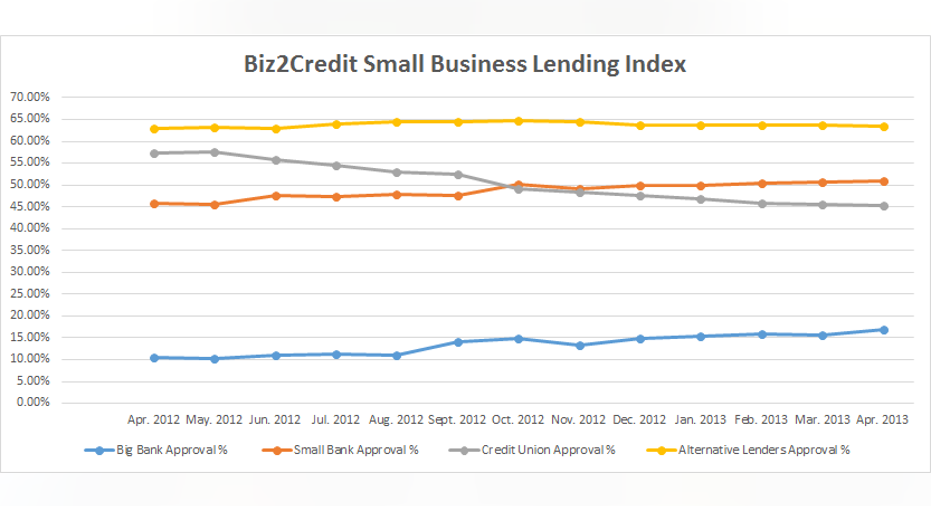

In 2012, credit unions and alternative lenders were the story in small business lending. In recent months, this has changed. Credit unions are handcuffed by a lending cap of 12.25% of their assets imposed by the Credit Union Membership Access Act of 1998. Thus, many of those who became active in small business lending quickly hit their limit. Meanwhile, the majority of credit unions still conduct business in a quaint, old-fashioned way in which one has to become a member of the credit union by going to the offices and filling out paperwork. In my opinion, the pace at which business is conducted in the 21st century renders this inefficient system as a hindrance to credit union profitability.

Conversely, cash advance companies, which specialized at making quick lending decisions and getting the money rapidly in the accounts of small business owners, cut out a niche for themselves in the small business lending marketplace. Entrepreneurs realized that they could get money to solve cash flow issues or to close a deal in which capital was needed quickly. However, they paid a premium for the availability of the funding in the form of higher interest rates.

I'm seeing a change in 2013. Big banks, many of which have not seen a rebound in mortgage lending, are reentering the small business lending game. They are taking advantage of their resources and automating their loan application processes. Thus, they are making better informed lending decisions in a shorter amount of time with less manpower. It is about time!

Actually, I have been amazed at how well big banks (defined as having $10B+ in assets) have made online banking more efficient, yet have made no technological improvements in the small business lending area. In recent weeks, I have met with numerous bank executives who tell me they are planning to make significant investments in online technologies in order to streamline the small business lending process. It is a topic that people have discussed with me not only here in America, but also at the International Finance Corporation (IFC) conference held in Dubai earlier this month.

Big banks are beginning to back up the marketing dollars spent on ad campaigns highlighting small business lending -- and are approving higher percentages of loan applications. According to the April Biz2Credit Small Business Lending Index, my company's monthly analysis of 1,000 loan applications, big banks are now granting 16.8% of funding requests. In a year-to-year comparison, approvals at big banks are up by more than 50%. Institutions such as TD Bank, Sovereign and Wells Fargo are investing heavily in new technology to increase speed and service of approvals. Others are in the process of preparing to do so.

Lending conditions are improving as the economy continues to rebound. Word is getting out that big banks have jumped back into small business lending. This bodes well for them, since the large institutions have better name recognitions and higher credit-quality customers tend to gravitate towards these lenders they know. This is especially true now that things seem to have improved in the economy overall.

The challenge now is for the small banks to react. The bigger banks may soon move into their territory, even though small banks have increased their approvals for the fifth consecutive month and are now granting about 51% of the applications they receive.

Small banks continue to be aggressive players in small business lending, but must maintain focus on advancements in technology to remain competitive in lending. Otherwise, big banks will eat their lunch. Big banks have the advantage of brand recognition and superior resources to invest in technological advancements. Additionally, they generally can offer lower interest rates on loans than small banks do. It is essential that small banks continue to make investments in their technology and process loans more rapidly to stay in the game.

Rohit Arora is co-founder and CEO of Biz2Credit, an online credit marketplace that connects small- and medium-sized businesses with a network of 1,100+ lenders, service providers, and complementary business tools. Having arranged $800 million in funding, Biz2Credit is a leading resource for loans, lines of credit, working capital and more. Follow Rohit on Twitter @Biz2Credit and on Facebook. http://www.facebook.com/businessloan.