What do Federal Reserve interest rate hikes mean for Main Street?

Higher interest rates means consumers will pay more to borrow

Fed expected to raise interest rates this week

Structured Finance Association CEO Michael Bright discusses what would happen for American families if the Fed raised interest rates on ‘Fox Business Tonight.’

The Federal Reserve is expected to announce a 50-basis point interest rate hike on Wednesday in what will be the second of several anticipated increases this year as the central bank seeks to combat soaring inflation, which is at a high not seen in four decades.

While the Fed's actions are closely monitored by Wall Street, people on Main Street will be impacted, too and should expect to pay more for car loans, mortgages and credit card balances.

The Federal Reserve building in Washington. ((AP Photo/Patrick Semansky, File) / Associated Press)

US COULD GET INTO AN INFLATIONARY SPIRAL ‘UNLIKE ANYTHING WE’VE SEEN': KEVIN HASSETT

AGGRESSIVE RATE HIKES PLANNED FOR 2022

John Lonski, president of Thru the Cycle and former chief capital markets economist at Moody's Analytics, says consumers might not feel the pain of the Fed's initial rate increase of 25 basis points earlier this year, but they will certainly notice the hikes if they continue through 2022 as policymakers have signaled.

After the 50 basis point hike on Wednesday, some economists say the Fed may be even more aggressive at other meetings this year, perhaps raising rates by 75 basis points.

Although a series of rate increases is expected, forecasting the Fed's behavior for the rest of the year is "a fool's errand" given the uncertainty with Russia's war on Ukraine, Lonski told FOX Business.

Federal Reserve Chair Jerome Powell listens during a Senate Banking Committee hearing on Capitol Hill in Washington. (Al Drago/The New York Times via AP, Pool / AP Newsroom)

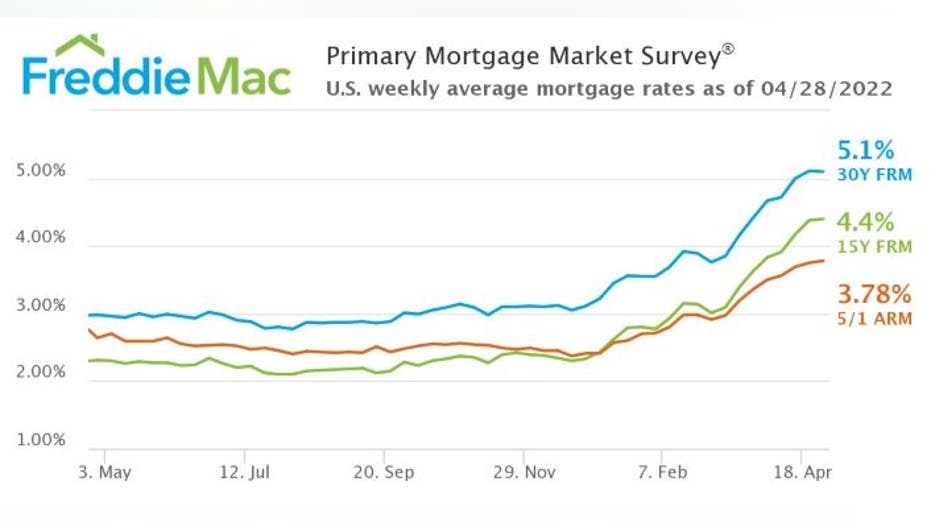

MORTGAGES

Rates for a 30-year fixed mortgage already crossed above 5% as tracked by Freddie Mac. So people considering the purchase of a house should not put it off – historically rates at these levels are still considered attractive.

While sky-high home prices have already made ownership unaffordable for many would-be buyers, higher rates may cool bidding wars.

FEDERAL RESERVE EXPECTED TO HIKE INTEREST RATES THIS WEEK, DESPITE UKRAINE VOLATILITY

CREDIT CARD DEBT - PAY IT DOWN OR ELIMINATE

In the meantime, Lonski says that anyone carrying credit card debt should work to pay down balances, especially with inflation at a 40-year high.

WIN FOR PLAIN VANILLA SAVERS

While savers can expect to earn more on their cash deposits as a result of rising interest rates, rates for savings accounts and CDs will rise at a slower pace.

"As banks raise the rates they lend at, they will want to make up for the compressed margins they have faced over the last several years due to the low-interest rate environment," says Certified Financial Planner Danielle Harrison, founder of Harrison Financial Planning in Columbia, Missouri.

According to Bankrate.com, Goldman’s Marcus and Capital One, are offering 0.6% on a savings account with no minimum deposit required.

| Ticker | Security | Last | Change | Change % |

|---|---|---|---|---|

| GS | THE GOLDMAN SACHS GROUP INC. | 1,039.61 | +7.03 | +0.68% |

| COF | CAPITAL ONE FINANCIAL CORP. | 217.76 | -2.24 | -1.02% |

"For savers, be wary of locking up your money in low-rate CDs in a rising rate environment," Harrison adds.

Is it too late for Fed to avoid triggering a recession?

Charles Schwab chief investment strategist Liz Ann Sonders discusses how the Fed can cool inflation on 'The Claman Countdown.'

RISING RATES AND INFLATION

Rising interest rates will have a direct impact on Americans, who are already struggling with soaring prices and wage gains that are insufficient to offset inflation.

"Inflation eats away at consumers' ability to pay their debts, it eats away at their ability to service their normal household needs," Structured Finance Association CEO Michael Bright told "FOX Business Tonight."

GET FOX BUSINESS ON THE GO BY CLICKING HERE

"It gets you either way," Bright said. "You can raise rates and squash inflation, but then borrowing costs go high. Or, you can let inflation run a little bit higher than it should … and that eats away at your ability to purchase."

The Fed's challenge is to implement rate increases without choking off growth and landing the U.S. in a recession.