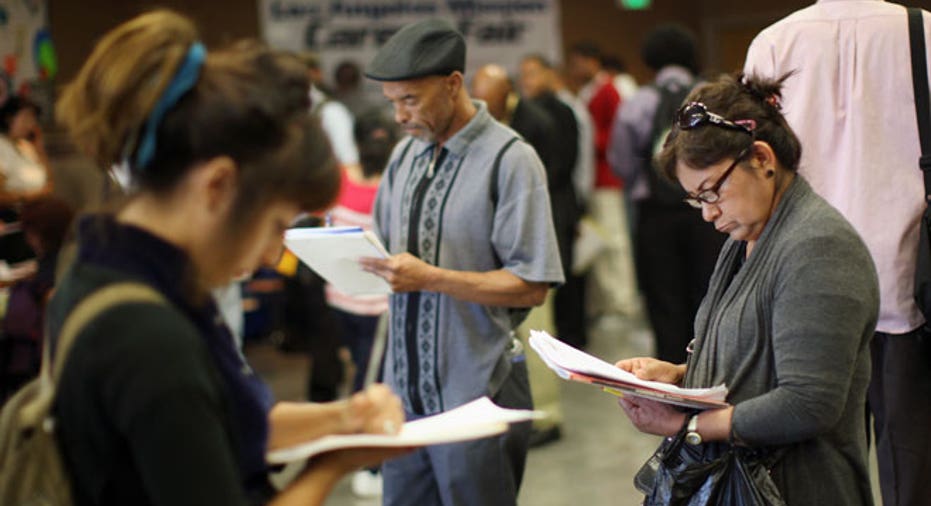

Economy Adds 223,000 Jobs in April; Unemployment Rate at 5.4%

The economy added 223,000 jobs in April and the unemployment rate dropped to 5.4%, a rebound from the dismal March report that led to concerns the U.S. labor market was heading into a prolonged skid.

Economists were nearly spot on in their predictions of a gain of 224,000 and that the unemployment rate would dip to 5.4%.

Wages rose by three cents per hour, or 0.1%, hardly at all from a month earlier. Meanwhile, the labor force participation rate was virtually unchanged at 62.8%. Both numbers are being closely watched by economists for signs that the labor market is strengthening beyond the headline unemployment rate.

“Weak wage growth remained the fly in the ointment of the labor market report, albeit with signs that pay pressures are gradually picking up, with average hourly earnings up 2.2% on a year ago,” Chris Williamson, chief economist at research firm Markit said.

The report is unlikely to clarify the Federal Reserve’s position on the timing and trajectory of interest rate hikes. Earlier this year, it seemed likely the central bank would start raising rates in mid-2015, possibly as early as its June meeting.

An array of lousy economic data released during the first quarter has delayed that plan, however. Another rough winter, a dock strike in California, the plunging price of oil and a surge in the value of the dollar cut into corporate profits, kept consumers home and negatively impacted hiring.

In March, just 85,000 new jobs were created, a figure that was revised lower than initially thought, while wages remained essentially stagnant and the labor participation rate, a key gauge of the percentage of Americans actually working, hovered at its lowest level in decades.

Williamson said the April rebound put a rate hike back on the table for later in 2015.

“The rebound in the economic data flow adds to the likelihood of the Fed opting to begin the process of gradually raising interest rates later this year, with September looking the most likely start date providing the data remain consistent with the moderate recovery story in coming months,” he said.

Analysts say signs of longer-term employment trends can be found by culling numbers from a handful of industries that serve as bellwethers for the broader economy. For instance, an increase in hiring in the mining and oil extraction sectors means that activity is likely picking up across-the-board in the sprawling energy sector.

Employment in mining fell by 15,000 in April, with most of the job loss in support activities for mining and in oil and gas extraction, according to the Labor Department. Since the beginning of the year, employment in mining has declined by 49,000, with losses concentrated in support activities for mining.

Construction and manufacturing are two other sectors eyed for improvement, construction in particular because it’s so closely tied to the all-important housing sector, an area of the economy that has lagged throughout the six-year, roller coaster recovery from the 2008 financial crisis.

Employment in construction rose by 45,000 in April, after changing little in March, the Labor Department reported.

In a sign that the March labor numbers may have been an anomaly, figures were released Thursday that showed the number of Americans filing new claims for unemployment benefits a week ago held near a 15-year low.

Initial claims for state unemployment benefits rose 3,000 to a seasonally adjusted 265,000 for the week ended May 2, the Labor Department reported. That was well below the increase to 280,000 that economists had forecast. Claims for the prior week were unrevised at 262,000, which was the lowest reading since April 2000.

Policy makers at the Fed will be closely watching Friday’s jobs report for signs of underlying strength, especially in the area average hourly wages. Months of wage stagnation has played a significant role in keeping inflation below the Fed’s 2% target rate.

The Fed is preparing to raise interest rates for the first time in nearly a decade, having lowered them to their current near-zero range in December 2008 at the height of the financial crisis. But they have vowed not to do so until they are convinced the economy is moving toward the Fed’s dual mandate of full employment and price stability, defined respectively as an unemployment rate of 5.2%-5.6% and inflation at about 2%.

The unemployment rate has reached that target range but inflation has proven more problematic. Despite the tightening labor market, wages have not risen in tandem with the falling unemployment rate.