Student loan refinancing is cheaper than ever as interest rates set new record lows

Locking in a low rate through a private lender can help you reduce your student loan payments

Find out if qualifying for a lower interest rate on your education loans can help you achieve better loan repayment terms. (iStock)

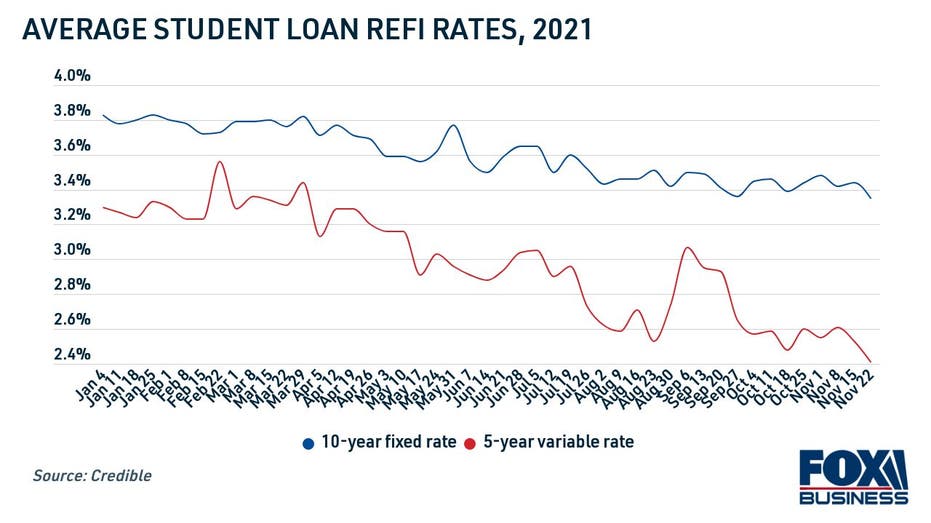

If you've been considering refinancing to save money on your student loan debt, there's never been a better time to do so. That's because student loan refinance rates just fell to an all-time low, according to Credible data.

Average student loan rates for the 10-year fixed-rate term fell to 3.35% for the week of Nov. 22, which is down from 3.95% a year ago. Rates are even lower for a 5-year variable-rate student loan refinance, at 2.41% compared with 3.14% last year.

Keep reading to learn more about student loan refinancing to decide if this option is right for you. You can visit Credible to compare student loan refinance rates for free without impacting your credit score.

STUDENT DEBT REFINANCE VS. LOAN CONSOLIDATION: WHAT'S THE DIFFERENCE?

How to decide if student loan refinancing is right for you

Student loan refinancing can help borrowers lower their monthly payments, pay off their debt faster and save money on interest over the life of the loan. Still, you should consider your unique financial situation to decide if this repayment option is beneficial for your needs.

Here's how to know if you should refinance your student loans:

- Gather your current loan documents. You'll want to know your type of loan, monthly payment, interest rate, loan balance and remaining repayment term. You should also check your credit report to get a good idea of where you stand.

- Get prequalified to see your potential repayment terms. You can view your estimated student loan refinancing rate without impacting your credit score with a process known as prequalification. This way, you can view your new loan terms without a hard credit check.

- Use a student loan refinance calculator to estimate your savings. You can see how changing your repayment period and loan type — like a variable interest rate or fixed interest rate — impacts your overall interest paid and monthly payments.

It's also important to note that refinancing your federal student loans into a private student loan will make you ineligible for certain government protections and benefits, such as income-driven repayment plans, federal forbearance options and select student loan forgiveness programs.

You can browse current student loan rates from real lenders in the table below and get prequalified on Credible to see your estimated rate with a soft credit inquiry.

BIDEN ADMINISTRATION BEGINS NOTIFYING BORROWERS OF STUDENT LOAN SERVICER CHANGES

Get a lower student loan rate with a cosigner

The eligibility requirements for student loan refinancing can be prohibitive for borrowers without an established credit history or a good debt-to-income ratio. If this is the case for you, consider enlisting the help of a creditworthy cosigner.

A cosigner is typically a trusted friend or relative with a good credit score who is willing to borrow the loan with you. Since both of your names and credit profiles will be used in the application process, you will share responsibility for repaying the loan. If you default on the loan, it will have a negative impact on your cosigner, too.

Student loan interest rates are determined in part by a borrower's credit score, which means that refinancing your loans with a cosigner may also help you qualify for a lower rate. By getting the lowest rate possible on your new loan, you'll be able to save even more on your student loan debt.

You can learn more about student loan refinancing by getting in touch with a knowledgeable loan officer at Credible.

PARENT PLUS LOANS VS. PRIVATE STUDENT LOANS: WHICH HAS BETTER RATES?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.