Homeowners cash in on refinancing as mortgage rates fall, MBA finds

Mortgage refinance demand was up 7% last week, according to the latest MBA data

See how refinancing to a new mortgage with a lower interest rate can save you money over the life of the loan. (iStock)

Homeowners are rushing to refinance as mortgage rates have dropped in the past two weeks, according to new data from the Mortgage Bankers Association (MBA).

Mortgage applications increased 5.5% for the week of Nov. 5 from the previous week. Demand for mortgage refinancing increased even more as "homeowners acted on the decrease in rates," according to a statement from Joel Kan, associate vice president of economic and industry forecasting at the MBA.

"Refinance activity was up 7% overall, with gains in both conventional and government refinances," Kan said. "Additionally, the average loan balance for a refinance application was the highest in a month."

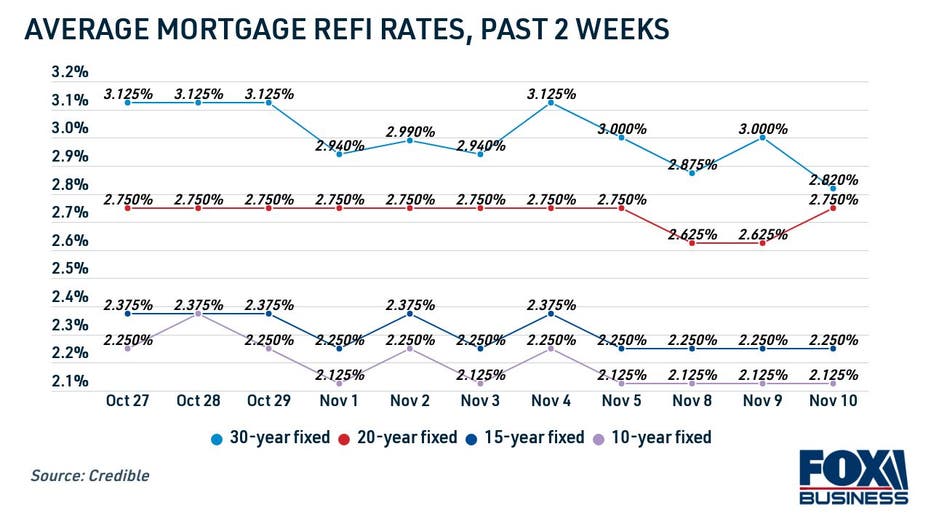

Well-qualified borrowers who refinanced on Credible's online loan marketplace are locking in average 30-year mortgage rates at or below 3% in early November.

Rates were even lower for the 15-year and 10-year fixed-rate mortgages, which are popular options for homeowners looking to refinance to a shorter term. For the 15-year mortgage term, the average rate has settled at 2.250% for the week. The average 10-year refinance rate was 2.125% for the same time period.

ADJUSTABLE-RATE MORTGAGES HAVE OBVIOUS ADVANTAGES FOR HOMEOWNERS

Now is a good time to refinance a mortgage with interest rates trending downward over the past few weeks. And since experts predict that mortgage interest rates will rise in the next two years, time is running out to lock in a historically low rate.

Keep reading to learn more about mortgage refinancing, and visit Credible to compare interest rates tailored to you without impacting your credit score.

HOW TO GET THE BEST HOMEOWNERS INSURANCE POLICY FOR YOUR NEEDS

Is it still a good time to refinance a mortgage?

Mortgage rates for the popular 30-year purchase term fell to record lows in January 2021, according to Freddie Mac. For the 15-year refinance term, interest rates were their lowest in September 2021. Despite the fact that mortgage rates have risen since then, it's still a good time for many homeowners to refinance.

That's because mortgage rates are likely to rise over the next few years, according to the MBA's most recent Mortgage Market Forecast. The MBA predicts that the average rate on a 30-year fixed-rate mortgage will reach 4.0% in 2022 and 4.2% in 2023.

The time is now to lock in a mortgage refinancing offer before rates inevitably rise. Get in touch with a knowledgeable loan officer at Credible who can guide you through the mortgage refinancing process.

REFINANCING AN FHA LOAN? HERE'S EVERYTHING YOU NEED TO KNOW

How to decide if you should refinance

Millions of homeowners still haven't taken advantage of record-low mortgage rates over the past year to refinance their mortgages, data shows. And while many homeowners can still benefit from mortgage refinancing, it may not be worthwhile for everyone.

Here's how you can determine if you should refinance your mortgage now:

- Your current mortgage rate. Look at your existing mortgage terms to determine your current interest rate. It may be worthwhile to refinance if you can shave your mortgage rate by about half a percent, depending on your circumstances, according to Credible.

- Your new monthly payments. Locking in a lower interest rate may help you lower your monthly mortgage payments while keeping the same mortgage term. If you want to reduce your mortgage payment further, you could also consider refinancing to a longer term.

- The overall interest paid. Refinancing to a longer-term mortgage loan may help you lower your monthly payments, but it could cost you more in interest charges over the life of your loan. Refinancing to a shorter mortgage term can make it possible to pay off your mortgage faster but it may result in higher monthly payments.

- Closing costs. Upfront fees like closing costs typically run about 2% to 5% of the loan amount, and they can be rolled into the total cost of the home loan. Make sure your overall interest savings exceed the closing costs.

- Private mortgage insurance (PMI). If you're considering a cash-out refinance, keep an eye on your home's equity. Mortgage lenders typically require PMI if you have less than 20% equity in your home.

VETERANS BORROWING VA LOANS AT A RECORD PACE, STUDY SHOWS

Once you know your current mortgage rate, see if you may qualify for a lower rate in just 3 minutes by getting prequalified on Credible. Then, use a mortgage calculator to estimate your new monthly payments and overall interest costs to decide if refinancing is worth it.

CAN YOU BUY A HOUSE WITH LESS THAN 20% DOWN PAYMENT?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.