Homeowners can potentially miss out on $300+ monthly savings by not refinancing, data shows

Here's how to lock in a low mortgage refinancing rate now

Although interest rates are predicted to rise, it's not too late to take advantage of current low mortgage refinance rates. According to some estimates, getting a lower interest rate on your new mortgage can save you hundreds of dollars on your month (iStock)

Millions of American homeowners were able to take advantage of historically low interest rates over the past two years to refinance their mortgages. Nearly half of mortgage borrowers who refinanced were able to lower their monthly payments by more than $300, and 18% lowered their payments by more than $500, according to a recent report from Zillow.

If you own a home and haven't yet refinanced your mortgage, now is the time to do so. Mortgage rates can't stay at this bargain level forever — in fact, they're already starting to creep up.

But despite rising mortgage rate averages, it's still not too late to lock in a lower rate on your home loan. Failure to refinance while rates are low can mean leaving money on the table, often amounting to hundreds of dollars each month — or tens of thousands of dollars over time.

You can get the mortgage refinancing process started on Credible, where you can compare mortgage refinance rates for free without impacting your credit score.

CASH-OUT REFINANCE VS. HOME EQUITY LOAN: WHICH TO PICK

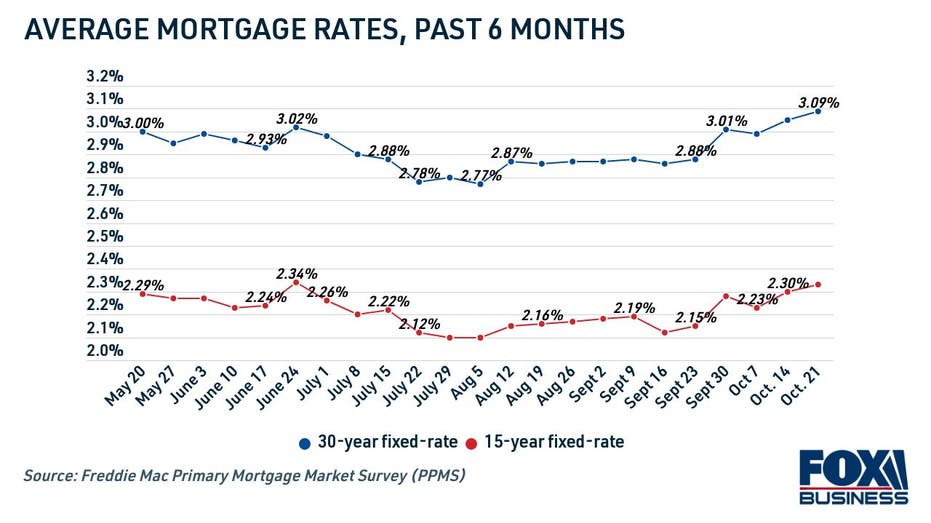

Mortgage rates continue to edge higher, but remain low

At the end of September, 30-year mortgage rates broke above 3% for the first time since June, per Freddie Mac data. Rates on 30-year mortgages have since risen to 3.09% as of Oct. 22, and industry experts agree that the days of sub-3% mortgage rates may not return anytime soon.

The Federal Reserve predicts a rate hike in 2022, which will cause mortgage rates to rise. The Mortgage Bankers Association (MBA) forecasts that 30-year rates will reach 4.0% in 2022 and 4.3% in 2023.

SHORTER-TERM MORTGAGE REFINANCE RATES CREEP UP, BUT STILL IN BARGAIN TERRITORY

Shorter-term loans typically offer lower rates. Rates on 15-year mortgages, which are a popular choice for homeowners looking to refinance and pay off their home loans faster, are still near all-time lows. The average 15-year mortgage rate fell to a record 2.10% in July, with current rates hovering at 2.30% as of October.

You can browse today's interest rates from real mortgage lenders in the rate table below. To get rate information tailored to you, get prequalified on Credible's online loan marketplace.

SHOULD I REFINANCE MY ADJUSTABLE-RATE MORTGAGE NOW?

How to refinance to a lower mortgage rate

With such a lucrative opportunity to save money on a home loan, it's a wonder why millions of homeowners still haven't refinanced their mortgages. Unfortunately, one of the primary reasons why Americans have passed up on this opportunity is because they don't understand the process — about 29% of homeowners surveyed by Zillow said so.

But mortgage refinancing may be simpler than you think. Just follow these steps, and you'll start saving on your housing costs in no time.

WHAT IS PRIVATE MORTGAGE INSURANCE (PMI) AND HOW DOES IT WORK?

1. Check your credit score, and build it if necessary

There are many factors beyond your control that determine mortgage rates, but there's one thing you can control: your credit score. Applicants with good or better credit scores will see the lowest interest rates, and those with bad credit will likely see higher rates.

Before you refinance, you should check your credit score to see where you stand. If your credit score is below 620, you should take some steps to raise it before applying for a mortgage refinance:

- Keep making payments on time. Your on-time payment history is one of the most important factors in determining your credit score, so consider setting up automatic payments if you're worried you'll miss a bill.

- Lower your credit utilization. Taking out a personal loan for debt consolidation may improve your credit score by lowering your credit balances and adding a new mix of credit to your profile.

- Open a secured credit card. Also known as credit-builder credit cards, secured cards can help you boost your credit score with on-time payments.

Once your credit score is sufficient, you're ready to begin the mortgage refinance process.

SHOULD YOU PAY DISCOUNT POINTS TO LOWER YOUR MORTGAGE RATE?

2. Compare offers from multiple lenders

This is perhaps the most important step in ensuring you lock in the best rate possible for your situation. Mortgage rates vary across refinancing lenders, which is why it's so important to estimate your interest rate with multiple lenders before you apply.

You can compare mortgage refinance offers from a variety of lenders for free on Credible. It's easy to get started, and doing so will not hurt your credit score.

MORTGAGE ORIGINATION FEES: WHAT ARE THEY AND HOW TO AVOID THEM

3. Choose a refinancing offer and formally apply

Typically, you'll want to choose the lender and loan term that offers you the lowest possible mortgage rate to help you save the most money on your monthly payments and over the life of your loan. Once you've selected a lender, a mortgage broker will guide you through the refinancing process.

Keep in mind that you'll also have to pay closing costs, which are typically 2-5% of the loan amount. These can typically be rolled into the total cost of the loan, so you don't have to worry about coming up with the cash upfront. The annual percentage rate (APR) on your home loan includes these fees as well as the refinance rate.

You can learn more about the mortgage refinancing process by contacting a knowledgeable loan officer at Credible, and you can also use a mortgage refinance calculator to determine if getting a new loan is worth it.

REFINANCING AN FHA LOAN? HERE'S EVERYTHING YOU NEED TO KNOW

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.