Mortgage rates sank from 5% to 3% since 2018: Why you should refinance now

Mortgage interest rates dipped below 3% for a 30-year loan, which is good news for consumers. Current mortgage borrowers and prospective homeowners alike can benefit from today's mortgage rate environment. (iStock)

Considering buying a home or refinancing your current mortgage? Don't miss out on the chance to lock in a historically low mortgage interest rate.

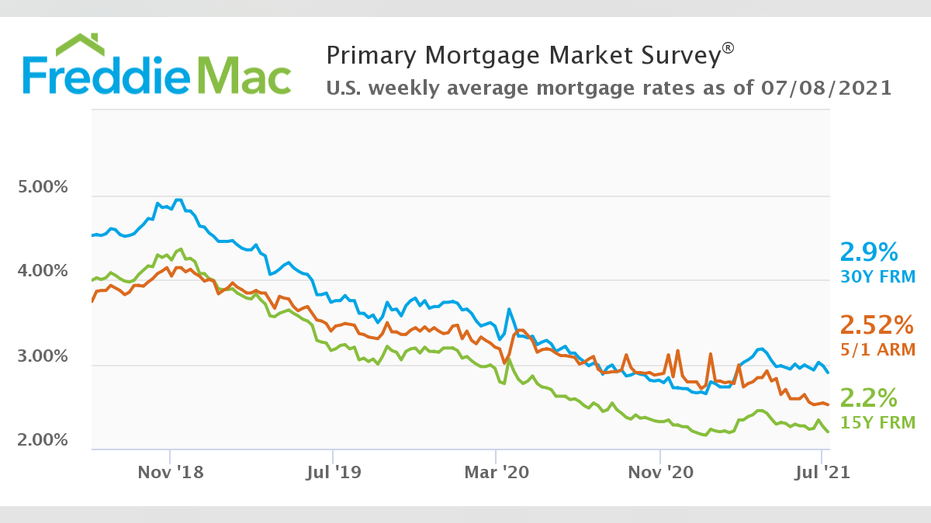

Mortgage rates are holding steady below 3% for the standard 30-year mortgage, according to the latest survey from Freddie Mac. Rates are even lower for 15-year mortgages, hovering at 2.2% for this popular refinancing option.

Even when compared with just three years ago, mortgage rates are extremely low. In 2018, 30-year rates reached nearly 5%, and they didn't ever dip below 3% until last year.

15 OF THE BEST MORTGAGE REFINANCE COMPANIES FOR 2021

But with talks of future rate hikes from the Federal Reserve, experts estimate that mortgage rates will rise again soon. The Mortgage Bankers Association (MBA) forecasts that mortgage rates will average 4.9% in 2023. The bottom line: If you've been waiting for a sign to refinance your mortgage or take out a home purchase loan, this is it.

The mortgage rates reported by Freddie Mac are just a weekly average, but you may qualify for even lower rates, depending on your financial situation. The rate table below shows estimated interest rates offered by real mortgage lenders, and you can check mortgage refinance rates without impacting your credit score on Credible.

SHOULD YOU PAY DISCOUNT POINTS TO LOWER YOUR MORTGAGE RATE?

Why should you refinance your mortgage?

It's no secret that there's never been a better time to refinance your mortgage. By snagging a historically low interest rate, you can save yourself money immediately and also in the long run. Here are some ways refinancing can affect your loan terms:

- Pay off your mortgage faster by switching to a 15-year mortgage. Your monthly mortgage payment may slightly increase, but you could save tens of thousands of dollars over the life of your loan — and get out of mortgage debt in half the time.

- Reduce your monthly payments by refinancing to a longer term. If you just bought your home within the past few years, it may be worthwhile to refinance to a 30-year mortgage to drastically lower your mortgage payment.

- Tap into your home's growing equity with a cash-out refinance. With home values at an all-time high, you may be able to take out a bigger mortgage amount than your current loan balance and pocket the difference to spend as you see fit.

The primary drawback to mortgage refinancing is the closing costs, but those are nominal and are typically recuperated within the first few years of refinancing. As long as you plan on staying in your home long enough to offset the fees — and you can secure a lower mortgage rate than what you're currently paying — then refinancing is a no-brainer.

When you refinance your mortgage, be sure to compare offers to make sure you're getting the lowest mortgage rate for your financial situation. You can compare rates across multiple lenders in just minutes on Credible's online loan marketplace.

SHOULD I REFINANCE MY ADJUSTABLE-RATE MORTGAGE NOW?

By the numbers: See how refinancing can reduce interest costs by nearly $100K

You've probably heard that refinancing your mortgage can save you a considerable amount of cash, but it's hard to imagine the potential savings when calculating such large sums of money. The following example shows how mortgage refinancing can save a homeowner nearly $100,000 in interest over the life of the loan.

Let's say you bought a home for $400,000 in October 2018 when mortgage rates were averaging 4.90%. Assuming a 20% down payment of $80,000 and a total loan amount of $320,000, here's what your mortgage would look like by July 2021:

- Monthly payment: $1,698

- Remaining loan balance: $306,194

- Interest paid up to July 2021: $42,239

By the time you pay off your mortgage in October of 2048, the total cost of the loan would be $611,397 after you've paid $291,397 in interest.

EVERYTHING YOU NEED TO KNOW ABOUT REFINANCING FHA LOANS

But taking advantage of current refinance rates can save you tens of thousands of dollars in interest and help you lower your monthly payment. Mortgage rates sank to 2.90% in July 2021, a full two percentage points lower than they were just a few years ago.

Assuming mortgage refinancing will cost you 1.5% of the total loan amount, closing costs will be about $4,500. Here's what would happen if you financed the remaining balance plus closing costs ($310,787) into a 30-year mortgage with a 2.9% mortgage rate:

- Monthly payment: $1,294

- Total interest paid: $197,144

- Interest savings over time: $94,253

In addition to saving nearly $100,000 in interest over the life of the home loan, you'll also cut your monthly mortgage payment by more than $400. Use Credible's mortgage payment calculator to see how much you can save by refinancing your remaining mortgage balance to a lower interest rate.

If you still need guidance, get in touch with a loan officer at Credible who can walk you through the mortgage loans process and help you decide if refinancing is right for you.

DO YOU NEED MORTGAGE INSURANCE?

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.