How student loans work

Both federal and private student loans can help you finance your college education — but you’ll have to repay them with interest once you leave school

Wondering how student loans work? Here’s the difference between federal and private student loans, including interest rates, repayment plans, and how to apply. (iStock)

Borrowing money can be a complex process, especially when you’re borrowing for something as important as funding your education. Headlines that dub America’s student loan debt a "crisis" and talk on Capitol Hill of forgiving federal student loans may have you wondering how student loans work — and whether they’re a good idea to pay for college.

While student loans can be a helpful tool, no one financial solution is right for everyone. It’s important to understand how student loans work before you sign for a loan.

If you need a student loan, comparison shopping is an important way to ensure you get the best one for your situation. Credible makes it easy to compare private student loan rates from multiple lenders.

- What are student loans?

- What to know about federal student loans

- What to know about private student loans

- How to apply for student loans

- How does student loan interest work?

- Repaying your student loans

What are student loans?

Student loans are specialized loans designed to help you fund the cost of your education. You’ll have to repay them with interest over an agreed-up repayment term. Depending on the type of loan and the terms you’ve agreed to, you may be able to defer paying your loans until after graduation or you’ve dropped to less than half-time enrollment.

Two types of student loans are available to borrowers who need help funding their education:

- Federal student loans — The U.S. Department of Education makes these loans, which typically come with benefits not available with private student loans.

- Private student loans — Borrowers can take out a loan from a private lender (typically from a financial institution) with varying terms and interest rates.

Before you consider taking out a loan to help pay for college, you should exhaust all your free aid options first. Complete the Free Application for Federal Student Aid (FAFSA) to see what grants, work-study, or other federal aid you may qualify for. When you’ve tapped out those options, you can think about student loans.

What to know about federal student loans

If you’re thinking of taking out a loan to help pay for college, it’s best to start with federal student loans.

These loans have fixed interest rates that are usually lower than those for private student loans, and they’re easier to qualify for. Plus, federal student loans come with perks and protections private loans don’t offer, such as:

- Federal student loan borrowers may be eligible for loan forgiveness.

- Income-driven repayment plans set your monthly payment at an affordable amount based on your income and household size.

Most federal student loans don’t require a cosigner or credit check. The Department of Education offers several types of federal student loans:

- Direct Subsidized Loans — Direct Subsidized Loans are for undergraduate students with demonstrated financial need for assistance. If you qualify for this type of loan, the government pays the interest while you’re in school at least half-time, whenever your loan is in deferral, and up to six months after you leave school.

- Direct Unsubsidized Loans — These loans are available to undergraduate, graduate, or professional students, and you don’t have to prove financial need to qualify for one. The Department of Education doesn’t pay the interest on unsubsidized loans. When you leave school, the unpaid accrued interest will be added to your loan balance — although you do have the option to make interest-only payments while you’re still in school.

- Direct PLUS Loans — PLUS Loans are available to graduate and professional students, as well as parents of undergraduate students. You’ll have to go through a credit check. If you have adverse credit history, you may still be able to get a PLUS Loan with a cosigner who has good credit.

- Direct Consolidation Loans — Borrowers who have multiple federal student loans can combine them into a Direct Consolidation Loan with one loan servicer and one monthly payment. However, consolidating won’t ensure you get a lower interest rate — your interest rate on the Direct Consolidation Loan will be the weighted average of the interest rates on the loans you consolidate.

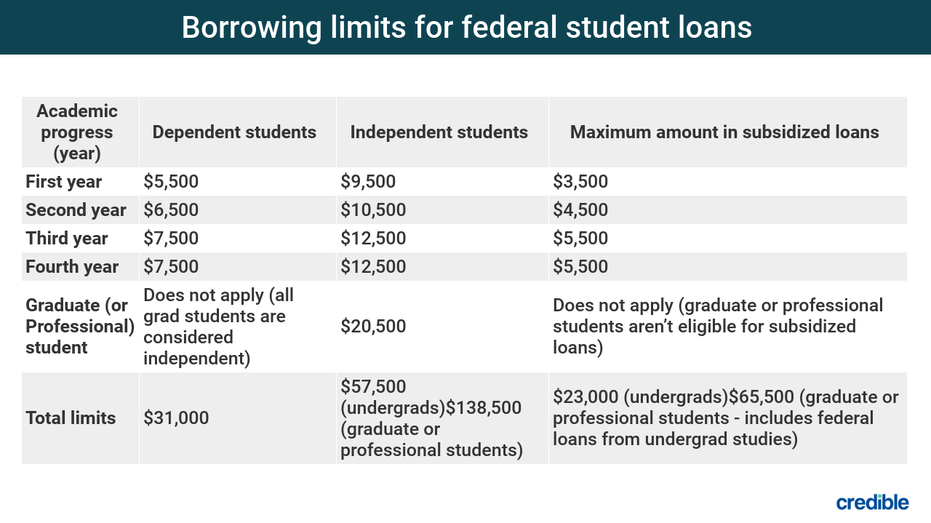

How much can you borrow with a federal student loan?

Federal student loan limits vary depending on the type of loan you borrow and whether you’re an undergraduate or graduate student.

(Credible)

What to know about private student loans

Banks, financial institutions, and online lenders typically make private student loans, which can have fixed or variable interest rates. Unlike federal student loans, private lenders will take into account your credit score and other financial details.

To get a loan through a private lender, you’ll need to submit an application with detailed information, such as your address and income. Loan terms and interest rates will vary based on the information you submit, and whether you’re an undergraduate, graduate, or professional student. Some lenders offer private student loans to parents, or an option to be a cosigner.

When you’ve exhausted your federal aid and loan options, private student loans can be a way to cover any funding gaps. Lenders may offer you different repayment terms, but you won’t be able to take advantage of programs such as federal loan forgiveness.

If you’re considering a private student loan, comparison shopping can help ensure you find the best rate and deal available to you. With Credible, you can easily compare private student loan rates from multiple lenders in minutes — without affecting your credit.

How much can you borrow with a private student loan?

Unlike federal student loans, which have specific dollar amount caps set by law, the amount you can take out in private student loans will depend on the lender. Many lenders have a minimum amount you’ll need to borrow, and the maximum amount is typically the cost of attendance at your school.

Keep in mind, though, that private lenders consider your ability to repay the loan when deciding how much you can borrow. They’ll look at your existing debt (if any) and will consider how much of your monthly income will need to go toward repaying your private student loan.

If you’re a student, you may not have much credit history or income. A private lender may require you to have a cosigner with good credit and sufficient income to repay the loan if you’re unable to.

HOW TO FIND STUDENT LOANS WITHOUT A COSIGNER

How to apply for student loans

When you’re ready to apply for student loans, here are the steps you’ll need to take for each type of loan:

Federal student loans

- Gather all necessary documentation. Information you'll need includes your Social Security number, contact details, the list of schools you plan on pursuing, tax information such as you or your parents' tax returns, and a list of assets.

- Fill out the FAFSA. The Free Application for Federal Student Aid qualifies you for federal financial aid such as loans, grants, and scholarships. You can fill out the FAFSA as soon as October of each year for the following school year.

- Review your SAR. After completing the FAFSA, you’ll receive a Student Aid Report (SAR), which outlines all the details you've submitted on the FAFSA. It also includes your Expected Family Contribution (the amount the Department of Education says your family should be able to pay toward your education) and an estimate of your eligibility for federal loans or grants.

- Review and accept financial aid offers. Depending on your financial situation, your school will offer you certain types of financial aid. Make sure to review all the terms so you understand what you’re getting into.

Once you’ve accepted the loan terms, the lender will disburse funds to your school. In turn, your school will apply the money toward your tuition, fees, and on-campus housing first. Any leftover funds will be disbursed to you, typically a minimum of two times per academic year.

Private student loans

- Compare rates and lenders. Before applying for a loan, you should compare interest rates from multiple lenders. This can help you get an idea of how much a private student loan might cost you, and if you’ll need a cosigner to secure one.

- Consider applying with a cosigner. Having a cosigner with good to excellent credit can help you get a loan at the most favorable rates and terms available to you.

- Gather documents. Put together the financial information you’ll need to apply, such as your current income and debts.

- Submit an application. You can apply for most private student loans directly on the lender’s website. For many lenders, you can also apply through a marketplace like Credible.

- Get your funds. As with federal loans, private lenders will send your loan funds directly to your school to apply toward your on-campus expenses.

STUDENT LOANS FOR BAD CREDIT — HERE ARE YOUR BEST OPTIONS

How does student loan interest work?

The amount of student loan interest you’ll pay will depend on factors such as the amount you borrow and whether you have a fixed- or variable-rate loan.

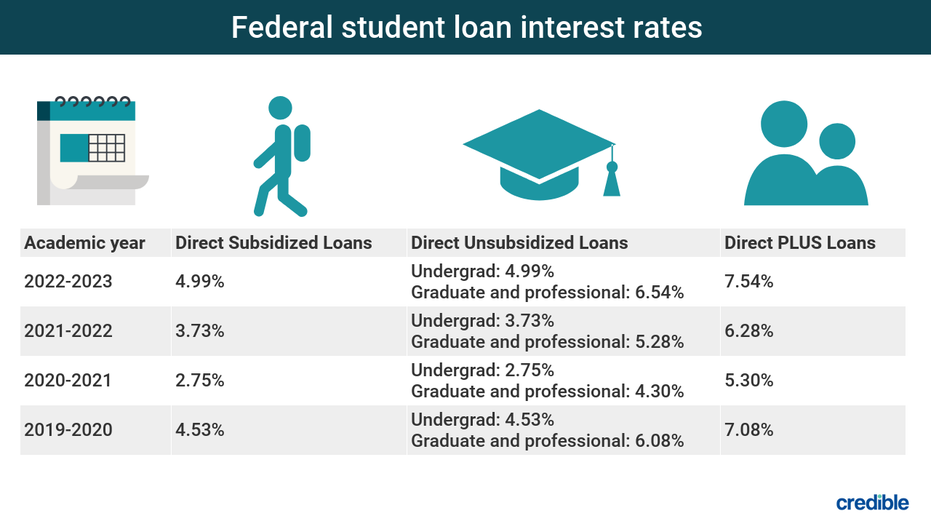

Federal student loans have fixed interest rates, meaning you’ll pay the same rate throughout your loan and have predictable monthly payments. Fixed interest rates may cost you less overall since federal student loan interest rates tend to be lower than private student loan interest rates.

(Credible)

With private student loans, interest rates can be both fixed and variable. With variable interest, the rate could change based on market conditions, which could cause your monthly payment amount to change. While many variable-rate loans charge less interest initially, the rate may increase over time, which means you could pay more in interest.

The table below shows current interest rate information for Credible’s private student lender partners.

Repaying your student loans

Exactly when and how you’ll need to repay student loans will depend on the type of loan you borrowed.

Federal student loans

For Direct, FFEL, and Grad PLUS federal student loans, you don’t have to begin repaying your loans until six months after you graduate, drop below half-time enrollment, or leave school — this is called a grace period. For Perkins Loans, the grace period is nine months, and for Parent PLUS Loans, there’s no grace period at all.

You’ll make payments to the federal loan servicer assigned to you by the Department of Education.

All federal student loans start off with a 10-year repayment period, during which you’ll make fixed principal and interest payments. You can also opt for a Graduated Repayment Plan that increases your payment amount every two years over a 10-year period. Or, you can choose an Extended Repayment Plan that gives you 25 years to pay off your loans with fixed or graduated payments.

If you’re having trouble making your payments under one of those plans, you can switch to an income-driven repayment (IDR) plan that bases your monthly payment on your income and household size.

The Department of Education offers four IDR plans:

- Revised Pay As You Earn Repayment Plan (REPAYE) — Loan terms are from 20 to 25 years, depending on whether the loan was for undergraduate or graduate studies. Payments are the equivalent of 10% of your discretionary income.

- Pay As You Earn Repayment Plan (PAYE) — Loan terms are up to 20 years and are the equivalent of 10% of your discretionary income, but never more than you’d pay with a Standard Repayment Plan.

- Income-Based Repayment Plan (IBR) — Loan terms are for 20 or 25 years and monthly payments are either 10% or 15% of your discretionary income.

- Income-Contingent Repayment Plan (ICR) — You’ll pay either 20% of your discretionary income or the amount you’d pay on a 12-year fixed payment term (adjusted according to your income), whichever is less. The loan term is 25 years.

It’s important to remember that by giving you more time to repay your loan, IDR plans can also lead to paying more interest over the life of the loan.

Private student loans

Borrowers may have different options to repay their student loans, but it depends on the lender. When you apply for a private student loan, you may be able to choose from different repayment terms.

Interest typically accrues as soon as the loan is disbursed, though some lenders allow you to defer payments until after graduation or if you drop below half-time enrollment. A lender may also allow you to make interest-only payments while in school, or pay a fixed amount each month that can go toward both interest and principal while still enrolled in school.

Be sure to learn what repayment terms each lender offers before taking out a private student loan. Credible makes it easy to compare offers from multiple private student loan lenders in minutes.