Americans are underprepared for end-of-life planning, survey finds: Here's how much life insurance you need

While many consumers understand the necessity of life insurance, they're not as prepared for end-of-life planning as they think, according to a new survey. Here's how to determine your life insurance needs. (iStock)

Americans are overconfident and underprepared for an unexpected death in the family, according to a recent USAA survey of more than 2,000 respondents. While the majority (74%) said their loved ones would be financially secure in the event of their death, 40% said their family wouldn't be able to afford basic living expenses for more than a year.

The reason? Less than half (46%) of Americans have life insurance.

Life insurance is a financial safety net for your loved ones in the event of your untimely death. A thorough policy can replace your income and provide enough money to cover funeral costs, debt repayment and future investments, as well as day-to-day living expenses.

USAA recommends having enough life insurance to pay off all of your debt and replace income for at least five years.

"It's important to protect your family today, so that if the unexpected happens, their primary focus can be supporting one another," Carter continued.

Shopping around for life insurance? You can compare life insurance quotes for free on Credible.

HOW MUCH SHOULD LIFE INSURANCE COST? SEE THE BREAKDOWN BY AGE, TERM AND POLICY SIZE

How much life insurance do you need?

No one likes to talk about untimely death — in fact, Americans feel more comfortable talking about politics (68%) than end-of-life planning (62%), the USAA survey found. But it's important to analyze your finances while you're healthy, so you can leave your family with a life insurance payout that can replace your income if you die suddenly.

Life insurance should cover the cost of your funeral and leave your family with enough money to cover living expenses and debt repayment. While a common rule of thumb is to take out a policy size that's 10 to 15 times your annual income, there are some considerations to keep in mind.

WHOLE VS. TERM LIFE INSURANCE: HOW TO DECIDE WHAT'S RIGHT FOR YOU

Questions to ask yourself when choosing a death benefit amount

The amount of life insurance coverage you need depends on several factors. Sit down with your monthly budget and ask yourself these questions about your financial obligations:

- What is your annual income, and how many years of income do you want to replace?

- What additional sources of income do your beneficiaries have?

- How much debt do you have? How much money do you have in savings and investments?

- How much money do your kids need for their education and college tuition?

- Do you have life insurance through work? If so, how much?

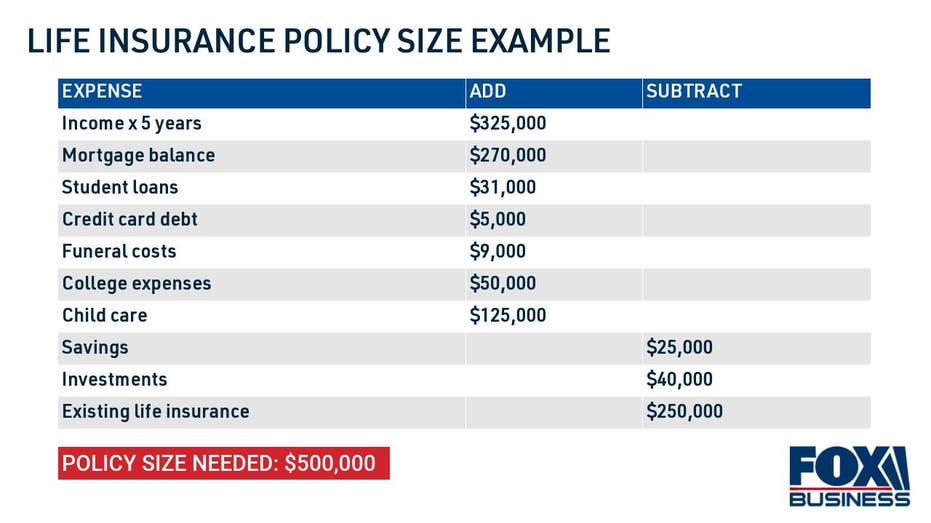

Next, you'll want to calculate your insurance needs by adding your financial obligations (mortgage payment, child care costs, burial expenses, student loans, credit card debt) and subtracting your assets (savings, investments, existing life insurance policies). Here's an example:

Once you've decided on the amount of coverage you need, use a life insurance calculator on Credible to estimate your monthly premium.

AOC AIMS TO EXTEND PANDEMIC UNEMPLOYMENT INSURANCE

What type of life insurance do you need?

In addition to assessing your coverage needs, it's important to compare the different types of life insurance, including term policies and whole life policies. Weigh the pros and cons of each below.

Term life insurance

A term policy is the traditional type of life insurance. You take out a policy that lasts a certain period of time, typically 10 to 30 years. If you die before the term expires, your beneficiaries receive a payout.

- Pros: Affordability

- Cons: No cash value

- Cost: $25 to $50 per month

Term life insurance policies are relatively affordable, especially if you enroll while you're young and healthy. The cost of life insurance rises as you get older and your health deteriorates.

Visit Credible to compare term life insurance quotes across multiple life insurance companies at once.

HOW HURRICANE SEASON CAN IMPACT YOUR HOME & AUTO INSURANCE, ACCORDING TO AN EXPERT

Whole life insurance

Also known as permanent life insurance, whole life insurance is a policy that doesn't expire until you die. It has a guaranteed cash value, and you can access payouts while you're still alive. Whole policies are much more expensive than term policies, but they're seen as an investment due to the resources provided.

- Pros: Guaranteed cash value

- Cons: High cost

- Cost: $300 to $3,000+ per month

You can compare the different types of insurance and find the right insurance company for you on Credible.

WHAT TO KNOW IF YOU LIVE IN ONE OF THESE TOP 10 AUTO THEFT HOTSPOTS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.