Today's Cash-Out Refinance Rates

Cash-out refinance rates vary by borrower and lender, but they may be slightly higher than traditional mortgage loans.

If you’re considering tapping your home’s equity, here’s what you should know about cash-out refinance rates. (Shutterstock)

American homeowners tapped a jaw-dropping $275 billion in home equity with cash-out refinances in 2021, according to mortgage data analysis company Black Knight. The number of cash-out refinances jumped by 20% in 2021, and in the fourth quarter alone, more than 1 million borrowers chose a cash-out refi.

With home values on the rise, it’s no wonder. Home prices were up nearly 19% in 2021, giving homeowners plenty of equity to cash in on, according to S&P data.

If you’re considering tapping your home’s equity, keep reading to learn more about cash-out refinance rates.

Credible makes it easy to see your prequalified refinance rates in minutes.

- Today’s cash-out refinance rates

- Historical cash-out refinance rates

- How Credible mortgage rates are calculated

- What’s a cash-out refinance?

- When to consider a cash-out refinance

- Do cash-out refinances have higher interest rates than standard refinances?

- What’s a good cash-out refinance rate?

- How do cash-out refinance rates compare to home equity loan and HELOC rates?

- How are cash-out refinance rates determined?

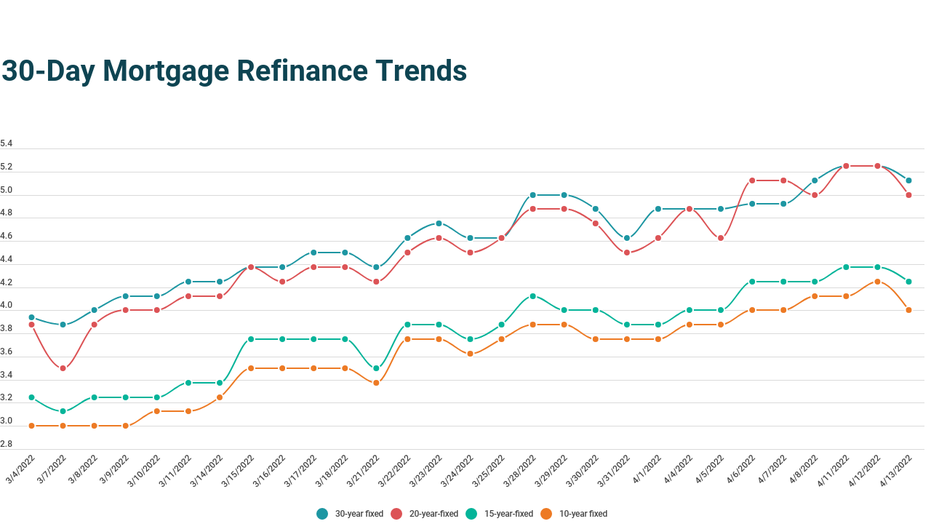

Today’s cash-out refinance rates

Cash-out refinance rates vary by lender, borrower, location, and even by day. Here’s a look at how average rates have trended over the last month.

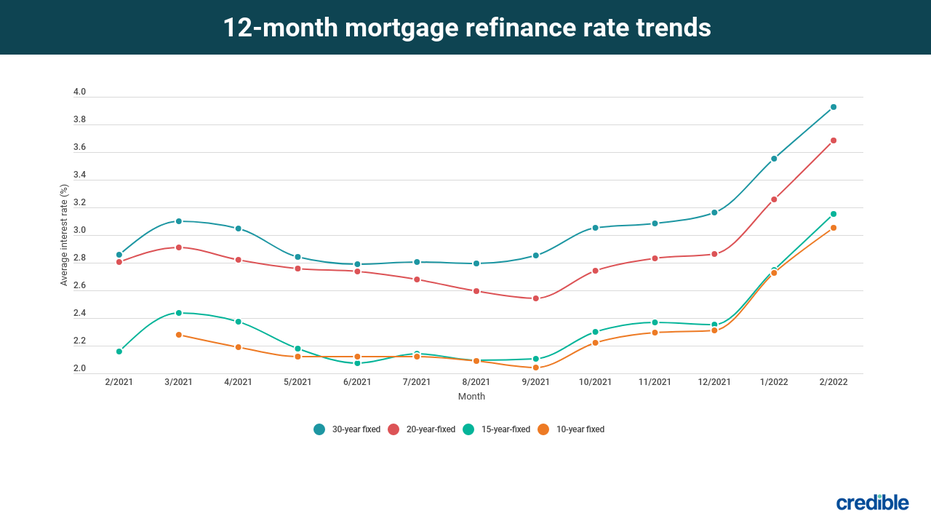

Historical cash-out refinance rates

Interest rates on cash-out refinances have seen their ups and downs over the years. Here’s what rates have looked like over the past 12 months.

How Credible mortgage rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment, and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional home loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

You can compare mortgage refinance rates from multiple lenders using Credible, and it won’t affect your credit score.

What’s a cash-out refinance?

A cash-out refinance is a type of refinance mortgage that replaces your existing mortgage loan with a new loan, while also allowing you to cash in on your home equity.

It works like this: You take out a new mortgage loan for a higher amount than your current one — provided you have enough equity. Your lender will pay off the balance for the old mortgage, and you’ll get the difference back in cash.

You can put that money toward home improvements, medical bills, college tuition, debts, or any other use. There’s no limit to how you can use your funds from a cash-out refinance.

When to consider a cash-out refinance

Cash-out refinances typically make sense if you have a good amount of equity in your home, you’re facing a large expense, and you’d otherwise need to take out a high-interest loan or rack up costly credit card debt to cover it.

This is because mortgage loans generally have much lower interest rates than other financial products. For example, Federal Reserve data shows that the average credit card APR was 14.51% in November 2021. Around that same time, the average rate on 30-year mortgage loans — the most common type of mortgage — was just 3%, according to Freddie Mac. This means homeowners facing big expenses could save significantly by using a cash-out mortgage refinance versus a traditional consumer credit card.

Cash-out refinancing can also be a good idea if you can lower your interest rate. If you took out your current mortgage in 2018, for example, you might have an interest rate nearing 5%. Getting a cash-out refinance loan in 2021 would’ve allowed you to lower your rate and take out cash in the process. If you’re refinancing to lower your interest rate, you typically want to see at least a 0.5% to 1% difference to make refinancing worth it.

Do cash-out refinances have higher interest rates than standard refinances?

Cash-out refinances may have lower rates than most financial products, but they’re usually slightly higher than traditional mortgage rates.

This is because cash-out refinances are considered higher-risk loans. To tap your equity, you have to take out a higher loan amount than what you currently owe. And the more you borrow, the more cash the lender has on the line if you default on your mortgage. Lenders make up for this extra risk by charging slightly higher interest rates.

What’s a good cash-out refinance rate?

In many cases, a good cash-out refinance rate is one that’s one percentage point lower than your current one or more. An interest rate that’s 0.50% to 0.75% lower may also be good, as long as you plan to be in the home long enough to break even on your refinancing costs (meaning the rate reduction saves you more than the closing costs and fees to refinance).

If you’re facing an unavoidable expense and would have to use a higher-interest product like a credit card or personal loan, any cash-out refinance rate is likely to be beneficial. The average interest rate for a 24-month personal loan was around 9% as of November 2021, according to the Federal Reserve. These loans also have shorter terms, so you’d have higher monthly payments and would need to repay the balance sooner.

In all scenarios, the cash-out refinance rate you’re offered will depend on your credit score, loan-to-value ratio, or LTV (how much of your home’s value you’re borrowing against), and the lender you choose. It’s critical to shop around and compare several refinance lenders before applying for a cash-out refinance.

How do cash-out refinance rates compare to home equity loan and HELOC rates?

Cash-out refinance rates are generally lower than home equity loan rates and home equity line of credit (HELOC) rates. But it’s important to note that you usually can’t make an apples-to-apples comparison when considering these three options.

For one, most HELOCs come with variable interest rates, so while you may get a low rate upfront, that rate won’t be consistent while you have the HELOC. Home equity loans and cash-out refinances, on the other hand, typically have fixed rates, giving you a reliable rate and payment for your entire loan term.

Additionally, HELOCs and home equity loans are types of second mortgages, so they come with an added monthly payment on top of your existing mortgage payment. This could mean extra financial strain on your budget.

If you’re considering refinancing or taking out a home equity loan or HELOC, you can always ask your loan officer to break down the exact rate, payment, and costs of each option based on your home’s value, your credit score, the loan amount you need, and other factors. They can then advise you on what’s best for your budget and unique goals as a homeowner.

If you’re ready to do a cash-out refinance, Credible makes it easy to compare mortgage refi rates from various lenders in minutes.

How are cash-out refinance rates determined?

Mortgage rates — including those on cash-out refinances — are heavily influenced by market conditions, the overall economy, and monetary policy from the Federal Reserve. When the economy is struggling, rates are generally lower, and when the economy is booming, rates are higher.

Rates vary by individual borrower, too. The following factors can all affect the cash-out refinance rate you receive:

- Credit score

- Debt-to-income ratio

- Loan-to-value ratio

- Location

- Lender

Keep in mind that closing costs also vary on cash-out refinances, so make sure to get several quotes and compare each one’s rates, fees, and other line items before deciding which lender to go with.