Bankruptcy filings continue to decline despite skyrocketing credit balances

Filing a bankruptcy petition is just one way to get out of debt

Fewer Americans are leaning on bankruptcy court to sort out their financial affairs, according to U.S. Courts. Here's when it may be worthwhile to file Chapter 7 or Chapter 13 bankruptcy. (iStock)

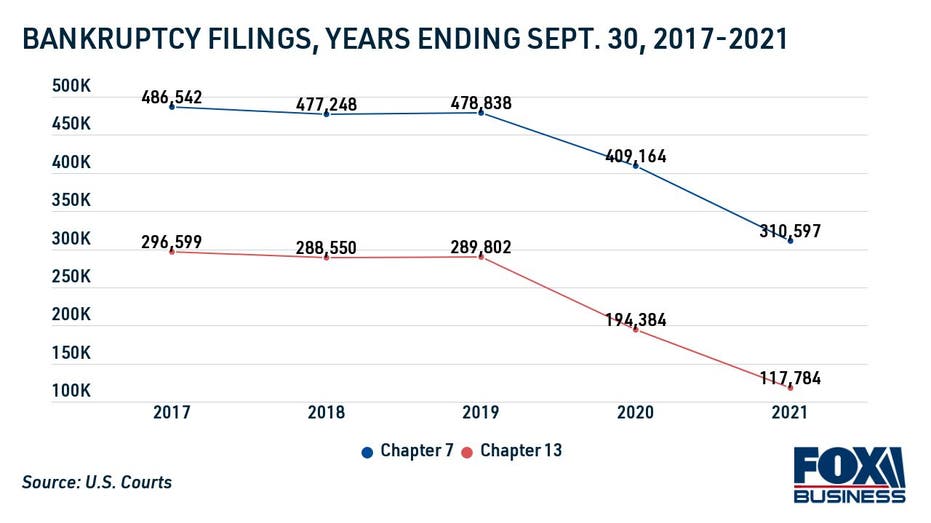

Bankruptcy filings declined when the coronavirus pandemic began in March 2020 as revolving credit balances sharply dwindled. Although revolving credit balances have abruptly risen in 2021, bankruptcy filings have continued to steadily fall.

Personal bankruptcy filings fell 29.1% for the year ending Sept. 30, according to the Administrative Office of the U.S. Courts. The annual Chapter 7 and Chapter 13 bankruptcy filings totaled 418,400 in 2021, compared with 590,170 in 2020.

HOW TO REBUILD YOUR CREDIT AFTER A BANKRUPTCY CASE

There are several reasons why bankruptcy filings have fallen since the pandemic began. For one, consumers have been carrying less revolving credit card debt during this time. Increased government benefits like stimulus checks, foreclosure moratoriums and eviction bans may have also "eased financial pressures in many households," according to the U.S. Courts report.

But recent data from the Federal Reserve shows that revolving credit balances have risen 7.7% nationwide in 2021 alone, which means that some consumers may be considering filing for bankruptcy to discharge unsecured debts like credit cards and personal loans.

Keep reading to learn how to decide if you should file for bankruptcy, as well as your alternative debt repayment options like debt consolidation loans. If you decide to borrow a personal loan to pay off debt, visit Credible to compare interest rates across multiple lenders.

MEDICAL BILLS ARE THE LEADING CAUSE OF BANKRUPTCY, DATA SHOWS

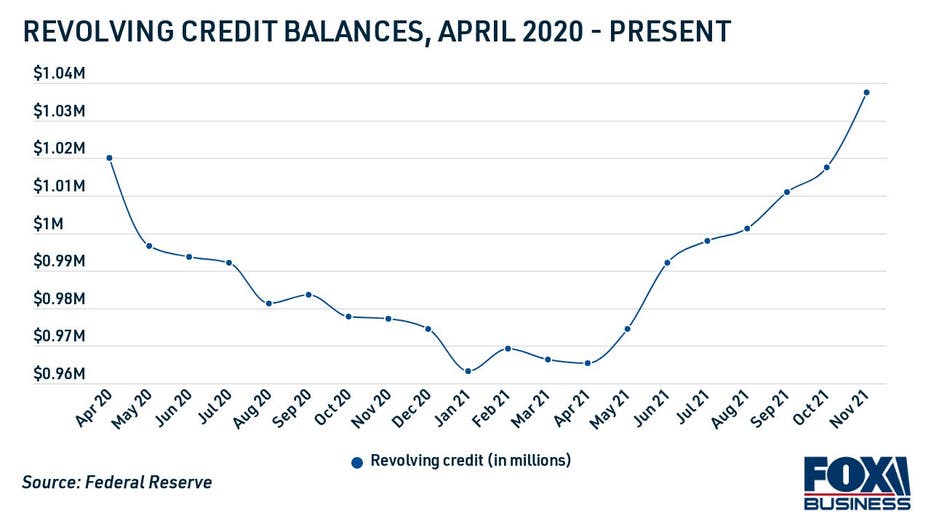

Rising credit balances haven't yet spurred bankruptcy demand

Outstanding revolving credit balances dramatically declined at the beginning of the pandemic, according to the Fed, as Americans aggressively paid down credit card debt and avoided taking out new loans. But as the nation's economy hums back to life and unemployment rates recover to pre-pandemic levels, consumers are returning to their old borrowing habits.

Revolving credit balances have grown nearly every month of 2021, rising from $961.5 billion in January to $1.04 trillion in November. This suggests that consumers are carrying higher balances on their credit cards, car loans and personal loans.

HOW YOUR TAX REFUND CAN IMPROVE YOUR CREDIT

For consumers who are struggling to repay their debts, bankruptcy can provide much-needed financial relief. But there are other debt repayment options, like credit counseling, debt management plans and debt consolidation loans, which is why it's important for debtors to know their options.

If you're considering borrowing a personal loan for debt consolidation, visit Credible to view your estimated terms for free without impacting your credit score. This can help you decide if this option is right for you.

WHAT IS A STUDENT LOAN INCOME-DRIVEN REPAYMENT PLAN?

How to decide if you should file for bankruptcy

Bankruptcy is a legal proceeding that's meant to help consumers regain control of their finances. There are two types of bankruptcy for individuals: Chapter 7, which is known as a liquidation bankruptcy, and Chapter 13, also known as a reorganization bankruptcy.

Filing for bankruptcy may help you repay your debts on more favorable terms and reduce the amount of debt you owe. But it comes with serious penalties, including a long-lasting blemish on your credit report. Plus, the bankruptcy process is a public court proceeding that typically requires the services of a bankruptcy lawyer. Because of these consequences, bankruptcy is often seen as a last resort.

Despite its drawbacks, there are circumstances when filing for bankruptcy is worthwhile, according to The National Foundation for Credit Counseling (NFCC). Here are a few reasons to declare bankruptcy:

- Your outstanding debts are larger than your net worth and assets

- Your income isn't sufficient to meet your financial obligations

- Creditors are suing you over your debts, resulting in wage garnishment

- You're considering borrowing money to pay for bills and necessary expenses

- Your home is in danger of foreclosure

Any of the situations above may be reason enough to file for bankruptcy, but you should also consider your alternative debt management options. You may be able to recover your financial situation without resorting to bankruptcy. Visit Credible to get in touch with a knowledgeable loan officer who can help you navigate your debt consolidation options.

BIDEN ADMINISTRATION RECONSIDERING STANCE ON FEDERAL STUDENT LOANS IN BANKRUPTCY

Alternatives to filing for bankruptcy

Bankruptcy can provide a fresh start for consumers who are struggling to manage their debts, but it's not the only way to get out of debt. Consider your alternative debt repayment methods:

- Negotiate with your creditors. If you're struggling to make mortgage payments, call your loan servicer to discuss your options like mortgage forbearance or a loan modification. If you owe money to the IRS, enroll in a payment plan or settle for less than you owe with an offer in compromise (OIC).

- Enroll in credit counseling. A nonprofit credit counselor can teach you how to cope with your debts through financial education. A credit counseling agency may also help you enroll in a debt management plan (DMP) and negotiate with your creditors on your behalf.

- Consolidate credit card debt. It may be possible to get a lower rate on your credit card debt through a balance transfer or debt consolidation loan. You'll need good credit to qualify for the best offers on balance-transfer credit cards and personal loans for debt consolidation.

You can visit Credible to compare offers on balance-transfer cards and debt consolidation loans for free with a soft credit inquiry, so you can see if this debt management strategy is right for you.

HOW TO PICK A BANKRUPTCY ATTORNEY

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.