10-Year Fixed Refinance Rates

Refinancing to a 10-year fixed mortgage can save you a significant amount of money over the life of your loan.

When you first took out your mortgage, the payments on a 10-year fixed-rate loan might have been too high for your budget. But if you’ve paid down enough of the balance on your current mortgage, refinancing into a 10-year term could help you pay off your home faster and realize significant interest savings.

In fact, in the second quarter of 2021, 30% of borrowers shortened their loan term when refinancing, according to Freddie Mac. Here’s what to know about 10-year refinance rates.

Credible makes it easy to see your prequalified refinance rates in minutes.

- Today’s 10-year mortgage refinance rate trends

- Historical mortgage rates

- How Credible mortgage refinance rates are calculated

- Pros of a 10-year mortgage refinance

- Cons of a 10-year mortgage refinance

- When is the right time to refinance?

- How to get your lowest mortgage refinance rate

- What is the average cost of a refinance?

- What credit score do you need to get a good 10-year refinance rate?

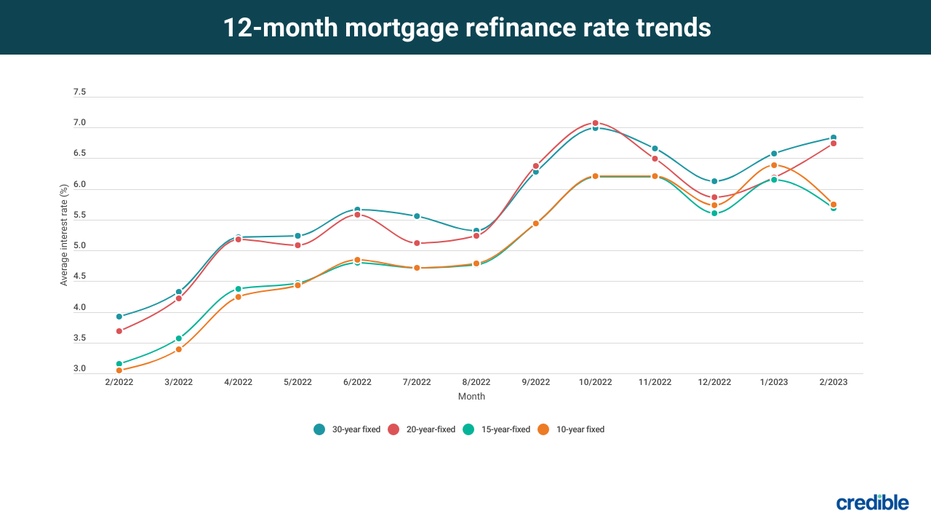

Today’s 10-year mortgage refinance rate trends

Here’s how mortgage refinance rates have been trending over the past 12 months.

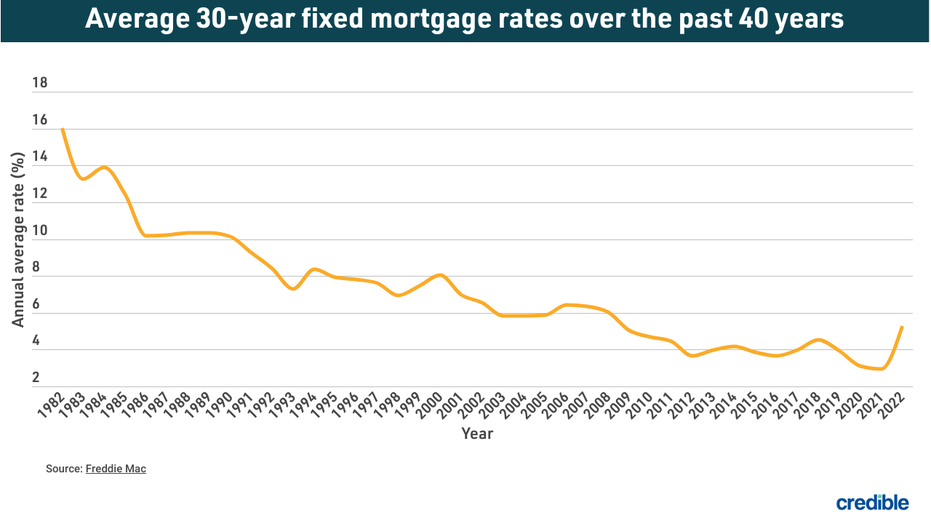

Historical mortgage rates

Here’s what the annual average mortgage interest rate has looked like for the past 39 years.

How Credible mortgage refinance rates are calculated

Changing economic conditions, central bank policy decisions, investor sentiment, and other factors influence the movement of mortgage rates. Credible average mortgage rates and mortgage refinance rates are calculated based on information provided by partner lenders who pay compensation to Credible.

The rates assume a borrower has a 740 credit score and is borrowing a conventional loan for a single-family home that will be their primary residence. The rates also assume no (or very low) discount points and a down payment of 20%.

Credible mortgage rates will only give you an idea of current average rates. The rate you receive can vary based on a number of factors.

Credible makes it easy to compare rates from multiple lenders in just minutes.

Pros of a 10-year mortgage refinance

Refinancing into a 10-year mortgage comes with several advantages:

- A lower interest rate — Current mortgage refinance rates are relatively low, and chances are they’re lower than your current mortgage rate. Ten-year rates also tend to be the lowest available, so refinancing your mature mortgage could mean you get a significantly lower interest rate.

- Quicker loan payoff — By refinancing to a 10-year mortgage, you could cut down the time it takes to own your home free and clear. Mortgage debt is often the biggest expense for a household, so eliminating that debt will make a big difference in your budget.

- Potential overall savings — By paying off your mortgage loan sooner, you could save a substantial amount of money by eliminating the interest that accompanies your mortgage payment. For example, if you take out a 30-year mortgage at 4% interest to buy a $250,000 home, you’ll pay $179,674 in interest over the life of the loan. But let’s say you’ve paid your balance down a bit to $240,000 and you refinance into a 10-year loan at 3% interest. The total interest on that 10-year refinance is just $38,095 — a savings of more than $140,000.

- Ability to get cash back — When you refinance a mortgage, you can get a cash-out refinance to tap the equity in your house. You can use the cash to make repairs or improvements that will add value to your home.

Cons of a 10-year mortgage refinance

You’ll also want to consider some possible drawbacks of refinancing into a 10-year mortgage:

- Higher monthly payments — Shorter mortgage terms typically come with higher monthly payments. In the scenario outlined above, refinancing your 30-year mortgage into a 10-year loan would push your monthly mortgage payments from $1,194 to $2,317. When you shorten your loan’s term, your monthly mortgage payment will probably go up.

- Closing costs — When you refinance a loan, you usually pay closing costs, which can be a few thousand dollars. You might be able to roll those costs into the loan.

- Might not be worth the effort — You first need to calculate what your potential savings would be if you refinance to a 10-year mortgage. Unless you’ll benefit financially, it might not be worth the expense and trouble to refinance.

- Reduced home equity — If you opt for a cash-out refinance, any cash you take out means you lose that much equity in your home.

When is the right time to refinance?

Many factors determine whether it’s the right time for you to refinance your mortgage. Generally, though, refinancing may be a good move if you can get a new mortgage interest rate that’s at least 0.75% less than your current mortgage rate.

Refinancing may also be a good idea if you've got an adjustable-rate mortgage that’s about to reset. While ARMs can start out with a very low interest rate, when the rate resets your interest costs can soar. Refinancing into a fixed-rate mortgage could be a way to protect yourself against future rate increases.

How to get your lowest mortgage refinance rate

Some factors that affect the refinance rate you’ll get are out of your control. But you can take several steps to ensure you secure the best refinance rate available to you. Here are some to consider:

Save for closing costs

In addition to saving for a down payment, it’s also a good idea to save up for closing costs, which can average $5,000, according to Freddie Mac.

Polish your credit

Just as when you bought your home, your credit score and history affect your refinance rate, so it’s a good idea to make sure your credit is in the best possible shape.

Check your credit report for any errors, such as incorrect information or duplicated accounts. Pay off as much other debt as you can to improve your debt-to-income ratio, and pay down credit card balances to reduce your credit utilization.

Comparison shop

Just as you’d compare quotes from multiple vendors for an expensive home repair, you should look at loans and mortgage interest rates from multiple lenders. In fact, getting five rate quotes could save you $3,000 over the life of your mortgage, according to a Freddie Mac survey.

What is the average cost of a refinance?

You’ll generally encounter costs when refinancing your mortgage — $5,000 on average, according to Freddie Mac.

Your exact refinancing costs will depend on multiple factors, including the size of your loan and where you live. Typical refinancing costs include:

- The cost of recording your new mortgage

- Appraisal fees

- Attorney fees

- Lender fees, such as origination or underwriting

- Title service fees

- Credit report fees

- Mortgage points

- Prepaid interest charges

Keep in mind there’s no such thing as a truly no-cost refinance. Lenders who market "no-cost loans" typically charge a higher interest rate and roll the costs into the loan — which means you’ll pay more interest over the life of the loan.

What credit score do you need to get a good 10-year refinance rate?

Your FICO score is one measure your mortgage lender uses in determining whether it will grant you a loan, and if so, what your interest rate will be. Note that it often pays to shop lenders to get the most competitive rates. FICO scores are broken down this way:

- 800-plus — Your score is considered exceptional, and you should qualify for the best available interest rates.

- 740 to 799 — If your score falls in this credit band, you have very good credit and will likely qualify for better rates.

- 670 to 739 — Your credit score is considered good. You should be able to qualify for a loan, but you might not get the best rate.

- 580 to 669 — With credit that’s just considered fair, you might have difficulty getting approved for a loan, and if you do secure a mortgage, you can expect to pay a higher interest rate.

- 579 and lower — Your score is far below the average credit score. Lenders may view you as a risky borrower and it may be very difficult to qualify for a loan.

Checking your prequalified rates on Credible doesn’t affect your credit score.