7 ways to retire with $1 million

How can you retire with $1 million in assets? It's easy … if you start with $3 million! All kidding aside, the best answer is to make a plan that achieves the savings necessary to get to $1 million.

We can help you formulate that plan using the following seven tips.

1. Make Saving and Budgeting a Priority

You can't even begin to save $1 million if you can't save anything on a monthly basis.

Saving is a mindset, and a budget is the way to turn that mindset into tangible results. Start by laying out a reasonable budget, looking for ways to cut expenses.

Your budget is the building block to get a monthly surplus – and you can't even begin to save $1 million if you can't save anything on a monthly basis.

2. Start Early

Start today. (iStock)

Whatever you choose to do, do it right away. Start saving well before retirement and you can take full advantage of compounding interest.

By adding regular deposits to your accounts and reinvesting your retirement plan earnings in the market, you can increase your savings by many thousands of dollars. Online calculators are available to help you see the effects over time – and maybe give you the incentive you need to stick to your plan.

3. Take Advantage of Retirement Plans

April Lewis-Parks, director of education and public relations for Consolidated Credit, puts it succinctly: "Start a retirement fund as soon as possible."

If your employer offers a 401(k) plan, take full advantage of it – especially if your employer offers matching funds. At the very least, you should contribute up to the matching limit set by your company. If you fail to do so, you are literally turning down free money.

If a 401(k) is not available to you, establish an IRA instead. Roth IRAs use post-tax dollars, while traditional IRAs use pre-tax dollars and allow you to defer taxes until the funds are withdrawn at retirement. The key is to put your funds in a growth vehicle that isn't easy for you to raid. On that note...

4. Don't Draw on Your Retirement Funds

(iStock)

It's tempting to borrow against your retirement funds or cash them out to deal with more immediate fiscal hardships, but it's almost always a bad idea to do so. In addition to the effect of taxes and fees, you will lose the positive effect of compounding on the withdrawn funds.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

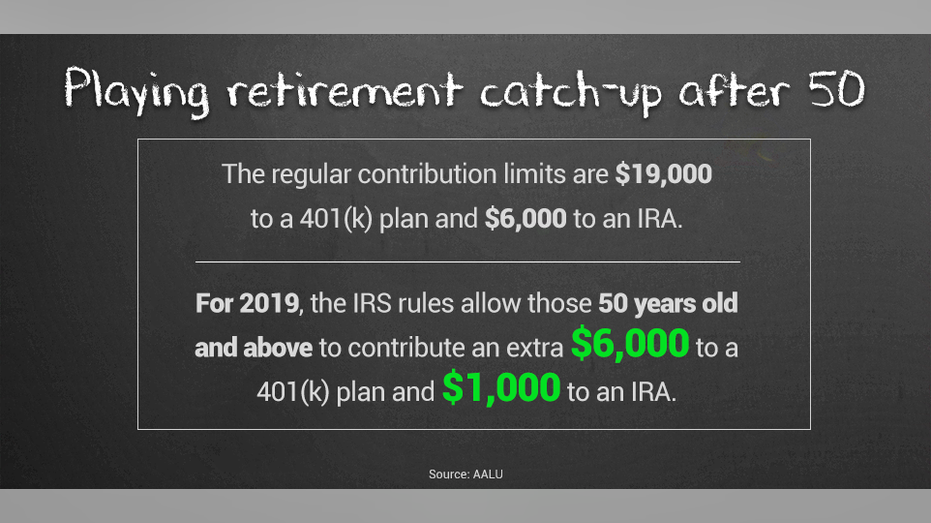

5. Take Advantage of IRS Catch-Up Rules

When you turn 50, you can take advantage of the IRS catch-up rules, designed to help those who are behind in their savings track. Fortunately, you can also take advantage of those same rules when you're ahead.

For 2019, the IRS rules allow those 50 years old and above to contribute an extra $6,000 to a 401(k) plan and $1,000 to an IRA. The regular contribution limits are $19,000 to a 401(k) plan and $6,000 to an IRA.

6. Keep Debt Low

It's difficult to save money when you are carrying excessive debt – especially high-interest credit card debt. Try to keep debts manageable and value-based, such as mortgage debt that builds valuable equity.

Using your credit card for purchases is perfectly fine, as long as you avoid interest by only charging what you can afford to pay in full at the end of the month.

7. Automate Deductions

Even if it's just $10 a week, that's something.

Set up automatic deductions to emergency funds or other accounts that you don't regularly access. It doesn't have to be much – as Lewis-Parks notes, "Even if it's just $10 a week, that's something... have it become a habit and keep doing it week after week, month after month, year after year."

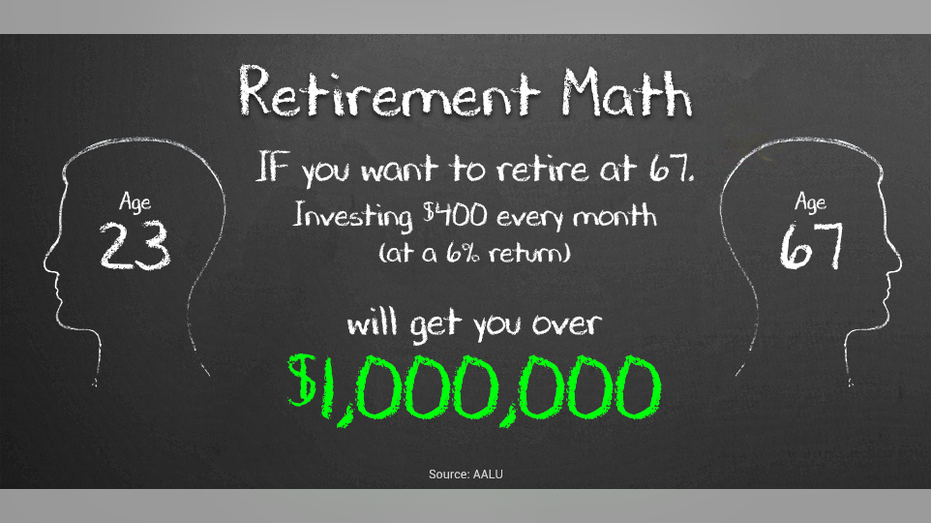

Let's say you're 23 and want to retire at 67. Investing $400 per month, every month, at a 6% return, will get you over the million-dollar mark.

The point is to establish savings reservoirs that you don't consider as being available for regular spending and contribute to them on a regular basis.

Armed with these tips and a determination to succeed, you can increase your chances to reach a $1 million nest egg at retirement – or maybe even $3 million. You can then enjoy the fruits of your labor with a secure retirement.