You Avoided Under Armour: Here's Why National Beverage Is the Next Bubble Stock to Avoid

They say you should invest in what you know. While this is a fantastic way to start looking for companies to invest in, it should only serve as a starting point.

Business history is replete with examples of companies that had fantastic products and always left customers satisfied, but nevertheless saw their shares fall by huge percentages at various times. More often than not, these large losses, which sometimes prove transient, are the product of huge gains.

Image source: Getty Images.

Historically, investors have relentlessly bid up shares because the product is just that great. But as the old Buffett-ism goes: Price is what you pay, value is what you get.

Take Under Armour (NYSE: UAA), for example. Shares reached a sky-high $50 per share in Fall 2015 -- assigning the company an earnings multiple of 91 times that year's earning per share (EPS) of $0.55. Today, shares change hands for about $20 -- a 60% drop. The reason for this staggering drop is simple: expectations came back to Earth and the bubble popped. Under Armour's future is probably still bright -- even the best of businesses can be a terrible investment if the price paid is too high.

Avoiding such situations is just as important to successful investing as picking winners, and just such a situation is bubbling up again -- this time, in shares of National Beverage (NASDAQ: FIZZ).

Recent results

National Beverage is the maker of one of the most popular beverages on retail shelves today: LaCroix flavored sparkling water. A major beneficiary of the declining interest in caffeinated sodas from the likes of companies like Coca-Cola, National Beverage's product sales have exploded in recent years.

For the quarter ended January 28, 2017, which were reported on March 9, 2017, net sales came in at $195 million, a 20% increase over the same period a year ago, and net income more than doubled, rocketing up from $11.2 million, to $24.3 million.

Results for the nine-month period ending on the same day were just as exceptional: revenues were up 17% and net income came in at just under $78 million, a solid jump from the $43.7 million in profits generated in the nine months ended Jan. 30, 2016.

These are solid results, and they build upon a history of success.

A solid record, but is it enough?

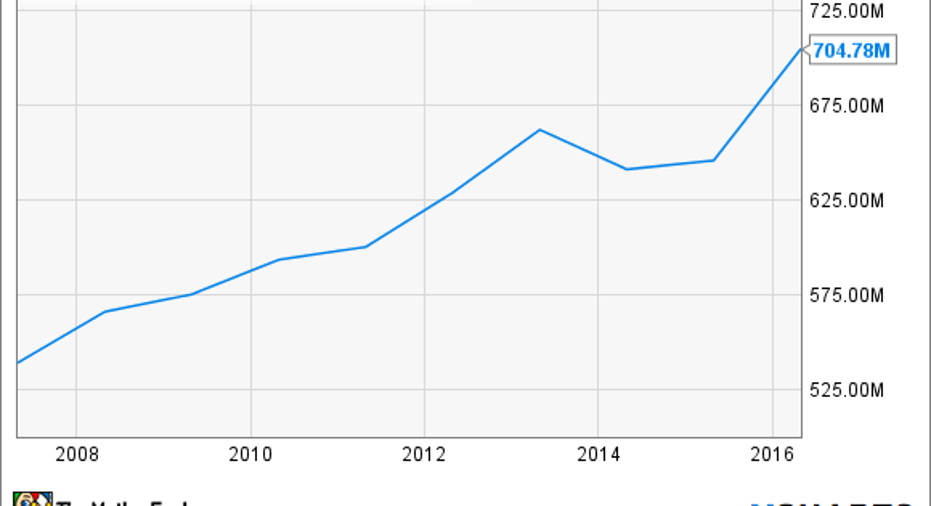

National Beverage's latest quarter, one for the record books by basically every measure, is less surprising when looking at the company's historic results:

FIZZ Revenue (Annual) data by YCharts.

National Beverages sales, led by leading brands LaCroix and Faygo, have been on a steady march upward for years -- exactly what an owner wants to see. Not only that, but the company has been smart with how it makes use of this success: as evidenced by its extraordinarily high return on equity in recent years:

FIZZ Return on Equity (TTM) data by YCharts.

An operating history like that of National Beverage is enough to catch the attention of any astute investor. Unfortunately, it's here that the company's attractiveness as an investment arguably ends.

Sparkling beverages and a bubbling valuation

There's no disputing that National Beverage has a runway of growth ahead of it and a record of solid profitability behind it. The problem with investing in the company, at present, is the valuation that Wall Street is currently assigning to its shares:

Source: S&P Global Market Intelligence.

With the bull market now entering its eighth year, and the S&P 500 Index sporting a trailing P/E ratio of 25, it would not be unreasonable to question the merits of paying such a high price for National Beverage. Growth is also beginning to slow, as evidenced by FY 2018's estimated earnings.

Foolish final thoughts

National Beverages' shares probably make a poor investment at their current price, but that does not mean the business itself is in trouble. Far from it. A high valuation implies that the market believes, to the point of irrationality, that the company in question's future is extremely bright.

National Beverage's products certainly belong on grocery store shelves (who doesn't enjoy a refreshing glass of Berry LaCroix?),but investors should think twice before adding its shares to their investment portfolios.

10 stocks we like better than National BeverageWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and National Beverage wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Sean O'Reilly has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Under Armour (A Shares). The Motley Fool has a disclosure policy.