Will 2016 Be SunPower Corporation's Best Year Yet?

Image source: SunPower.

SunPower Corporation has been in something of a holding pattern for most of the last two years. It's been building a 350 MW annual production expansion and holding projects on its balance sheet in anticipation of launching a yieldco, both of which have reduced profits. And slowly, the company has been buying or developing capabilities to compete as energy management and energy storage become more prevalent.

These developments have made SunPower look like a slow growth company on the surface, but they're fundamentally changing its underlying strength. And the growth picture could change starting in 2016.

The growth engine heats up I mentioned that a 350 MW capacity expansion is going to start adding to growth, but that's just the beginning of SunPower's growth plans. The company bought Cogenra Solar in 2015 and will use its technology to build low-cost solar panels for use in emerging markets.

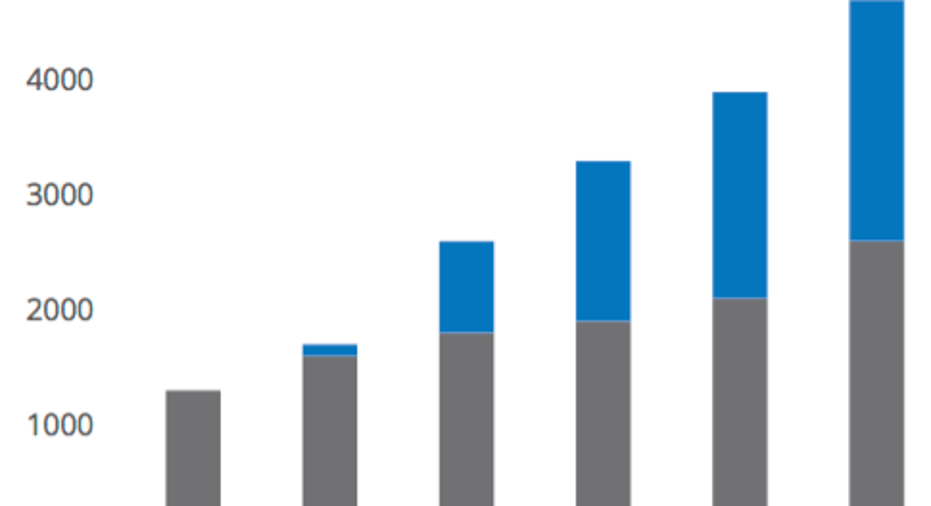

SunPower's expected production growth thru 2020. Image source: SunPower.

These markets have largely been off limits for SunPower because its systems have higher upfront costs than competitors, which are made up for with greater energy generation long term. But in high cost of capital environments, the higher revenue in out years couldn't overcome higher upfront costs for investors.

You can see that between 2015 and 2020, SunPower will more than triple production based on current plans, and I wouldn't be surprised to see more capacity expansion announced in 2016. The U.S. solar investment tax credit extension has created an environment for high growth domestically, and SunPower may look to expand to take advantage given more policy certainty.

The yieldco kicks into high gear 2015 also saw the launch of the yieldco 8point3 Energy Partners, but 2016 is when it will start paying dividends.

SunPower and First Solar agreed to forego dividends early in the yieldco's life as the projects it bought were being completed. That way, public investors could get their expected dividend from cash available for distribution. That will likely end sometime in mid-2016, when there will be enough cash flow to pay both sponsors based on their ownership percentage. For SunPower, the payout from its 40.7% ownership stake of the company will be about $30 million annually based on the $74 million in predicted cash available for distribution in 2016.

Plus, if the yieldco recovers at all in 2016, it'll be able to sell shares to fund more acquisition, which benefits SunPower from the initial dropdown as well as the ongoing dividend.

A tide that lifts all boats SunPower has a lot going for it in 2016, and with industry-leading technology and margins, I think this will indeed be a great year. Look out for the booming U.S. solar market providing upside as well, whether it's in the form of higher margins for solar panels, or more commercial customers deciding that now is the time to go solar.

Watch for production growth during the year and, potentially, a further expansion of capacity. Now that the industry has some certainty in the U.S., and international markets seem keen on growing their solar footprints, it's time for SunPower to put the pedal to the metal on growth. If that happens, the stock could be one of the best energy stocks of 2016.

The article Will 2016 Be SunPower Corporation's Best Year Yet? originally appeared on Fool.com.

Travis Hoium owns shares of 8point3 Energy Partners LP, First Solar, and SunPower. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.