Why You Should (and Shouldn't) Buy Barrick Gold Corporation Stock

Image source: Getty Images.

Physical gold has had a phenomenal year. After a multiyear downtrend, the lustrous yellow metal is up by more than $260 an ounce year to date, and spot gold logged its best performance during the first quarter since 1986. Without question, some of the biggest benefactors of this march higher in gold prices have been the mining companies themselves.

One of those beneficiaries is large-cap miner Barrick Gold (NYSE: ABX), which is up a brisk 148% year to date. Gains of this magnitude are bound to turn investors' heads. But the big question is whether Barrick Gold has the momentum to continue heading higher or whether this move has been fool's gold all along.

To answer this, we've enlisted the help of two of our Fool contributors. Not surprisingly, they each have a markedly different view on where Barrick Gold could be headed next. Here's what they had to say.

The case in favor of buying Barrick Gold

Sean Williams: Gold stocks haven't had an easy go of things since 2011, but theoutlook for the industry and Barrick have made a 180-degree turn. Now, even after a substantial rally from its lows in 2016, I'd suggest Barrick Gold could make for a solid long-term buy.

Image source: Getty Images.

There are fundamental and psychological factors fueling spot gold's ascent that I anticipate will continue. For example, there is the traditional uncertainty present that sparks buying interest in gold. Britain's exit from the European Union, who will be the 45th president of the United States, and China's slowing GDP growth are all unknowns that send anxiety-driveninvestors flocking to gold. Physical demand for gold is also on the rise, with central banks and investors gobbling up the precious metal.

However, the biggest underlying catalyst for gold is low global yields. Everything revolves around opportunity cost, which is the idea of giving up guaranteed gains in one asset for possible larger gains in another. Right now, global yields in the U.S., Japan, U.K., and Britain are all at or near record lows. This means that while nominal gains from bonds are possible, investors in fixed-income assets like government bonds are probably going to lose real money to inflation. This makes buying gold in a low-interest rate environment the logical choice. The higher gold prices go, the more miners like Barrick Gold will benefit.

Beyond just rising gold prices, Barrick Gold has fundamental factors that make it attractive. Leading the pack is its sector-leading low all-in sustaining costs (AISC). When I examined the largest gold miners in May, not one was projected to deliver a lower AISC in fiscal year 2016 than Barrick. This is a result of Barrick throwing its capital at only its top-tier projects. Based on Barrick's second-quarter report, full-year capital expenditures are only expected to total $1.25 billion to $1.4 billion, which is actually down from the first quarter by $100 million on the low end of the range and $150 million on the high end. The midpoint of its 2016 capex is just half of what it had been on track to spend only four years prior. Looking ahead, Barrick Gold's AISC in 2016 is down to just $770 an ounce at the midpoint, which would yield well over $500 an ounce in margin based on gold's current spot price.

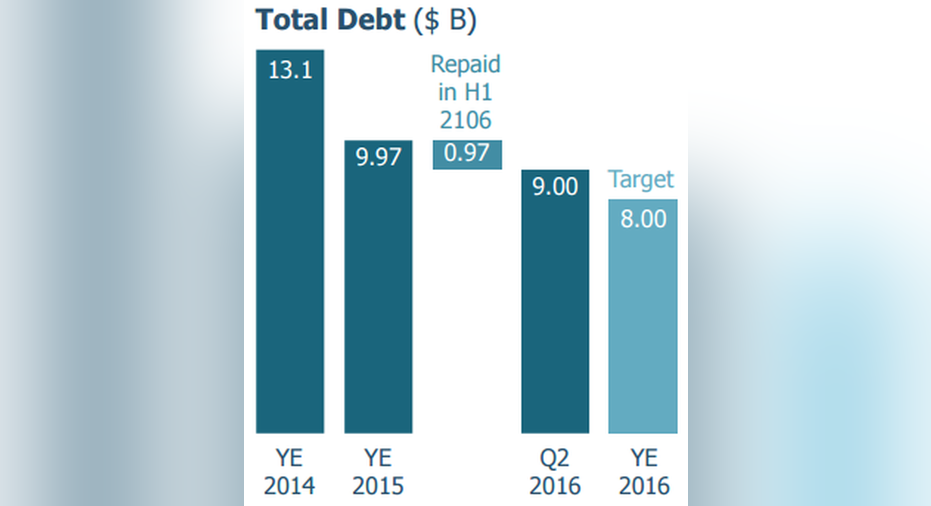

Image source: Barrick Gold.

Barrick Gold has also made incredible progress in getting the biggest monkey off its back: debt. At the end of 2014, Barrick had more than $13 billion in debt, which constrained its ability to maneuver and invest in new projects. After reducing its debt by more than $3.1 billion in 2015, following the sale of non-core assets, the company is on track to pay off another $2 billion this year. Through two quarters, Barrick has reduced debt by $968 million in 2016. The company remains firmly on track to hit its intermediate goal of $5 billion or less in debt by 2018 or 2019, which with lower net interest payments could help push its AISC under $700 an ounce.

What we have with Barrick is a company with falling AISC, reduced and now manageable debt levels, and a product that it mines seemingly poised to increase in value in a low-yield environment. That, to me, is a recipe to buy.

The case against buying Barrick Gold

Neha Chamaria: There's no denying that Barrick Gold is one of the strongest gold miners today, thanks to its aggressive efforts to reduce AISC and deleverage its balance sheet, as Sean pointed out. That said, investing in Barrick has its fair share of risks, and you may be better off avoiding it for several reasons.

Image source: Getty Images.

First things first: No one can predict where gold prices are headed, and even the slightest fluctuation can cause gut-wrenching movements in Barrick's stock. Barrick lost a whopping 17% in just one week as of this writing, as gold cooled off in anticipation of a Fed rate hike in near months. Meanwhile, surging gold prices sent demand from the world's top two gold-consuming nations, India and China, lower by 14% and 18%, respectively, during the second quarter.

The point I'm trying to drive home is that there are too many unpredictable variables that drive gold prices, and the yellow metal could reverse its gains just as quickly if the unknowns don't play out as anticipated. While that could send Barrick shares tumbling, it's also worth knowing how sensitive Barrick's earnings are to gold prices: For every $100 per-ounce increase or decrease in gold prices, Barrick's earnings before interest, taxes, depreciation, and amortization (EBITDA) could increase or decrease by roughly $536 million. That's a huge risk to pay for when you realize that Barrick incurred EBITDA losses worth $710 millionin 2015. Not to mention that Barrick hasn't turned a profit since 2011.

Image source: Barrick Gold.

I'm also a tad concerned about Barrick's declining gold production rates, as it's guiding for 4.6 million to 5.1 million ounces of gold for 2018. That's an 18% to 26% decline from its 2014 production levels. Lower volumes -- a price Barrick is paying for its moves to alleviate debt through the sale of non-core assets -- could prove a setback if demand for gold continues to rise.

Barrick is weighing options to develop Pascua-Lama -- a high-potential Chilean project it mothballed after running into legal hassles that led to cost overruns of billions of dollars. However, it's an uphill task, as the risky project could require significant capital expenditures to get started, which would put tremendous pressure on Barrick's cash flows. Meanwhile, the gold miner continues to burn a hole in its pocket by spending millions of dollars annually on maintaining Pascua-Lama.

I could delve deeper into the several other risks associated with Barrick, but I'll stop here and give my verdict: You can find better options than investing in a stock that has more than tripled in one year despite the company making losses and lacking clarity as to when it'll turn profitable given the highly unpredictable nature of its business.

What's your take on Barrick Gold: Is it time to buy or keep your distance?

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Neha ChamariaandSean Williams have no position in any stocks mentioned.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.