Why We're Excited About These 5 Top Stocks

Image source: Getty Images.

It's pretty exciting when you find a stock idea you can really get behind. We reached out to some of our top Motley Fool contributors to ask them what stocks have them jumping for joy right now. They came back with an eclectic list of intriguing stocks that includes Transdigm (NYSE: TDG), Wal-Mart Stores (NYSE: WMT), Exelixis (NASDAQ: EXEL),Align Technology (NASDAQ: ALGN), and Terra Nitrogen Company(NYSE: TNH). Are these stocks right for your portfolio? Read on to find out.

This stock will continue flying high

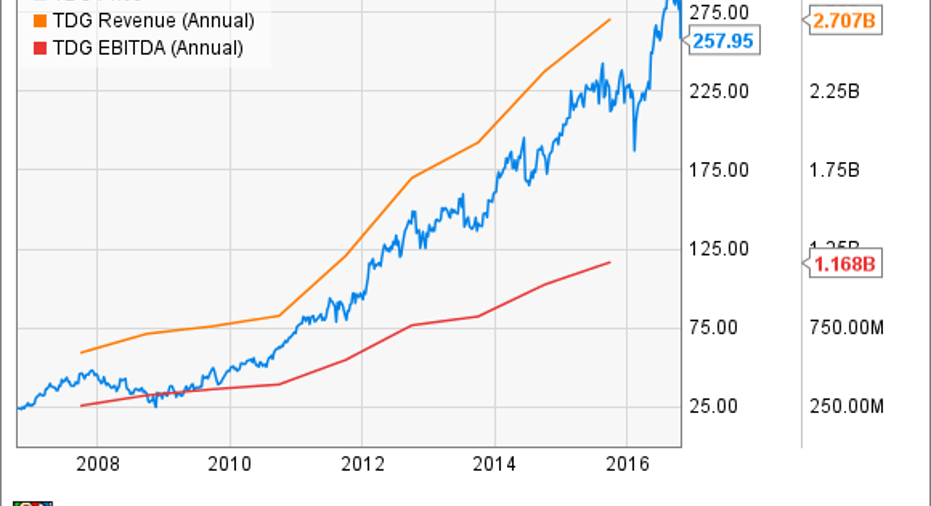

Daniel Miller: One stock I'm excited about is found within the aerospace industry, but it's not the juggernaut manufacturers you'd likely think of (like Boeing or Airbus). Rather, TransDigmis a leading designer, producer, and supplier of engineered aircraft components and systems that are used on just about every commercial and military aircraft in service. The company IPO'd roughly a decade ago and hasn't looked back.

The good news for long-term investors is that the aerospace industry isn't slowing down, either. In fact, Boeing estimates that more than 39,000 commercial airplanes -- we're not even considering military aircraft, here -- will be needed over the next two decades thanks to a surge in Asia demand. Those airplanes are valued at more than $5.9 trillion, and TransDigm's business should carve out its fair share of that pie.

TransDigm also possesses competitive advantages that should last for the long term. It has intellectual property on its products that are produced according to strict FAA certifications. Further, for those unaware of the process, once FAA certifies an aircraft design, it also certifies the bill of materials, which would include TransDigm's parts. That essentially creates switching costs for aerospace manufacturers that are less likely to make changes in the design for years.

Ultimately, TransDigm's business has soared along with a booming aerospace industry, but part of the reason its growth has been such on a blistering pace is its acquisition-heavy strategy and leveraged balance sheet. That makes TransDigm risky, but if it continues to do business as well as it has historically, the company is poised to reward long-term investors.

No more messing around

Tim Green: The retail industry is going to look a lot different 10 years from now. E-commerce will continue to steal away sales from traditional retailers, and the weakest operators will struggle to survive. Wal-Mart, the 800-pound gorilla of the brick-and-mortar retail business, aims to not only survive, but thrive. The company is going all-in on e-commerce, and while this will hurt its results in the near term, it's the only path forward.

Wal-Mart is scaling back its plans to open new stores, with just 55 U.S. stores planned for fiscal 2018, down from 230 in fiscal 2016. At the same time, the company is rapidly growing its stable of e-commerce distribution centers and investing in new technology to make its warehouses more efficient. According to Justen Traweek, VP of e-commerce supply chain and fulfillment, Wal-Mart can now ship to the majority of the U.S. population in one day.

The $3 billion acquisition of Jet gives another boost to Wal-Mart's e-commerce business, while at the same time giving the company a brand that may prove more appealing to younger consumers. Other initiatives, like ShippingPass, a $49 annual subscription service that provides free two-day shipping and online grocery pickup and delivery, show that Wal-Mart isn't going sit idly by and let Amazon eat its lunch. Wal-Mart may have fallen behind in e-commerce, but that doesn't mean it can't catch up.

Image source: Getty Images.

Sales of this newly approved drug look ready to explode higher

Sean Williams: Call me a bit biased since I've been a shareholder for more than two years, but I'm really excited to see what happens next with biotech Exelixis.

There have been two major dynamics at work with Exelixis: the rise of Cabometyx and the recent struggles of one of its biggest competitors.

Cabometyx is Exelixis' lead cancer drug. It was approved by the Food and Drug Administration in April as a treatment for second-line renal cell carcinoma after it delivered the first-ever "trifecta," as management has called it: Cabometyx led to statistically significant improvements in progression-free survival, median overall survival, and overall response rates relative to the placebo. It was a big win for Exelixis after Cabometyx flopped in an advanced prostate cancer study.

Here's where things get interesting. Recently, Exelixis announced mid-stage data from the CABOSUN trial, noting that Cabometyx proved to be superior with respect to progression-free survival to the current standard of care, Sutent, in first-line renal cell carcinoma. It's possible a label expansion opportunity could be on the horizon.

Exelixis is also benefiting from the suggestion of the independent data monitoring committee (IDMC) in the CELESTIAL trial, which is examining Cabometyx as a treatment for advanced liver cancer. The IDMC suggested the phase 3 trial continue as planned, which implies that Cabometyx has a shot of hitting its primary endpoint of a statistically significant improvement in median overall survival. Top-line data should be out next year.

Finally, Bristol-Myers Squibb's Opdivo, a cancer immunotherapy that can seemingly do no wrong, is reeling after Opdivo failed to even come close to hitting its primary endpoint in a first-line non-small cell lung cancer study known as CheckMate-026. The failure of Opdivo, which is the current market share leader in second-line renal cell carcinoma, could open the door for Cabometyx to capitalize in the second-line (and perhaps, down the road,first-line) for this indication.

Things are really starting to heat up for Exelixis, and shareholders should rightly be excited.

The reason is clear

Todd Campbell: Align Technology, Inc.is one of healthcare's fastest-growing companies, and demand for its Invisalign clear orthodontic aligners is showing no signs of slowing.

In Q2, Align Technology's year-over-year sales and profit increased by 29% to $269 million and 59% to $0.62 per share, respectively.

ALGN Revenue (TTM) data by YCharts.

Invisalign's growth stems from compelling advantages versus traditional metal braces. Since Invisalign is clear, it's less noticeable to others. The aligners can be removed easily, and there aren't any restrictions on the types of food you can eat while wearing Invisalign. Invisalign can be cheaper than traditional metal braces, too.

Currently, Invisalign's market share is only 7%, and since next-generation Invisaligns are being designed for use in tougher-to-treat patients, the peak sales opportunity appears big -- especially if Align Technology successfully extends its reach beyond orthodontists to general dentistry.

Based on the company's anticipated revenue growth, Align Technology's C-suite thinks bottom-line growth will clock in north of 23% per year over the next five years, so even though shares are up significantly, I think there's still plenty of upside ahead.

A strong player in a tough market

Tyler Crowe:Just about every publicly traded commodity is struggling today, even ones we assumed would be very stable markets, like agriculture products and fertilizers. The thing is, the agricultural market is suffering from the same malaise as everyone else: too much capacity brought on to satiate the rapid growth of the Chinese economy with little regard to the possibility that this market would slow down. One product in particular has been hit hard: nitrogen-based fertilizers such as urea. Despite the 10-year decline in prices, Terra Nitrogen Company still looks like a compelling investment.

What separates Terra Nitrogen from the rest is that it is out in front of a major shift in the industry. Its urea and ammonium nitrate manufacturing capacity uses cheap domestic natural gas versus more expensive means, such as the anthracite coal used across much of the Asia Pacific region. So, despite the very low prices for urea today, Terra Nitrogen still has gross margins in the 55%-60% range over the past 12 months. Add in the fact that the company has a very lean operation and no debt and you get a company that throws off loads of cash it can distribute to investors -- it is a master limited partnership -- and generates a whopping 45% return on capital.

Any potential investor needs to keep in mind that Terra Nitrogen is a variable-rate master limited partnership, so its payout varies from quarter to quarter based on commodity prices and any maintenance downtime. When you consider that the company can do so well even in a distressed commodity market like today, there's a lot of reasons to think Terra Nitrogen will succeed over the long term.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Daniel Miller has no position in any stocks mentioned. Sean Williams owns shares of Exelixis. Timothy Green has no position in any stocks mentioned. Todd Campbell has no position in any stocks mentioned. Tyler Crowe owns shares of Terra Nitrogen. The Motley Fool owns shares of and recommends Amazon.com, Exelixis, and TransDigm Group. The Motley Fool recommends Align Technology. Try any of our Foolish newsletter services free for 30 days.

We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.