Why Intrexon Won't Commercialize Fuels by 2018

Image source: Mike Mozart via Flickr.

A few years ago, a former executive at engineered biology conglomerate Intrexon told me that one of the company's internal guiding principles was simply "to avoid all of the mistakes made by Amyris." Amyris was a pioneering industrial biotech that went from darling of the field to a company now trading well below $1 per share thanks to a lack of market focus, a suffocating debt load, and management hubris. It's likely on its way to bankruptcy or a much worse fate: becoming a zombie company that's impossible to resurrect yet refuses to die. It also serves as a textbook case of the first-mover disadvantage -- and Intrexon is not the only company learning from missteps at Amyris.

Intrexon has delivered on the internal mission to date. The company has generated more revenue in the past 12 months than Amyris has made in renewable product sales in its lifetime. Intrexon monetizes R&D, spreads risks across numerous potential opportunities in unrelated markets, and acquires businesses that it hopes to scale and grow, while internal projects are commercialized in the background. Investors are willing to accept growing losses (for now) because the revenue growth has been spectacular (so far).

Despite the vast performance improvements in the early days of operationscompared to the field's pioneers, Intrexon is following them over one particularly devastating cliff by failing to learn the dangers of overpromising on manufacturing milestones. While investors have been told to expect the natural gas-to-fuels platform to be commercialized by 2018, real-world indicators essentially guarantee that won't be the case -- and hint that it won't even be close.

Here's why investors should adjust their expectations.

Mission impossible

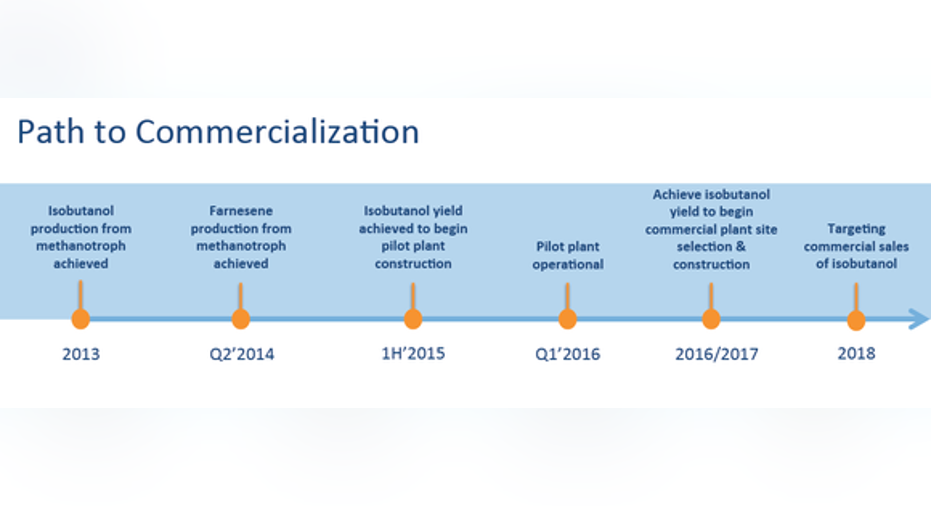

The first red flag for investors is the timeline presented by Intrexon, which itself is enough to ensure the deadlines won't be met. The company is developing an industrial biotech platform that feeds methane to engineered microbes that churn out a renewable fuel blendstock called isobutanol, which boasts significant advantages over ethanol. In 2013, it announced it had successfully produced isobutanol from a methane-chomping microbe. On the second-to-last day of the first quarter of 2016, Intrexon announced it had opened a pilot plant -- utilizing a single 500-liter bioreactor -- in South San Francisco.

Image source: Intrexon.

From there, the path to commercialization is a little hazy, but it could be summarized as follows:

- Openpilot facility.

- ?

- Commercial sales a little over two years later.

That shouldn't instill much confidence in investors. Look at it this way: Intrexon says it will go from proof of concept to commercial sales in as little as six years, or from pilot operations to commercial sales in as little as 33 months.

The ambitious timeline is further complicated by the limited throughput of the pilot facility, which will significantly complicate the direct transition to larger scales.Investors cannot be reminded enough that biology is difficult to scale, or thatcommodity chemicals and fuels require a fantastically optimized process to be economical. The fact that Intrexon has no prior manufacturing experience for the novel process its developing adds another layer of difficulty.Amyris, TerraVia, and others have had at least 10 years to commercialize fuels from more traditional and better-understood technology platforms. None has been perfect, but over 120 months later, none has developed an economical commercial process for fuels. Some have moved on completely.

Other gas fermentation companies have been diligently collecting data from real-world facilities over the course of many years to improve their processes before even considering commercial-scale operations. LanzaTech, which feeds carbon monoxide to engineered microbes that churn out ethanol, began pilot-scale operations (from a much larger pilot-scale facility) with a feedstock partner in 2008. In summer 2015, the company announced it would build a facility capable of producing 14 million gallons per year by 2018.

Around the same time, Intrexon announced a partnership with Dominion Resources to supply natural gas and eventually build commercial-scale facilities. Intrexon has told investors that small, commercial-scale facilities will have an annual capacity of 3.5 billion cubic feet of natural gas, which, assuming half of theoretical yield is achieved, will produce roughly 8 million gallons of isobutanol annually. Larger facilities may have "10x that capacity."

The difference is that LanzaTech will have over 10 years of data from multiple, adequately sized pilot plants across the globe to support process development decisions. Intrexon will have no prior experience with its platform outside of laboratory conditions.

Regulations and thermodynamics

In recent months, I've discussed other major obstacles that the commercialization of Intrexon's natural gas-to-fuels platform faces. First, there are major regulatory obstacles that are unlikely to be resolved by 2018. The company's fuel likely won't qualify for subsidies under the Renewable Fuel Standard because the ultimate feedstock is a fossil fuel. That puts a significant amount of pressure on a never-before-attempted process to reach optimal performance in a record amount of time. It also makes it difficult to dethrone ethanol, which has strict regulations supporting its continued use. Refiners have no incentive to use isobutanol and may not even be physically able to do so after blending required amounts of ethanol into the nation's gasoline supply. Regardless of whether or not the laws make sense, that's the reality.

Second, Intrexon'sprocess faces what may amount to insurmountable technical hurdles. Investors can thank thermodynamics. Essentially, it's very difficult to cram methane into water, which will force the company to use a very inefficient process -- if it works at all. Commercially relevant processes, especially those for low-value commodity chemicals, need titers (concentrations of cultured products) of at least 50 grams per liter to be economical. Intrexon's patent application from early 2014 shows that different combinations of genetic parts resulted in isobutanol titers of 0.001 g/L and 0.22 g/L. The latter requires a 227 times improvement to hit the minimum level of economic relevance. In the two years after the patent was filed, the company has achieved a 44 times improvement.

Making it work profitably at scale by 2018 (or shortly thereafter) doesn't seem like a reasonable expectation for investors at this point.

What does it mean for investors?

I'll be the first to admit I was wrong if Intrexon successfully commercializes fuels by 2018, but given all of the factors at play, it seems impossible. There isn't enough time for the company to scale its process, beat thermodynamics (hint: you can't), or smooth over regulatory issues that usually take the EPA years to resolve. While it's possible to increase production metrics such as titer to required levels given enough time, 33 months is likely not enough time. Investors need to maintain realistic expectations.

The article Why Intrexon Won't Commercialize Fuels by 2018 originally appeared on Fool.com.

Maxx Chatsko has no position in any stocks mentioned. Follow him on Twitter to keep up with developments in the engineered biology field.The Motley Fool recommends Dominion Resources and TerraVia. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.