Why Edwards Lifesciences Could Be About to Soar

IMAGE SOURCE: EDWARDS LIFESCIENCES

The FDA has approved the use ofEdwards Lifesciences (NYSE: EW)Sapien 3 transcatheter heart valve in a key group of heart disease patients. The regulator's green light for the use of the Sapien 3 as an alternative to open heart surgery in patients at intermediate risk could double its use, providing the company with a significant sales and earnings edge over competitor Medtronic (NYSE: MDT)in this growing market. Should you be a buyer of its stock?

The backstory

Aortic stenosis, a narrowing of aortic valves that can lead to heart failure, affects 1.5 million Americans. Currently, most patients are treated via surgical aortic valve replacement, or SAVR, a procedure that involves replacing the narrowed aortic valve with a mechanical valve or a tissue valve.

Although SAVR is still commonly used to treat patients for whom surgery is a low or intermediate risk, high-risk patients are increasingly being treated via a new, less-invasive procedure known as transcatheter aortic valve replacement, or TAVR. TAVR involves inserting a valve within the narrowed valve using a catheter inserted via the femoral artery in the groin or through a small chest incision. Because the procedure doesn't require surgically opening the chest, recovery time and surgical outcomes can be improved, especially in frail patients.

Because of its advantages, adoption of TAVR has been growing -- a boon for both Edwards Lifesciences and Medtronic, the two largest manufacturers of TAVR valves. Edwards Lifesciences manufactures the top-selling Sapien valves, while Medtronic markets the Core Valve.

Moving the needle

Despite TAVR only being used in high-risk patients until now, sales from its transcatheter heart valve therapy (THVT) segment, already account for over half of Edwards Lifesciences revenue. In Q2, global THVT sales grew 48.7% to $418.6 million andU.S. sales were up 71.5% to $246.4 million.

The robust second-quarter performance led management to boost itsTHVT revenue guidance for this year by $100 million. Edwards Lifesciences now expects underlying growth to exceed 30%.

The increasing use of TAVR has Mussallem and his team estimating that companywide full-year sales will be at the high end of its $2.7 billion to $3 billion guidance range, and that EPS will be between between $2.78 and $2.88. Prior to this latest guidance, management was guiding fortop-line sales of between $2.6 billion and $2.85 billion, and bottom-line EPS of between $2.57 and $2.67. For comparison, the company's EPS was $2.29 in 2015.

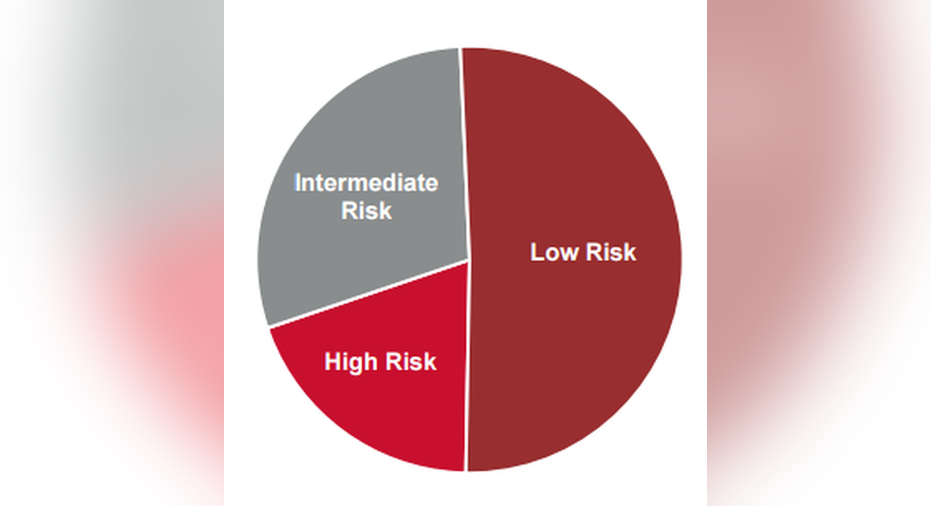

TAVR market distribution. Source: Edwards Lifesciences

Edwards Lifesciences' forecast, however, may be conservative. The high-risk addressable patient population is the smallest of the three segments that could benefit from its Sapien 3 devices and until now, that has slowed TAVR adoption. That impediment is likely to quickly disappear, however, now that the FDA has given the go-ahead for them to be used in intermediate-risk patients. The approval means that the device can now be used in roughly half of all patients requiring treatment for a narrowing heart valve.

The FDA's decision to expand Sapien's label follows resulted from a large late-stage study that compared TAVR with Sapien head-to-head against open heart procedures; Sapien patients did as well or better than those in the control arm of the study.

The rate of all-cause mortality or stroke in Sapien TAVR patients was 19.3%, versus 21.1% for open-heart surgery patients at the two-year mark. Patients receiving the Sapien transfemorally enjoyed even better outcomes, with an event rate of only 16.3%.

According to Medtronic, the TAVR market will be at least a $4 billion market by 2020 and Edwards Lifesciences recently said it could reach $5 billion by 2021. Clearly, the opportunity is big, and approval of its device for intermediate-risk patients positions Edwards Lifesciences nicely to capture its fair share of it.

Time will tell

This label expansion is undeniably a big win, and momentum for TAVR procedures should boost profit given that Edwards Lifesciences margins are better on its TAVR valves than on its traditional surgical valves.

However, Medtronic isn't about to concede this market.Medtronic is studying its Core Valve in the intermediate-risk population too, and results from Medtronic's trial should be available later this year. If Core Valve delivers similarly strong results to Sapien, then Edwards Lifesciences advantage may prove short-lived.

An even bigger battleground, however, may be on tap in 2018. Most heart valve replacement patients are categorized as low-risk patients and if Edwards Lifesciences and Medtronic studies that are under way demonstrate TAVR is equivalent or better than SAVR in that population, then sales could grow even more quickly.

Medtronic's study of Core Valve in low-risk patients began in February and Edwards Lifesciences low-risk patient trial kicked off in the second quarter. Based on those start dates, both companies could have data to digest in 2018. Therefore, while the approval in intermediate-risk patients is a win that should reward Edwards shareholders in the next year, the biggest battle for dominance in this indication has yet to be fought.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Todd Campbell has no position in any stocks mentioned.Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned.Like this article? Follow him onTwitter where he goes by the handle@ebcapitalto see more articles like this.The Motley Fool owns shares of Medtronic. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.