Why Chemours' Great Month (Up 18%) Ain't So Great

Chemours is a chemical company that was spun off from DuPont in 2015. Image source: Getty Images.

On the last day of September, the stock ofDuPont(NYSE: DD) spinoff Chemours (NYSE: CC) hit $16 a share, a high it hadn't seen in more than a year. On the first day of September, it had closed at $13.47 a share for a monthly gain of 18.8%.

And that's just the icing on the cake. Since the beginning of August, the stock has skyrocketed 45%. While those kinds of returns are likely to make investors salivate, they don't tell the whole story.

The spark that lit the flame

Chemours' impressive run began with its better-than-expected Q2 earnings report on Aug. 9. The company reported $0.27 in adjusted EPS, crushing analysts' consensus estimate of $0.17.

Even though Chemours still posted a revenue miss of $40 million, it also reported progress in chipping away at its mountain of debt, paying down $92 million in the second quarter. It had been able to reduce expenses, raise prices on its titanium dioxide products, and grow its Opteon refrigerant business. Free cash flow was positive for a change, and the company maintained its 2016 outlook.

The company hasn't released any major news since its earnings report, so the gains since then appear to be entirely due to this lone quarterly report.

Clawing its way back

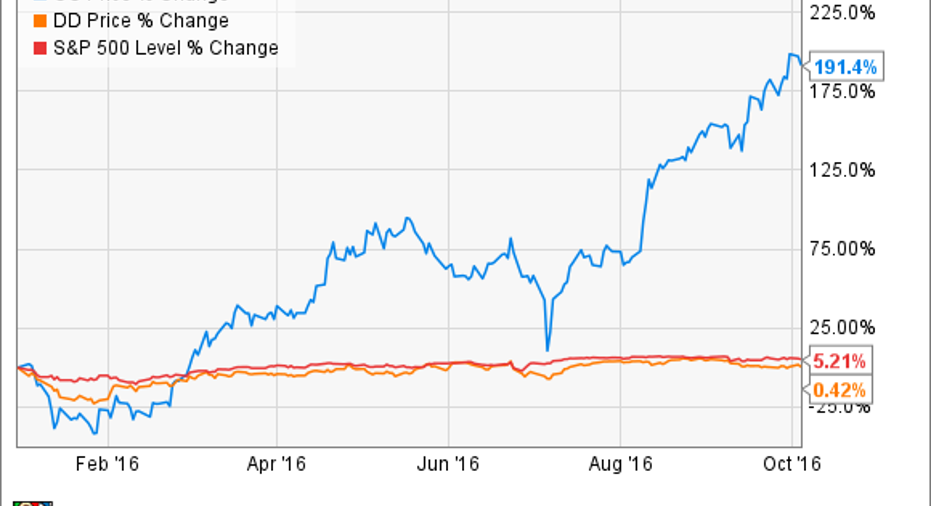

The stock's gains seem impressive, even more so when you consider its year-to-date return vs. those of its former parent DuPont and the S&P 500:

Looks incredible, to be sure. One analyst trumpeted that the stock "has been one of the top-performing stocks not only in the basic materials sector but also in the entire market since being spun out of E. I. du Pont de Nemours and Companylast July."

But that's just not correct. In fact, if you look all the way back to its spinoff, a very different picture emerges:

The stock is still down 25% from its spinoff point, while DuPont and the S&P 500 are ahead (albeit by the hairs of their chinny-chin-chins). So, while investors who timed their entry incredibly well are seeing a tremendous return, everyone who was in from the beginning has lost money on the stock.

The dumping ground

Chemours' long-term underperformance isn't surprising. DuPont loaded up the new company with five times its EBITDA in net debt and numerous environmental cleanup liabilities and lawsuits -- including an estimated 2,400 asbestos-related lawsuits.

Chemours was also forced to indemnify DuPont for damages in any PFOA-related lawsuits, of which there are currently more than 3,500. The few PFOA lawsuits that have already been litigated have resulted in more than $6.7 million in damages against DuPont. DuPont is appealing, but if it's unsuccessful, Chemours may be on the hook for the entire sum.

In exchange for buying into all this uncertainty, investors don't reap much reward. Chemours' dividend yield has been slashed to a paltry 0.77%, compared with 2.27% for DuPont. Profit margins are poor. Further PFOA litigation is looming in November.

Investor takeaway

Clearly, many investors are bullishon Chemours.They may like Chemours' forward P/E, which is much lower than its chemical peers, including DuPont's. The company is also projecting 51% year-over-year earnings growth in 2017.

But even if those rosy projections come to fruition, the company will still have massive amounts of debt to pay off, billions of dollars in possible legal liabilities, and a puny dividend. Chemours is simply too risky to jump into right now.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

John Bromels has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.