Why Callon Petroleum Is Thriving Through This Oil Downturn

While many oil and gas producers in North America are peering into the abyss, Callon Petroleum is doing quite well. In fact, the company just picked up another significant slug of some of the most desirable shale oil land in the world.

What you may not know about Callon is how close the company came to not surviving the last oil crash and just how incredibly different the company looks today versus then.

A near-death experience

During 2008, Callon Petroleum was caught with its pants down at the worst possible time. The company was in the midst of developing a prospective offshore field called Entrada when the world started falling apart.

Everything that could go wrong for Callon did go wrong. First, oil and gas prices plunged as the world went spiraling into an epic recession. Then two hurricanes hit the Gulf of Mexico, causing significant delays for Callon. When you're spending a few hundred thousand dollars a day on a drilling rig, you can't afford to have it sitting idle.

Then, with Callon already hurting, came the near finishing blow. The company discovered that before it could begin producing from Entrada, an expensive side-track well would have to be drilled, since the original had missed its mark.

With cash flows crimped, access to capital shut down because of the financial crisis, and an expiry data looming on the Entrada lease, Callon did the only thing it could do. It walked away from the Entrada project.

After that, Callon walked away from the offshore business entirely and instead turned its attention to a very off-the-radar shale play in the Permian basin. By selling off its offshore assets and acquiring Permian acreage early and inexpensively, Callon turned its story from one of near disaster to one of a company with a new beginning.

The latest acquisition

As we have learned in recent years, the Permian is turning out to be the mother of all shale oil plays. With many hydrocarbon-bearing formations stacked on top of each other, land in the Permian contains an incredible oil and gas treasure.

This land is extremely valuable, and acreage transactions that have taken place even since the price of oil crashed reflect that fact. Land value in the Permian has held up much better than elsewhere.

With the stock market recognizing a high-quality Permian land position, Callon's share price has held up well. That has allowed the company to raise cash when needed and continue adding selectively to its Permian holdings.

Callon's most recent Permian acquisition was announced in April and involved paying $220 million in cash and 9.3 million Callon shares for:

- 14,089 net acres, located mainly in Howard County, Texas.

- 165 net horizontal drilling locations targeting the Wolfcamp A, Lower Spraberry, and Wolfcamp B zones

- 1,931 barrels per day of production (82% oil).

- 4.1 million barrels of proved developed producing reserves (71% oil).

As detailed in the slide below the price paid by Callon is better than previous Howard County-focused Permian transactions. So while acreage values in the Permian are still higher than elsewhere, the timing of this deal well into the oil crash helped Callon with the purchase price. The land was acquired from privately held Big Star Oil and Gas so we can't know for sure the reason for the seller unloading these properties at this time.

Source: Callon corporate presentation.

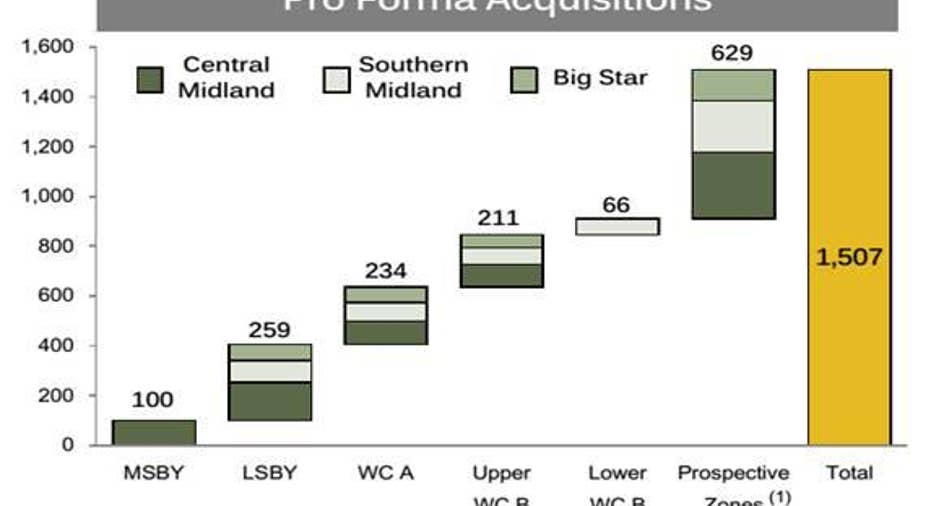

Callon was kind enough to provide us with a pro forma view of the company after this deal closes. What the deal will do is increase Callon's number of drilling locations by nearly 50% to 1,507. That sets the company up for years and years of drilling.

Source: Callon corporate presentation.

To put the size of this drilling inventory into perspective, consider that in 2015 Callon drilled 25 wells. To get through an inventory of 1,500 at that pace would take 60 years.

It isn't coincidence that these Permian players are holding up

If you spend some time perusing the producers that are focused on the Permian, you'll notice that the share prices of these companies have held up very well. Callon's shares are up from where they were on average going into the oil crash. In fact, they are very near the highest point they reached when oil was at $100 per barrel in mid-2014. Shares of Diamondback Energy (NASDAQ: FANG) have also done very well.

This is not a coincidence. Like Callon, Diamondback has a huge land position in the Permian, with almost 2,800 drilling locations. The really cool thing about the Permian is that the drilling location number is likely to increase over time, as the producers figure out how to economically access the multiple layers of shale reservoirs in the Permian zones.

Source: Diamondback Energy corporate presentation.

In Diamondback's presentation, the company shows that the main producing formation, the Lower Spraberry, can earn a 41% rate of return at $40 WTI prices. Anything positive at these oil prices is good.

Source: Diamondback Energy corporate presentation.

A 41% IRR is a little bit higher than what Pioneer Resources presents for its Sprayberry/Wolfcamp wells. At current strip pricing with $45 WTI in 2016 to $50.25 WTI in 2020 Pioneer believes its wells have an IRR of 30% (see Pioneer slide below). If you were wondering, Callon says that its newly acquired acreage also has IRRs of 41% at current strip prices, so all three of these companies are in the same ballpark with their estimates.

Source of image: Pioneer Resources Corporate Presentation

The bottom line

We must always take any numbers in a corporate presentation with a grain of salt, but the actions of companies in this industry that keep chasing Permian acreage speaks volumes. The Permian is the land they most want, and over time it's going to be the biggest oil shale play of them all. It is this Permian focus that hasn't just brought Callon back from the dead but allowed it to outperform during this brutal downturn.

The article Why Callon Petroleum Is Thriving Through This Oil Downturn originally appeared on Fool.com.

TMFWolfpack has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.