What Is the Average Income in the U.S.?

Image source: Flickr user Pictures of Money.

The average American's income is falling, and according to a recent report from Pew Research, the middle class is shrinking. Stagnant income paints a pretty grim picture for retirement savings, but before we get too nervous, let's take a closer look at how you stack up against your peers.

How does your income compare?

Median income across every state in the U.S. is $62,462, but because income varies widely. it may be more useful to see how your income stacks up against others by specific income ranges.

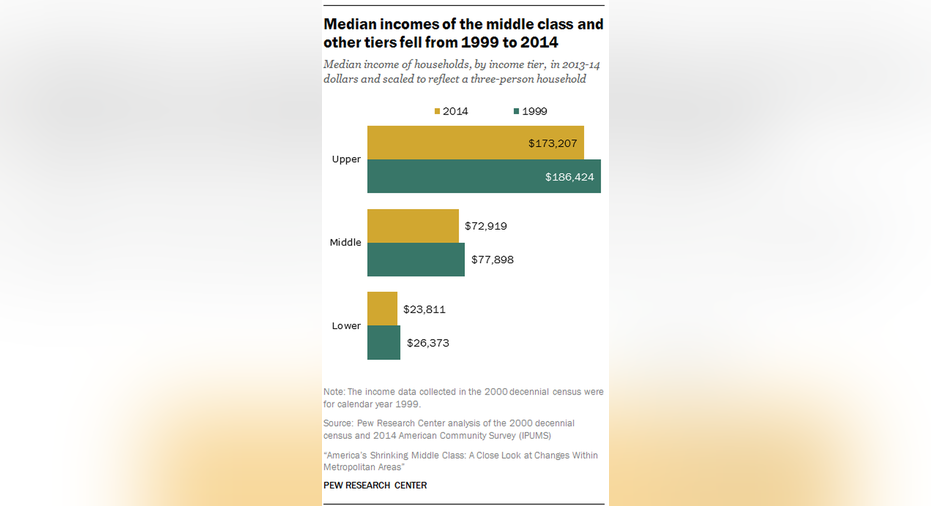

Pew Research calculated income figures for three income groups: lower-income, middle-income, and upper-income earners. Lower-income households earn less than 67% of the median income, middle-income households earn two-thirds to double the national median income, and upper-income households earn more than double the median national income.

Breaking up income into these groups reveals that the median income for lower-income Americans is $23,811 and the median income for middle-income and upper-income Americans is $72,919 and $173,207, respectively.

However, the size of a household can significantly impact how far income stretches so it's also important to take that into consideration. After adjusting for household size, Pew Research determined that a single American earning $24,042 is considered a middle-income earner. However, a household of four members would need an income of $48,083 to be considered middle income.

A big problem

What's worrisome is that Pew Research's findings show that median income across all three income groups has fallen since 1999 in current dollars.

In 1999, the average American's income was 8% higher than it was in 2014, the most recent year for which income data is available. Income has declined 10% for lower-income households, 6% for median-income households, and 7% for upper-income households.

Previously, Pew Research reported that in addition to slipping income, fewer Americans are in the middle class. While the middle class comprised the largest number of Americans in the past, the number of Americans in the middle class now is about equal to the total number of people in lower- and upper-income households.

The combination of income declines and a shrinking middle class is especially worrisome because it suggests that many Americans are struggling to save money for retirement.

According the Federal Reserve, the average American has less than $60,000 savedfor retirement, and according to the Employee Benefit Research Institute's 2016 Retirement Confidence Survey, 31% of Americans haven't put aside a dime for their golden years. That figure is up from 25% in 2009.

Making changes

According to the EBRI survey, American workers are deeply concerned that about their financial future in retirement. Only 28% of survey respondents said that they're very confident about their financial preparedness for retirement.

A lot of that lack of confidence stems from the fact that the majority of Americans haven't calculated the amount of income they're likely to need in retirement and therefore have little to no idea if their savings goals are on track.

Figuring out how much income you're likely to need in retirement is the first step in creating a successful retirement savings plan because that figure allows you to determine how much money you'll need to save every year. Typically, it's recommended that people withdraw no more than 4% of their retirement savings annually as income.

Since the average individual currently receives $16,140 in Social Security income, a person needing $40,000 in retirement income would have to generate $23,860 in additional income from their savings every year. At a 4% withdrawal rate, an individual's total retirement savings would need to be about $600,000. If they've saved less than that amount, then they'd either need to cut their expenses or withdraw a higher percentage of their savings than they might want to in retirement.

If you're shy of your goal, the quickest way to get on track is to make the most of your tax-advantaged retirement plans. In 2016, employees can contribute up to $18,000 to a 401(k) or 403(b) plan, and employees over 50 can contribute an additional $6,000 to catch up. Many Americans also qualify to contribute to an IRA every year. Individuals can contribute $5,500 to an IRA in 2016 and an additional $1,000 can be contributed by people over 50. If you can't max out your contributions to these plans, make sure you consistently increase them every year. That can help you accumulate retirement savings more quickly.

The article What Is the Average Income in the U.S.? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.