what Investors Can Learn from Berkshire Hathaway's Greatest Company

Photo by: GEICO.

Few people understand the extent to which GEICO has been a powerhouse of profitability for Berkshire Hathaway . But Tom Russo certainly does. At a recent event at Alphabet, the fund manager explained why GEICO was worth so much more to Berkshire Hathaway than anyone else.

Russo calls it Berkshire's "capacity to suffer," or its capacity to defer profits today for larger profits in the future. It's a really important concept in finance. Businesses that can suffer low profits today for larger profits in the future can make exceptional investments for patient capitalists.

GEICO was an extraordinary business in the 1990s. By spending more money on marketing, it was finding new customers at a cost of about $250 apiece in the first year. However, those customers would generate profits of $150 per year each year thereafter.

Russo commented that a new customer might be worth as much as $1,500 if all of the future profits from one more customer were discounted back to today.

This is a no-brainer investment, and its why Berkshire Hathaway wanted to own GEICO outright. Buffett knew that any time you can create a $150 annuity for a $250 loss in year one, you should take that deal. Any time you're offered a way to create $1,500 of wealth by reporting a $250 loss today, you should similarly jump at that deal.

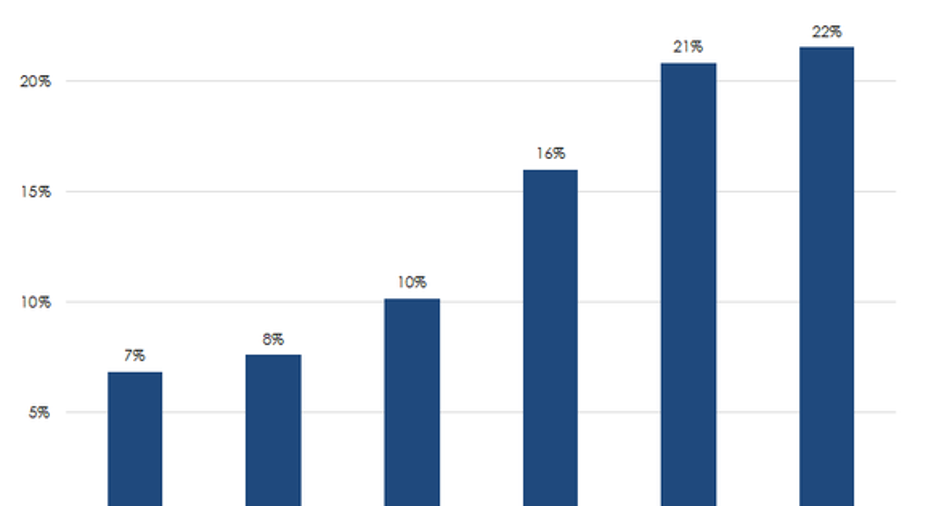

In a clear sign that Berkshire was more than willing to suffer, note that growth in policies in force exploded after it took control of GEICO in 1996, the result of a substantially increased marketing budget.

Simply put, the more money GEICO was willing to lose in the near term, the more it would be worth later. However, it's an unfortunate reality that at publicly traded companies, accounting often encourages managers to avoid growth fueled by operating expenses for fear of weakening earnings in the present.

If a company buys a new piece of machinery to help grow its business, that purchase won't show up in the income statement, at least not all at once. Rather, the cost of the machine will be broken down into bite-sized pieces and digested over time through depreciation expenses. Machinery is depreciated over time because it has a multi-year benefit to a company.

Marketing, however, is expensed immediately on the income statement, despite the fact it provides multi-year benefits to a company, much like a new piece of machinery would.

For companies that have the capacity to delay gratification like Berkshire Hathaway does and did, this business model is fantastic. When a company's investments come in the form of operating expenses, it can compound wealth tax-free by rolling would-be profits into additional expenses for future profits. That's essentially the model that has fueled GEICO's growth for the last 20 years, though it is a very profitable company today despite double-digit growth rates.

Berkshire Hathaway's experience with GEICO is a very good reminder that not all corporate investments are found on the capital expenditures line of a cash flow statement. Sometimes, the best businesses of the future are the companies losing piles of money in the present.

The article what Investors Can Learn from Berkshire Hathaway's Greatest Company originally appeared on Fool.com.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Jordan Wathen has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Alphabet (A shares), Alphabet (C shares), and Berkshire Hathaway (B Shares). Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.