Weatherford International's Management Outlook Is Much Brighter Than Its Third-Quarter Results

This was supposed to be the year that things finally turned around for Weatherford International (NYSE: WFT). The company had started taking the necessary steps of drastically reducing its work force, cutting its debt load, and starting to work toward generating gobs of free cash flow. Unfortunately, this third quarter the company took some major steps back in that regard. But although the results weren't that great, management was surprisingly chipper about the company's future.

Let's take a quick look at the results to see what went wrong, and why management seems much more optimistic than the numbers might indicate.

image source: Getty Images.

By the numbers

All numbers in millions, except per-share data. Data source: Weatherford International earnings release.

One thing to keep in mind with these results is that there are some considerable asset writedowns in that net-income number, so from a continuing operations standpoint, things aren't as bad as they look. For the quarter, management booked $1.43 billion in charges, of which $719 were asset impairments and inventory writedowns and another $683 million in tax valuation allowances. Last year, management had said it didn't foresee any further non-cash charges to the balance sheet, but then again, it also thought that it would generate $650 million in free cash flow this year.

To the company's credit, it has continued to cut costs throughout this down cycle. This quarter the company announced that it had let go 8,000 employees to lower its cost base, as well as shut down five operational facilities. On an annual basis, the head-count reduction should save the company $500 million annually.

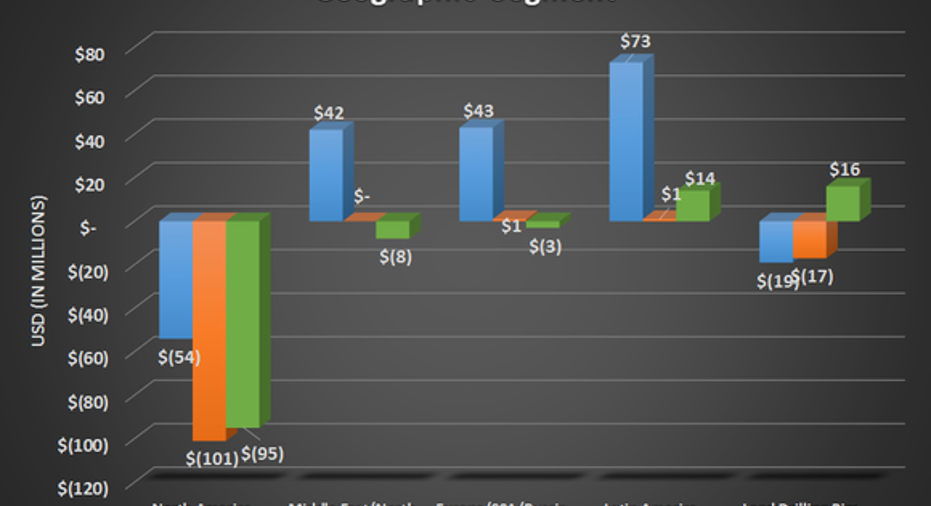

The biggest issue has been that revenue declines have outpaced those gains. Only in North and Latin America did Weatherford's operational efficiencies lead to improved results:

Data source: Weatherford International earnings releases. Chart by author.

The other discouraging point about Weatherford's results is the continued cash burn that is setting the company back yet again. This quarter, operations burned through $106 million, on top of the $41 million in capital investments, net sales and insurance recoveries. For the year, the company has burned through $519 million in cash and has, as a result, needed to tap the debt markets yet again. At the end of the quarter, net debt stood at $7.05 billion -- $1.26 of which is convertible debt that it used to refinance its debt coming due between now and 2018.

What management had to say

Even though the numbers across the board didn't look good for the company, CEO Bernard Duroc-Danner sounded surprisingly optimistic in his earnings release statement. His positive spin on everything came down to the fact that the market is starting to show signs of life that indicate it is recovering:

Duroc-Danner isn't alone in this opinion, but his views do paint a rosier picture than most. Schlumberger's CEO Paal Kibsgaard also noted in his company's press release that he expects activity across the industry to pick up in 2017. But it will be a very muted recovery because the financial statements of producers ranging from the small mom-and-pop operations to the national oil companies in the Middle East look absolutely dismal right now, and companies will need to pay off some debts before going full-bore again.

What a Fool believes

It seems that no matter what Weatherford tries to do to lower its cost structure, the oil and gas market dips even lower. This puts the company so far behind its strategic plan from last year that it had to throw that plan out the window and refinance its debts, rather than pay them down with free cash flow.

Management believes that it is in a great position to capture the benefits of a market rebound and estimates a rapid return to profitability. Based on statements from other oil-services executives, though, that recovery may not be as robust as Weatherford is hoping for. Plus, with so many spending gaps that need to be filled, Weatherford still has a lot of work to do before investors should seriously consider it.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Tyler Crowe has no position in any stocks mentioned.You can follow him at Fool.comor on Twitter@TylerCroweFool.

The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.