Use This Unorthodox but Effective Metric to Value McDonald's Stock

In the first article of this two-part series, we looked to the EV-to-EBITDA ratio to bring clarity when valuing McDonald's Corporation, given its recent debt expansion and intended transformation to a company that will be nearly completely franchised in the future.

As a quick refresher: EV, or "enterprise value," is a company's total market capitalization plus net outstanding debt.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, removes the non-cash items of interest expense, tax effects, and depreciation and amortization from the income statement.The adjustment of earnings by non-cash items in EBITDA approximates a company's cash flow.

Divide EV by EBITDA, and you've formed a ratio of total market value plus debt to operating cash generated. The EV-to-EBITDA multiple is a widely recognized and useful way to compare companies with different capital structures. But there's a better way to understand McDonald's, which is simultaneously leveraging up and transitioning its business model.

The poorly understood but eminently useful "EV to earnings" ratio

Image source: Getty Images.

To value McDonald's, consider using the "EV-to-earnings" ratio, which employs the same calculation of enterprise value, but without any adjustments to earnings.

To some readers, this may seem controversial. Enterprise value is a non-levered measure. Adding net debt to a company's market capitalization pulls out inherent leverage in the shares."Earnings" -- that is, net income presented in conformity with generally accepted accounting principles (GAAP) -- are by contrast a levered measure. Profits are presented after the effect of borrowings (i.e., interest expense).

So combining an unlevered numerator like enterprise value with a levered denominator like earnings drives some financial types crazy: It's not apples to apples.

But let's ignore the protests of those who stride along the high road and hang with the crowd that doesn't mind mixing it up -- for a few moments, anyway.

The SEC requires GAAPearnings -- often referred to as "unadjusted" earnings -- to be presented to shareholders of publicly traded companies for a reason. They're all-inclusive earnings, revealing the effects of the interest a company has to pay on its debt, the depreciation and amortization that eat away at the value of assets on the balance sheet, and the tax expense incurred on income each and every quarter.

Think of positive GAAP earnings as a hurdle:A company at minimum should generate enough profit margin to enable it to pay interest and taxes, while providing for the replacement of fixed assets like equipment on a timely basis. I love this aspect of GAAP earnings; they remove no warts from a company's profit and loss ledger.

Keeping this in mind, when you look at a company's enterprise value in comparison to GAAP earnings, you're asking the following question: What multiple of "all-in" earnings am I paying for the right to total assets plus the obligation of assumed debt?

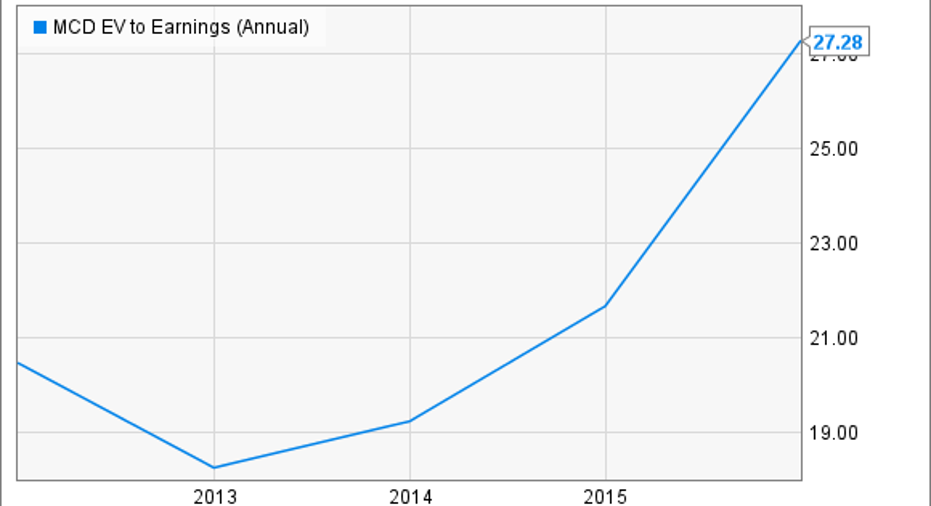

Viewed through this specific lens, we see that McDonald's has become expensive very quickly. Another interpretation is that the company has lost some earnings power relative to its expanding capital base:

MCD EV to Earnings (Annual) data by YCharts.

Ways the EV/earnings ratio will decrease and reflect a more reasonable valuation

What would pull the trend line back down a bit? McDonald's could reduce its enterprise value by using future operating cash flows to pay down debt. Incidentally, this would also decrease interest expense. A smaller enterprise value reduces the overall multiple and would make the company less expensive (or more attractive) to the average stock investor who tracks this metric.

Alas, such a course isn't likely this year. As we discussed in the previous article, McDonald's will borrow more money in 2016 to fulfill a management promise. The additional debt will be used to repurchase shares on the open market. This will have a cancelling or "wash" effect on enterprise value. So unless McDonald's stock begins to decline, the EV/earnings ratio will probably remain high through this year.

The second way the burger chain can work this ratio down is by simply becoming more profitable on an "all in" basis, something that the current management team seems committed to. Moving to a lighter capital expenditure model by franchising more restaurants will reduce depreciation expense. Following through with a general and administrative cost cutting target of $500 million (announced late last year) will also positively affect the bottom line.

When you examine McDonald's through this unorthodox but reasonable metric, one thing is clear: The company is certainly becoming expensive relative to its ability to churn out profits. At the same time, this doesn't have to remain the case. In the previous article, we saw that in comparison to peers, McDonald's isn't terribly overvalued. It's just that when you throw the obligation of debt into the equation, investors are paying a higher enterprise multiple for each dollar of earnings. If you're interested in this quality stock, keep an eye on both debt and earnings and consider averaging into a position over time.

The article Use This Unorthodox but Effective Metric to Value McDonald's Stock originally appeared on Fool.com.

Asit Sharma has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.