This Tax Credit Could Save You Thousands This Year

Source: BIGSTOCK.

We all want to lower our tax bills and get our hands on more money, right? Well, tax credits do just that. If you have low to moderate income, the Earned Income Tax Credit could put thousands of dollars back in your pocket come tax season.

Want to find out how much this credit is worth to you? That depends on your specific circumstances, such as the exact amount you earned in 2015 and the number of qualifying children you have.For the 2014 tax year, an estimated 27.5 million tax filers received an average of $2,400 each thanks to the EITC.And although filling out extra forms is a drag, this one is worth your while if you qualify. Plus, it's easy. All you need to do is file aSchedule EICalong with your tax return.

Tax credits versus tax deductionsFirst, let's get one thing straight: The EITC is a tax credit, not a tax deduction. And there's a big difference between the two.

A deduction reduces your taxable income, so your ultimate tax savings will only be a percentage of the tax deduction. For example, let's say youpaid $5,000 in mortgage interest last year. You can deduct that $5,000 from your taxable income, but the amount of money the deduction actually saves you depends on your tax bracket. If you're in the 15% bracket, you'll save 15% on that $5,000, or $750.

Meanwhile, a taxcreditis a dollar-for-dollar reduction of your tax liability. If it's anonrefundablecredit, it can lower your tax liability to $0, but any leftover credit money is lost. If it's arefundablecredit, then it can not only wipe out your tax bill, but pay you any money left over. Let's say you owe $1,000 in taxes and you're eligible for a $1,500 tax credit. If that credit is nonrefundable, then you and the IRS are even -- nobody pays a dime. If that credit is refundable, however, then Uncle Sam owes you the $500 remainder.

With that out of the way, here's some good news: The EITC is refundable, so if you're eligible for a credit that's bigger than your tax liability, then that extra money goes straight to your wallet.

EITC criteriaNow let's get down to the nitty-gritty of the EITC. First, the bad news: Not everyone is eligible. You can't claim the EITC if your filing status is married filing separately. However, if your status is married filing jointly, head of household, single, or qualifying widow, you may qualify.

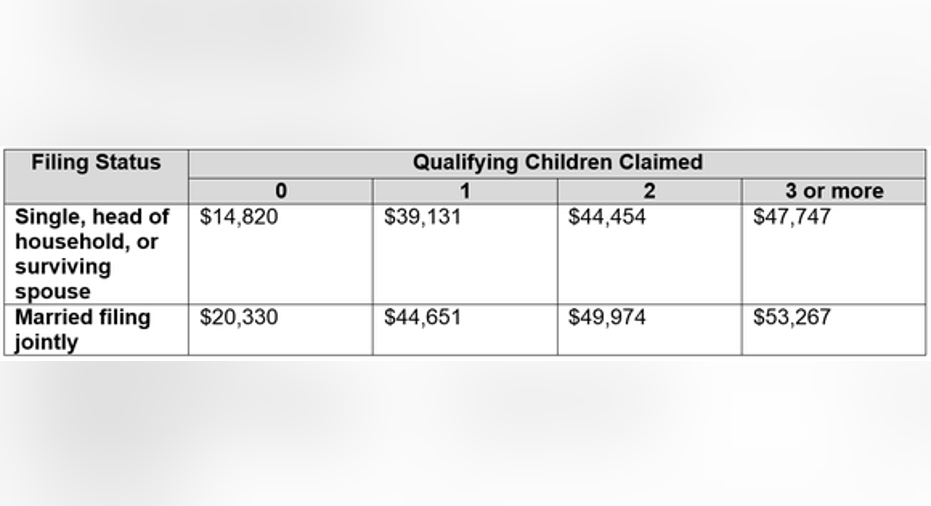

Now let's talk income. To qualify for the EITC, you must have earned at least $1 in 2015 (in which case I hope you didn't spend it all at once). Additionally, your investment income for the year must be $3,400 or less.There are also income caps that vary based on your filing status and the number of qualifying children you claim. In order for you to be eligible, both your earned income (the money you earned from your job) and your adjusted gross income (your gross income minus certain deductions) must both remain below a certain threshold.

Here are the 2015 income thresholds for the EITC:

DATA SOURCE: INTERNAL REVENUE SERVICE.

For the 2016 EITC income caps, see the IRS website.

Show me the moneySo here's what you stand to earn by filling out some extra paperwork. For the 2015 tax year, you could receive up to:

- $6,242 with three or more qualifying children.

- $5,548 with two qualifying children.

- $3,359 with one qualifying child.

- $503 with no qualifying children.

All you have to do to get your hands on that money is claim it the Earned Income Tax Credit. Strangely enough, about 20% of eligible tax filers pass it up.Unless you also like turning down free money, you'd be wise to see what a little extra paperwork can do for you.

The article This Tax Credit Could Save You Thousands This Year originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.